Choosing the Right Income Protection Waiting Period in New Zealand

When it comes to income protection insurance, one of the most important—but often overlooked—things you’ll need to decide is your waiting period. In simple terms, the income protection waiting period is the time you’ll wait from when you first become unable to work because of illness or injury until your insurance payments start coming in.

Why does the waiting period matter so much? During this waiting time, you’ll need to manage your expenses using your resources, such as your savings, sick leave, or emergency funds. Picking a waiting period that’s too short might mean paying unnecessarily high premiums. On the other hand, choosing one that’s too long could leave you short of money when you need it most.

You might already have some common questions on your mind, like:

- “What’s the best waiting period for me?”

- “How will the waiting period affect my monthly premiums?”

- “Can I change my waiting period if my circumstances change later?”

Don’t worry—we’ve got you covered. This guide is designed specifically for New Zealanders, whether you’re an employee with regular sick leave benefits, a self-employed professional with unpredictable income, or a contractor juggling irregular payments.

In the next sections, we’ll break down exactly what the waiting period is, how it works, and the ways it affects your coverage and insurance costs—so you can make the best possible decision for your unique situation.

What is a Waiting Period in Income Protection?

Let’s start with the basics—what exactly does the waiting period (sometimes called the stand-down period) mean in the context of income protection insurance?

In simple terms, the waiting period is the set amount of time you’ll have to wait after becoming unable to work due to sickness or injury before your insurance payments kick in. Think of it as a buffer period where you’ll need to cover your living expenses using other resources, such as your savings, sick leave, or help from family and friends.

Here’s how it works within a typical policy: Let’s say you have a waiting period of four weeks. If you fall seriously ill and can’t work, your income protection payments won’t begin immediately. Instead, they will start exactly four weeks after you initially become unable to work, assuming you’re still off work at that point.

In New Zealand, insurers typically offer waiting periods of:

- 2 weeks

- 4 weeks

- 8 weeks

- 13 weeks

- 26 weeks (6 months)

- 52 weeks (1 year)

- 104 weeks (2 years)

To illustrate, imagine Sarah, a marketing manager, opts for a 13-week waiting period because she has ample sick leave and personal savings. After she breaks her leg in a skiing accident, Sarah uses her sick leave and savings for the initial three months. Once the 13-week waiting period ends, her income protection insurance starts paying, ensuring she remains financially secure during her recovery.

Choosing the ideal waiting period largely depends on your financial situation and your ability to support yourself during that initial time. If you’re still unsure about how income protection works overall, you can explore our comprehensive guide on What is Income Protection Insurance in NZ? for further clarity.

The Relationship Between Waiting Period and Benefit Period

Now that we’ve discussed the waiting period, it’s crucial to understand another important aspect of your income protection policy: the benefit period.

The benefit period refers to the maximum length of time that your insurance policy will continue to pay you once your waiting period is over, and you’re still unable to work. Common benefit period options in New Zealand include two years, five years, or even coverage extending right up until retirement age (typically age 65).

Your waiting period directly affects your coverage timeline because it determines when your benefit payments will begin. For instance, if you select a short waiting period of four weeks and a two-year benefit period, you’ll start receiving payments relatively quickly after you become unable to work, and they’ll continue for up to two years, assuming you’re still unable to return to your job.

Conversely, a longer waiting period, such as 26 weeks, means you’ll wait six months before payments kick in, but you’ll typically enjoy lower monthly premiums. However, you’ll need solid financial resources or other benefits, like ACC cover, to manage financially during this time.

Pro Tip: To effectively balance your waiting and benefit periods, consider your personal financial safety net, current savings, and any additional insurance covers you might have. For example, if you’re young, healthy, and have robust savings, a longer waiting period coupled with a longer benefit period could provide both affordability and extensive protection. But if you have limited savings or financial commitments, opting for a shorter waiting period and a medium-length benefit period (e.g., 2–5 years) may offer optimal peace of mind and security.

Ready to find the perfect income protection plan that matches your situation?

Factors to Consider When Choosing Your Waiting Period

Let’s face it: choosing the perfect income protection waiting period can feel overwhelming. But don’t worry—by looking at your own situation carefully, the decision gets a lot easier. Here’s a clear breakdown of what you should consider:

1. Emergency Fund: How much can you cover yourself?

- 3–6 months’ savings? → You can afford a longer waiting period (cheaper premiums).

- Little or no savings? → Choose a shorter waiting period (2–4 weeks).

2. Sick Leave & Annual Leave

- Lots of paid leave? → You can delay benefits = longer waiting period.

- Limited leave? → Go shorter so payments start sooner.

3. ACC Cover: Know what’s covered

- ACC only covers injuries, not illness.

- If illness risk is higher (and for most, it is) → shorter waiting period is safer.

