Comparing Best Income Protection Insurance NZ (2025 Update)

Imagine earning NZ$1,150 a week—then falling ill and finding ACC only offers you NZ$393/week, leaving a NZ$757 shortfall every single week.

In 2025, Best Income Protection Insurance NZ isn’t optional—it’s your financial lifeline. Whether you’re a salaried employee, self-employed, a parent, or a business owner, a serious illness or injury can devastate your cash flow and drain your savings in weeks. The right policy steps in to replace up to 75% of your income when you can’t work, keeping your mortgage, bills, and lifestyle intact.

What You’ll Learn

- The Big Picture: Why ACC leaves a gap and who needs cover now

- Comparison Playbook: Step-by-step on waiting periods, benefit terms, and premium structures

- Provider Rankings: A neutral A/B/C/D table + our partner grid for AIA, Asteron Life, Fidelity Life & Partners Life

- Real Kiwi Case Studies: Three true-to-life scenarios with payouts, timelines, and outcomes

- Pro Tips & Pitfalls: Bundling hacks, review reminders, and exclusion traps to avoid

- ROI Breakdown: Exact premium vs. payout math so you see the value

- FAQS & Legal Updates: Quick answers and 2025 regulatory changes

Why Income Protection Matters for Kiwis in 2025

FACT: ACC Only Covers Accidents

- ACC processed 1.2 million claims in 2023–24, but just 10 per cent were for illness or gradual-process injuries (ACC Annual Report 2024)

- Non-accidental conditions (like back pain or stress) cause 60 per cent of all workdays lost (Stats NZ).

- Max ACC payout for illness is NZ$393/week, yet the average Kiwi earns NZ$1,150/week, leaving a NZ$757 gap you must fund.

Legal Insight: Under the ACC Act 2001, only accidents (and a handful of gradual-process events) are covered. Cancer, heart disease and mental health conditions? Your responsibility.

STEP 1: Identify Your Risk Profile

- Employees: five days’ paid sick leave per year under the ERA 2000. After that? Unpaid leave.

- Self-employed & Contractors: Zero statutory sick days—every hour off equals lost income.

- Parents & Homeowners: Average mortgage of NZ$600/week plus rent, school fees, and groceries—no payment pause.

- Small-Business Owners: Your absence can stall cash flow, staff wages, and supplier bills.

PRO TIP: Tally up your total monthly outgoings. If it’s over NZ$3,000, target a policy that pays up to three-quarters of your usual pay when you can’t work.

REAL KIWI STORY: Sarah the Self-Employed Designer

Sarah, a Wellington-based freelance graphic designer, faced an unexpected setback when she needed knee surgery in July 2024. With no ACC cover or sick pay, her policy’s 4-week waiting period kicked in, and from week 5 she received 75 % of her NZ$1,250 weekly income (about NZ$937). Thanks to that payout, she managed rent, utilities, and groceries without touching her savings.

“I didn’t think minor surgery would derail my finances, but I was wrong. Best Income protection insurance nz saved my business—and my peace of mind.” —Sarah.

STEP 2: Calculate Your Income Shortfall

- Average Your Earnings: Total income over 12 months ÷ 52 weeks.

- Subtract ACC Max: NZ$1,150 – NZ$393 = NZ$757 shortfall.

- Multiply by Waiting Period: e.g., NZ$757 × 8 weeks = NZ$6,056, you must cover.

PRO TIP: Round up to the nearest NZ$100. A little buffer beats a big headache later.

Follow our step formula to see how much of a gap ACC leaves you. Or

Calculate exactly how much cover you need with our full gap calculator guide.

WHY THIS MATTERS NOW

- 1 in 3 Kiwis will face a disabling illness before 65

- A NZ$15,000 emergency fund can vanish in just 12 weeks at NZ$1,250/week spending.

- WINZ hardship assistance caps at NZ$450/week—and is means-tested with processing delays.