- How ACC and Income Protection Work Together → full guide here.

4. Other Insurance (Mortgage Protection, etc.)

- Already have mortgage protection or other income covers?

→ You may not need quick IP payments → longer waiting period could save you $$$.

5. Monthly Budget & Expenses

- High fixed expenses (mortgage, rent, dependents)? → Shorter waiting period = more secure.

- Flexible budget? → A longer period could work.

6. Self-Employed or Contractors?

- No sick leave, inconsistent income → shorter waiting period is usually safer (2–4 weeks).

- More tips: Income Protection for Self-Employed Kiwis

7. Mental Health Considerations

- Mental health claims often take longer to assess.

- Want fast help? → Shorter waiting period = better option.

To get a full overview, check out our complete guide: What Is Income Protection Insurance in NZ?

Pros & Cons of Short vs. Long Waiting Periods

When selecting your income protection waiting period, one of the most important decisions is whether to go with a short or long waiting period. Both options have their own advantages and trade-offs, and the right choice depends on your personal financial situation and risk tolerance.

Short Waiting Periods (2–4 weeks)

Short waiting periods are ideal for those who need financial support as soon as possible after an illness or injury. If you choose a short waiting period—such as two or four weeks—your income protection payments will start quickly, helping you manage bills, rent, or mortgage payments during the early stages of recovery.

However, the main trade-off with a shorter waiting period is the higher premium. Since the insurer starts paying benefits sooner, it takes on more risk, which is reflected in the cost of your cover.

Short waiting periods work well for:

- Individuals with little to no savings.

- Those who have high fixed monthly expenses.

- Self-employed people or contractors who do not have sick leave.

Long Waiting Periods (13–26 weeks or more)

Long waiting periods offer a different set of advantages. If you can cover your expenses for an extended period—through savings, sick leave, or other resources—you can opt for a longer waiting period, which will generally lower your monthly premium.

This can be an effective way to manage costs while still having protection for serious, long-term situations.

Long waiting periods are better suited to:

- People with strong savings or employer-provided sick leave.

- Those looking to reduce premium costs while still maintaining long-term protection.

Final Thoughts

Choosing the right balance between premium cost and financial protection is key. There is no universal “best” option—what matters most is selecting a waiting period that fits your lifestyle and financial safety net.

If you’d like to explore which waiting period could work best for your situation, you can easily compare income protection insurance policies here.

Special Considerations for Self-Employed & Contractors

If you’re self-employed or working as an independent contractor, choosing your income protection waiting period requires a slightly different approach compared to employees.

Why? Simply put, self-employed individuals don’t have the benefit of employer-provided sick leave or annual leave. This means you’re fully responsible for covering any period where you’re unable to work, making your choice of waiting period even more important.

How to Choose When Income Is Irregular

When your income varies month to month, it’s crucial to think carefully about how much time you can realistically manage without earnings.

A shorter waiting period (such as 2–4 weeks) is often the better option for self-employed people, since it provides faster access to benefit payments. This can help smooth out your cash flow when illness or injury strikes.

However, if you’ve built up a robust financial buffer—perhaps several months’ worth of business and personal expenses—you might consider a slightly longer waiting period to reduce your premiums.

Building a Financial Buffer

Whether you choose a short or long waiting period, it’s wise to create a financial safety net:

- Aim for at least 3–6 months of savings.

- Factor in both personal living costs and essential business expenses (subscriptions, marketing, contractors, etc.).

- Remember that business income may take time to recover even after you return to work.

Real-World Examples

- Freelance Graphic Designer: Project-based income, no sick leave. Chooses a 4-week waiting period to ensure quick support during gaps in client work.

- Tradie (Plumber): Steady demand, but physical job = higher injury risk. Selects a 2-week waiting period for fast coverage.

- Consultant: Strong emergency fund and stable client contracts. Opts for a 13-week waiting period to save on premiums.

Pro Tip: If you’re self-employed, always review your waiting period regularly as your savings and business stability change.

Need help finding the right option for your business?

How Waiting Period Works with Other Benefits

Your income protection waiting period doesn’t operate in isolation. It’s important to understand how it interacts with other benefits you might already have, so you can make a more informed choice and avoid gaps or overlaps in your cover.

Coordinating with ACC

In New Zealand, the Accident Compensation Corporation (ACC) provides cover for injuries, but not illnesses. If you’re injured at work or elsewhere, ACC may provide weekly compensation payments after an initial stand-down period (typically 1 week).

Income protection policies usually integrate with ACC, meaning they won’t duplicate payments. Instead, your insurer may “top up” any shortfall after your waiting period expires.

Using Sick Leave First

If you’re an employee with sick leave entitlements, you can (and should) use this first during your waiting period. In many cases, your waiting period will begin from the date you are medically unable to work, not after you finish using sick leave, so it’s worth checking how your policy defines this.