FACT: Missing one mortgage payment can trigger late fees, credit-rating hits, and lender penalties—all avoidable with income protection.

If you’re new to income protection, start with the basics in our foundational guide.

How to Compare the Best Income Protection Insurance NZ Policies

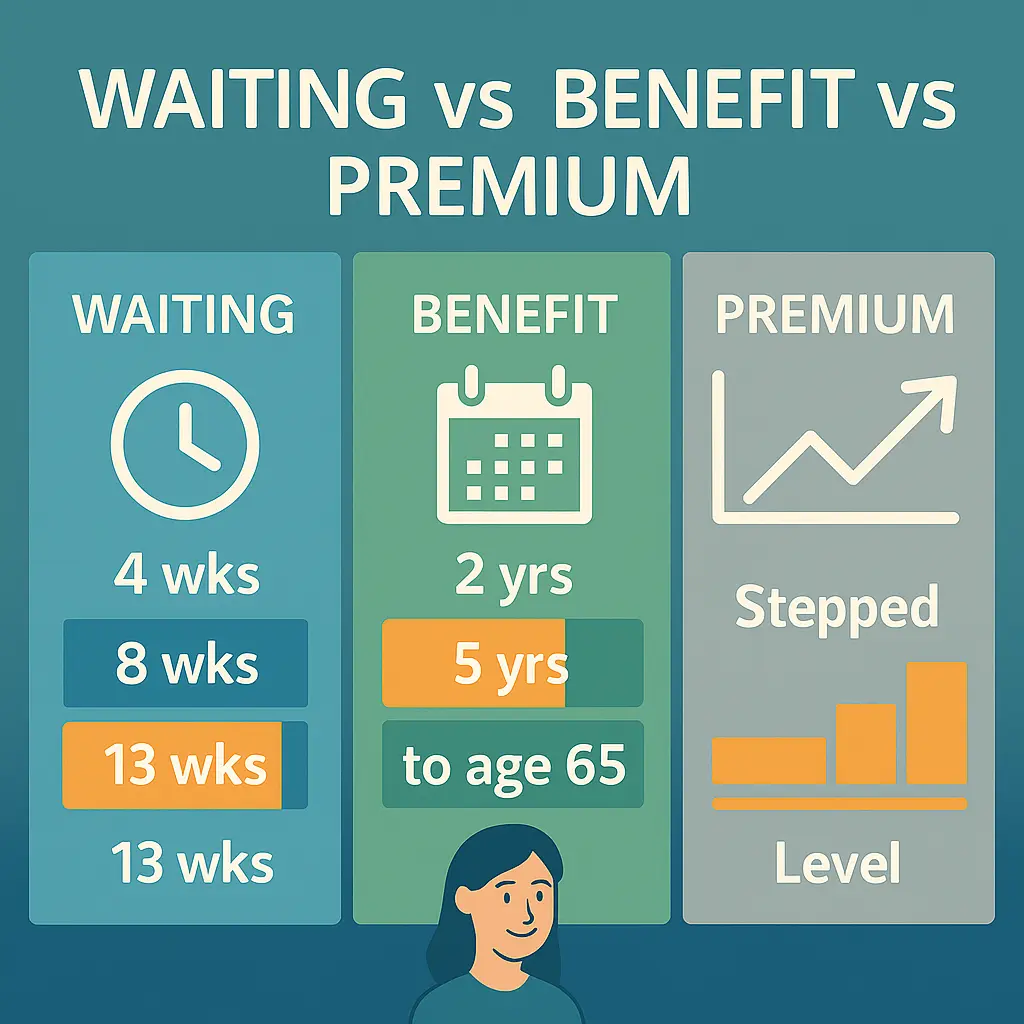

STEP 1: Compare Waiting Periods

4 Weeks

○ Fastest payout, ideal if you have minimal savings.

○ Premium impact: ~25% higher than the 13-week wait.

8 Weeks

○ Balanced option: moderate premiums and delay.

○ Popular mid-range choice for many Kiwis.

13 Weeks

○ Lowest premiums—up to 30% cheaper than a 4-week wait.

○ Requires a solid emergency fund (≈ NZ$3,000–4,000).

PRO TIP: If you have at least three months of living costs in savings, a 13-week wait can slash your annual premiums by NZ$400–500.

STEP 2: Evaluate Benefit Periods

2-Year Cover

○ Cost-effective: premiums are 20–30% lower than “to 65”.

○ Best for: short-term risks (e.g., recovery from surgery).

To Age 65 Cover

○ Lifetime peace of mind: payouts continue until retirement age.

○ Higher cost, but critical for long-term or chronic conditions.

INSIGHT: Under-30s often start with a 2-year term, then upgrade “to 65” as income and responsibilities grow.

STEP 3: Choose Your Premium Type

Stepped Premiums

○ Low entry cost (e.g., NZ$65/month at age 30).

○ Annual increases (~5–7%), potentially tripling by retirement.

Level Premiums

○ Higher start (e.g., NZ$90/month at age 30).

○ Locked-in rate—no surprises later.

PRO TIP: If you’re on a fixed income or nearing retirement, level premiums protect your budget from price spikes.

Top Income Protection Providers in NZ (2025 Rankings)

Neutral Comparison Table

| Provider | Waiting Periods (weeks) | Benefit Periods | Max of Income | Key Feature |

| Provider A (AIA) | 2, 4, 8, 13, 26, 52, 104 | 1, 2, 5 years, or to age 65 (70 for some roles) | Up to 75% typically | Pregnancy Premium Waiver, Vitality Post-Care Recovery, Return-Home Benefit |

| Provider B (Asteron Life) | 2, 4, 8, 13, 26 (or 1–2-year waits) | 2 years, 5 years, or to age 65/70 | Covers 75% of actual income loss | Loss of Earnings Plus: Rehabilitation & Retraining Support |

| Provider C (Fidelity Life) | 2, 4, 8, 13, 26, 52, 104 | 2 years, 5 years, to age 65/70 | Up to 75% of gross income | Choice of Indemnity or Agreed Value cover |

| Provider D (Partners Life) | 4–104 | Short-term options (3, 6, 12 months) or to retirement age | Up to 75% of pre-disability income | Recovery Support & Return-to-Work Benefits; Special Care Benefit |

*Note:** All details (waiting periods, benefit terms, cover percentages, and key features) are drawn from publicly available PDSS as of May 2025 and may change. AIA’s payout reduces from 75 % to 60 % after 24 months. For full policy documents and the latest offers

Compare Now

Real-Life Case Studies

Case Study 1: Mike’s Rugby Injury

- Who: Mike, a 32-year-old Christchurch plumber and weekend rugby player.

- What Happened: Broke his ankle playing club rugby off-duty in May 2024.

- Policy Setup: 8-week waiting period, “to age 65” benefit term, stepped premiums.

- Timeline & Payout:

- Weeks 0–8: Used savings (≈ NZ$3,200) to cover household bills.

- Week 9: The policy kicked in, paying 75 per cent of his NZ$1,200/week income (≈ NZ$900).

- Week 9–14: Received NZ$900/week for six weeks—fully covering mortgage and living costs.

Outcome: Kept debt-free, avoided dipping into KiwiSaver or credit cards, and returned to work without financial stress.

Key Takeaway: Even with savings, an 8-week wait can drain your emergency fund. A shorter wait (e.g., 4 weeks) may cost more in premiums but preserve cash reserves.

Case Study 2: Anna’s Chronic Illness

Anna, a 45-year-old secondary-school teacher in Tauranga, was diagnosed with an autoimmune condition in January 2025 and relied on roughly NZ$16,000 in savings during her policy’s 13-week waiting period. From week 14, her level-premium plan (2-year term) paid 70 % of her NZ$1,300 weekly salary—about NZ$910—each week for the next 52 weeks, allowing her to pay down mortgage principal, cover medical bills, and avoid WINZ hardship support.