Using sick leave helps you bridge the gap until your income protection starts.

Stacking with Mortgage Protection

Some Kiwis have both income protection and mortgage protection insurance. If this applies to you, consider how they work together:

- Mortgage protection often pays directly toward your mortgage.

- Income protection is more flexible, covering broader living expenses.

If stacked carefully, these can provide comprehensive protection, but you’ll want to align waiting periods to avoid gaps or overlaps.

Changing Jobs or Employment Type

If you switch from employee to contractor, or from salaried to self-employed, your risk profile changes. You may also lose access to employer sick leave or group cover.

Pro tip: Review your income protection waiting period and policy terms anytime your employment situation changes.

Want to see how different waiting periods stack up with your current cover?

Real-Life Scenarios: Waiting Period Choices

How do real people choose their income protection waiting period? Let’s look at some common situations:

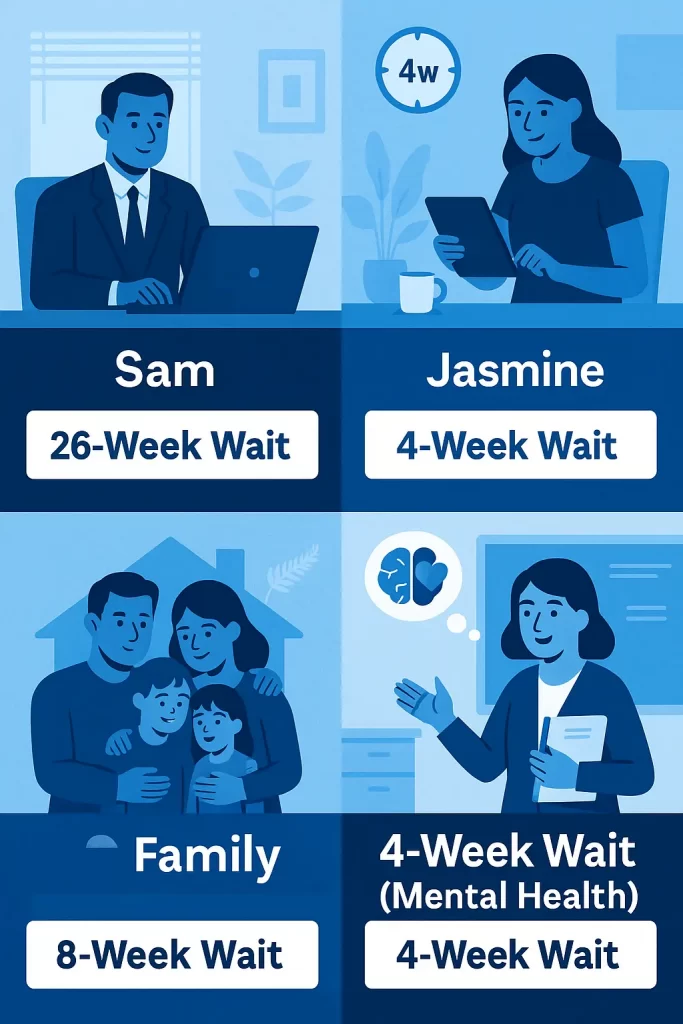

1️⃣ Employee with Strong Sick Leave & Savings → Long Waiting Period

Sam is a 40-year-old senior IT manager at a large firm.

✅ 4 months of paid sick leave

✅ $25K in emergency savings

✅ Stable household income (partner also works full-time)

Because Sam has solid financial backup, he chooses a 26-week waiting period. This lowers his premiums, and he knows he can comfortably cover the first 6 months of any illness or injury himself.

Lesson: If you’ve got strong sick leave + savings, a longer waiting period makes sense—and saves you money.

2️⃣ Young Contractors → Shorter Waiting Period

Jasmine is a 27-year-old freelance graphic designer:

✅ No employer sick leave (self-employed)

✅ Income varies month to month

✅ Just $3K in savings

She selects a 4-week waiting period. If she can’t work, bills will pile up fast. A short waiting period gives her peace of mind that income protection will start quickly.

Lesson: Self-employed or variable income? A shorter waiting period provides vital protection.

3️⃣ Family with Mortgage → Middle-Ground Choice

David & Amy are in their early 30s, with two young kids and a mortgage:

✅ 2 weeks of sick leave each

✅ Around $10K in shared savings

✅ Big monthly expenses: mortgage, childcare, groceries

They go with an 8-week waiting period, balancing premium savings with the need for income to start relatively soon if something happens.

Lesson: For families with mortgages and kids, a middle-ground waiting period offers a good balance of cost vs. protection.

4️⃣ Mental Health-Focused → Shorter Waiting Period Prioritised

Rebecca, a 35-year-old primary school teacher:

✅ Some sick leave

✅ $15K in savings

✅ Family history of mental health issues

She’s proactive—choosing a 4-week waiting period because mental health claims can take time to assess. She wants to minimise delays in getting financial support if she needs time off for stress or related conditions. Keep in mind that in New Zealand, some insurers have different terms for mental health cover, such as exclusions, waiting periods, or benefit limits. It’s important to check your policy wording carefully or get advice.

Lesson: If mental health coverage is a priority, go for a shorter waiting period to ensure quicker benefits.

Key Takeaway

There’s no “one-size-fits-all” answer. Your ideal income protection waiting period depends on YOUR income, savings, family situation, and risk tolerance.

👉 Want to see which option fits YOUR life? Compare income protection policies here.

How to Choose, Review & Adjust Your Waiting Period Over Time

Your income protection waiting period shouldn’t be a “set and forget” decision. As life changes, so should your cover. Let’s walk through how to choose the right waiting period—and when to review it.

How to Choose the Right Waiting Period

Start by considering your personal and financial situation:

- Savings: The bigger your emergency fund, the longer a waiting period you can afford.

- Sick leave: Generous sick leave? You can delay income protection kicking in.

- ACC cover: If your risk is more illness than injury, adjust your waiting period accordingly.

- Fixed expenses: Mortgage, rent, childcare—if your monthly costs are high, you’ll likely want a shorter waiting period.

- Employment type: Self-employed? No sick leave? You’ll usually need a shorter waiting period.

👉 For a full refresher, check out our guide to income protection insurance in NZ.

Life Stage Changes to Watch For

Big life changes are natural times to reassess your waiting period:

- Having kids → New expenses, may need a shorter waiting period.

- Buying a home → Mortgage adds a fixed financial commitment.

- Changing jobs → Switching to self-employed or contracting removes employer sick leave.

- Income changes → Higher income might support a longer waiting period (lower premiums).

When Should You Review Your Cover?

Best practice: Review every 12–24 months or after any major life event (new job, mortgage, new baby, marriage, divorce).

How Easy Is It to Adjust?

Good news: many policies allow you to adjust your waiting period, often at the policy anniversary.

However:

- Shortening the waiting period may require new underwriting.

- Lengthening is usually easier (and reduces premiums).

Pro Tip: Don’t wait too long. It’s better to adjust proactively than find yourself under-protected when life changes. For more information about how financial services and insurance advice are regulated in New Zealand, you can visit the FMA’s official website.

👉 Ready to check which waiting period works best for YOU today?

FAQs: Income Protection Waiting Period

1️. What is the most common waiting period in NZ?

Industry data from major NZ insurers shows that 4 weeks and 13 weeks are among the most commonly selected waiting periods

2. How does ACC affect my waiting period choice?

ACC covers injuries, but not illnesses, so you may want a shorter waiting period to cover illnesses.

3️. Can I change my waiting period after getting a policy?

Yes! You can usually change it once a year. Going shorter may need approval.

4️. Does the waiting period apply to mental health claims?

Yes — the waiting period applies to all types of claims, including mental health.

5️. Is a longer waiting period always cheaper?

Yes — the longer you wait, the cheaper your monthly payments.

6️. What’s the best waiting period if I’m self-employed?

Usually 2 to 4 weeks, because you don’t have sick leave to rely on.

7️. When does my waiting period start?

It starts from the date your doctor certifies you unfit for work, not from when you file the claim.

8️. Can I have different waiting periods for different policies?

Yes — for example, your mortgage protection might have a different waiting period from your income protection.

9️. What happens if I get sick again later?

Some policies will skip the waiting period if it’s for the same illness — check your policy wording.

Conclusion

Choosing the right income protection waiting period is one of the most important parts of building a policy that truly works for you. The waiting period directly affects how soon your payments would start if you couldn’t work, and it also impacts how much you’ll pay in premiums.

There’s no single “best” option. The right choice depends on your savings, sick leave, income stability, expenses, and personal priorities. That’s why it’s worth taking the time to assess your situation, and don’t be afraid to adjust your cover as life changes.

Remember: your waiting period should give you peace of mind, not stress. Whether you’re self-employed, supporting a family, or simply want affordable protection, there’s a waiting period that can fit your needs.

Ready to compare options and find the best income protection policy for you?

Disclaimer

This article is provided for general information purposes only and is not intended to provide personal financial advice. While every effort has been made to ensure the information is accurate and up-to-date for New Zealand readers, income protection insurance products and features may vary between providers. Before making any decisions about insurance cover, you should seek advice from a licensed Financial Advice Provider or qualified insurance adviser to ensure the product is suitable for your individual needs and circumstances.

{kind=link}

{kind=link}

{kind=link}