Key Takeaway: Level premiums can be worth the extra initial cost when you know you’ll need long-term support. Here we get to know how best income protection insurance NZ saved Anna’s life.

PRO TIP: Learn & Optimise

- Review Definitions: Make sure “own-occupation” or “partial disability” terms match your real job duties.

- Adjust Annually: Update insured income if you get a raise or change roles.

- Check Add-Ons: Look for support services (rehab, retraining, recovery equipment) that can cut your recovery time.

Pro Tips for Getting the Best Deal

STEP 1: Bundle to Save

- Why Bundle? Insurers love multi-policy customers—and you should too.

- Typical Discount: 10–15 per cent off combined premiums when you add life, trauma, or TPD cover.

- How to Do It:

- Request a quote for standalone income protection.

- Ask for a bundled quote including life or trauma.

- Compare savings vs. standalone cost.

PRO TIP: Even if you don’t need extra cover now, bundle temporarily to lock in the discount—then drop the add-on later if it’s surplus to requirements.

STEP 2: Review Annually

- Set a Calendar Reminder: Pick a date each year—your policy anniversary works great.

- Check Your Income: Have you had a raise, bonus or side-gig earnings? Update your insured amount.

- Assess Life Changes: New baby, new mortgage, new business venture—your cover should keep pace.

INSIDER INSIGHT: Brokers report 70 per cent of clients under-insure within two years of their policy start date simply because they forget to update it.

STEP 3: Shop at Key Milestones

- Graduating Uni or Starting Work: Lock in lower premiums while you’re young and healthy.

- Buying a Home: Ramp up cover to match your mortgage repayments.

- Approaching Retirement: Consider switching to level premiums for predictable costs.

PRO TIP: If you’re switching jobs, check for portability clauses—keep your cover even if your new employer offers different benefits.

BONUS TIP: Leverage “Cooling-Off” Windows

- Most policies include a 30-day “cooling-off” period after signing. Test the customer service by calling to ask questions. If you’re unhappy, cancel without penalty.

Cost vs Benefit: Is It Worth It?

STEP 1: Compare Average Premiums vs. Typical Payouts

Here’s what Kiwis pay—and what they receive—based on insurer PDS data and a Sorted.org.nz survey (2024):

| Age Bracket | Avg Premium/Month | Avg Weekly Payout |

| Under 30 | NZ$60–90 | NZ$2,500 |

| 30–45 | NZ$80–120 | NZ$3,500 |

| 45–60 | NZ$100–150 | NZ$3,200 |

Bold Insight: For NZ$1,200/year (≈ NZ$100/month), you could secure up to NZ$3,500/week when you can’t work—a 291% weekly ROI on your premiums.

STEP 2: Calculate Your ROI

- Annualise Your Premium: Monthly premium × 12.

- Estimate Annual Payout Value: Weekly payout × average number of claim weeks (e.g., 8 weeks).

- ROI Formula: (Payout Value ÷ Annual Premium) × 100%.

PRO TIP: Even a short, 8-week claim typically delivers 5–10× the value of your annual premium. That’s peace of mind you can’t put a price on.

STEP 3: Consider the True Cost of No Cover

- ACC Gaps: Only covers accidents—max NZ$393/week for illness.

- WINZ Support: Capped at NZ$450/week, means-tested and delayed.

- Savings Drain: A NZ$15,000 emergency fund can vanish in just 12 weeks at NZ$1,250/week spending.

- Hidden Costs: Credit card interest, late payment fees, stress and reduced recovery speed.

FACT: Without the best income protection insurance NZ cover, the average Kiwi faces a NZ$6,000 shortfall during an 8-week illness, before credit card interest or WINZ delays.

Run Your Personal Income Protection Quote

Common Pitfalls & How to Avoid Them

PITFALL 1: Under-Insuring Your True Income

What happens: You insure only your base salary and forget to include bonuses, overtime or KiwiSaver employer contributions.

Why it hurts: Your payout matches what you declared, leaving you out of pocket if you underquote.

Quick fix:

- Pull your last 24 months of IRD income statements (they show everything).

- Total all earnings (base + extras) and divide by 52 for your true weekly income.

- Round up to the nearest NZ$100 for a safety buffer.

PRO TIP: Link your premiums to a dedicated “Insurance” account so you never miss a payment.

PITFALL 2: Overlooking Policy Exclusions

What happens: You assume every illness or injury is covered, only to find mental-health caps, gradual-process or high-risk hobby exclusions.

Why it hurts: A claim can be denied or reduced, leaving you scrambling.

Quick fix:

- Highlight every exclusion in the PDS.

- Ask your broker for real examples of declined claims.

- Compare exclusion lists side by side before you buy.

Warning: Mental-health cover often tops out at 24 months—make sure it meets your needs.

PITFALL 3: Letting Your Policy Lapse

What happens: You miss a premium payment and forget to restart your cover; quietly, it cancels.

Why it hurts: Reapplying can trigger new medicals, higher rates, or even declined cover.

Quick fix:

- Automate your premiums from a dedicated “Insurance” bank account.

- Use “premium holidays” only when you have a clear restart date.

- Set an annual calendar reminder on your policy anniversary.

Pro Tip: Bookmark Employment NZ’s Sick Leave page so you know your entitlements while you sort cover.

You can check your Employment NZ: Sick Leave Rights.

PITFALL 4: Ignoring Market Changes

What happens: You stick with the same old stepped-premium, 2-year term policy you bought years ago—even though new riders (inflation protection, redundancy cover, wellness rewards) are available.

Why it hurts: You miss out on better value and extra benefits.

Quick fix:

- Review your policy every 2–3 years.

- Scan competitors’ PDSS for new features.

- Top up or switch if you find a better deal.

Avoid Pitfalls—Compare Policies Now

FAQS on Best Income Protection Insurance NZ

Q1: What Does Income Protection Cover?

It usually replaces 70–80 % of your pre-tax earnings if illness or injury stops you working (ACC-covered accidents excluded).

Insight: Income protection generally covers 70–80% of your pre-tax earnings and excludes ACC events. For a full coverage breakdown, see “What Does Income Protection Cover?” in our guide.

Q2: How Do Waiting & Benefit Periods Work?

Your waiting period (4, 8 or 13 weeks) delays the first payout; your benefit period (2 yrs, 5 yrs or to age 65) sets how long you get paid.

Q3: Can I Claim ACC & Income Protection Together?

Yes – claim ACC for your treatment costs first, then use income protection to top up your lost earnings after the wait.

Q4: How Do I Switch Providers?

Apply for new cover before your old policy lapses; some insurers let you port pre-existing conditions, but others may require new medicals.

Q5: Is Income Protection Tax-Deductible?

Typically, yes for self-employed or rental-income earners; PAYE employees usually can’t claim—check the latest IRD ruling.

Q6: Can I Add Redundancy Cover?

Yes – if offered, a redundancy rider pays you a set benefit if you lose your job involuntarily.

Insight: Not all providers offer this—ask specifically during quoting.

Q7: What Happens If I Change Jobs?

If your policy is portable, you keep your cover with no new underwriting; otherwise, you’ll need to reapply, possibly at different rates.

Got More Questions? Compare Policies Now

Next Steps

- Review Your Needs – Use our free worksheet to list your expenses and coverage gap.

- Compare Quotes – Click the link below and get tailored quotes from leading providers.

- Secure Your Future – Choose a policy, sign up online, and enjoy peace of mind.

Ready to Protect Your Income?

{kind=link}

{kind=link}

{kind=link}

{kind=link}