How Much Income Protection Cover In NZ Do You Really Need ?

Why Income Protection Cover in NZ Matters in 2025

Imagine waking up tomorrow and realising you can’t work — not for a few days, but for weeks, months, or longer. Maybe it’s due to a serious illness, injury, or mental health crisis. Now imagine that your regular paycheque has stopped — but your mortgage, groceries, childcare, and power bill haven’t. That’s where income protection cover in NZ becomes essential.

It’s not a luxury — it’s your financial backup plan. The one thing that stands between you and financial instability when you’re medically unable to earn.

Yet one of the most common questions Kiwis ask is:

“How much income protection do I actually need?”

Many either underinsure themselves, risking hardship, or overpay for cover they don’t use.

✅ In this guide, you’ll learn:

● Why income protection is essential in NZ’s 2025 economy

● How to accurately calculate your cover using a proven step-by-step method

● How to customise your policy to fit your budget and lifestyle

● Common mistakes to avoid (from real Kiwi cases)

● And how to balance premiums vs protection — like a pro

🧠 2025 Insight: Why It’s More Critical Than Ever

● Over 70% of income-related claims are due to illness, not accidents

● The average claim duration is 7.2 months.

With rising living costs in cities like Auckland and Wellington, being out of work even temporarily can devastate your financial situation.

💬 “I thought ACC would cover me,” says one Christchurch tradie. “But my illness wasn’t an accident — so I got nothing.”

Compare income protection quotes in NZ

✅ Why Getting the Right Amount of Income Protection Cover Matters

Choosing the right amount of income protection cover in NZ isn’t just a technical decision — it’s the foundation of your financial stability during a crisis. Too little, and you may struggle to meet basic needs. Too much, and you’re overpaying on premiums you may never fully benefit from.

Underinsurance vs Overinsurance: What’s the Risk?

| Issue | Risk | Real-World Impact |

| Underinsurance | You won’t have enough to cover your essential expenses | You could fall behind on rent or mortgage payments, incur credit card debt, or be forced to rely on WINZ or whānau |

| Overinsurance | You’re paying for more than you realistically need | Higher monthly premiums reduce savings capacity and may become unaffordable |

🔍 Insight from 2025 Data:

Research from FSC NZ shows 1 in 3 Kiwis underestimate how much cover they need, often by $800–$1,200/month, leaving them financially exposed during recovery.

🧾 Real Kiwi Case Study: Emma & the $2,000 Gap

Emma, a 38-year-old Wellington designer with two children, insured herself for $2,500/month. But when she had to stop working for six months due to breast cancer, her actual monthly costs were closer to $4,500.

She had to:

● Dip into emergency savings

● Rely on her partner’s income

● Delay mortgage repayments (accruing interest)

Had she accurately assessed her needs and chosen even $4,000/month cover, the financial stress would have been significantly reduced.

💬 Emma’s takeaway:

“I thought I’d be fine with the basics covered — I didn’t realise how fast everything added up.”

🔍 Compare Income Protection Options Now

Free quotes from trusted NZ providers. No pressure. No hidden fees.

🧠 Pro Tip:

Before you buy a policy, ask yourself:

● “Could I cover my essential expenses for 6+ months without working?”

✅ What Does Income Protection Insurance Typically Cover in New Zealand?

Before you determine how much income protection cover you need, it’s crucial to understand exactly what income protection in NZ actually includes — and what it doesn’t.

Income protection is designed to replace a portion of your income when you’re medically unable to work due to illness or injury. In 2025, with rising living costs and increasing health-related absences, this cover has become more relevant than ever.

📌 Core Coverage: What’s Typically Covered?

| Condition Type | Examples | Why It Matters |

| Physical Injuries | Fractures, back injuries, repetitive strain | Prevents you from doing physical work or daily tasks |

| Major Illnesses | Cancer, heart attack, stroke, diabetes | Long recovery time may prevent even desk-based work |

| Mental Health | Depression, anxiety, PTSD, burnout | One of the top 3 causes of income protection claims |

| Surgical Recovery | Spinal, organ, or orthopaedic surgeries | Extended downtime requires physical and mental rest |

💡 Updated Insight (2025):

According to the Insurance Council of NZ, over 70% of income protection claims are now for illness, not injury. This includes long-term conditions like cancer, autoimmune disorders, and severe stress burnout.

❌ What’s Not Covered (Know This!)

Understanding exclusions is just as important. Here’s what most NZ income protection policies do NOT cover:

| Not Covered | Explanation |

| Redundancy | Only covered if added as a specific rider or separate product |

| Undeclared Pre-existing Conditions | Can void a claim, especially common for mental health or injuries not disclosed |

| Pregnancy-related leave | Standard leave is not covered unless medically necessary (e.g., bed rest) |

| Voluntary leave or sabbatical | If you quit or take unpaid leave for non-medical reasons, claims won’t apply |

| Workplace misconduct | No payout if dismissal or absence is due to breach of conduct or fraud |

⚠️ Warning:

Non-disclosure is still the #1 reason claims are denied in New Zealand. Always declare past injuries, illnesses, or medications — even if they seem minor.

🧑🔧 Real-World Example: Liam’s Injury

Liam, a 34-year-old builder in Christchurch, strained his lower back after years of repetitive lifting. ACC covered part of the initial treatment but could not extend long-term income support when his condition lingered beyond 3 months.

✅ His income protection policy covered $4,000/month for 5 months, which helped him stay afloat until he could resume part-time work.

🧠 Pro Tip:

If you’re in a high-risk job or already managing a chronic condition, consider:

● A partial disability benefit (lets you claim if you can only work part-time)

✅ How to Calculate the Right Income Protection Cover in NZ (2025 NZ Edition)

Understanding your ideal income protection amount isn’t about guesswork — it’s about knowing your real expenses and risks and how long you could survive without your regular paycheque.

This step-by-step breakdown will help you calculate just the right amount of cover, not too little, not too much.

🧮 Step-by-Step: Calculate How Much Income Protection You Need

📌 Step 1: List Your Monthly Essential Expenses

Start with everything you must pay each month — no fluff, just the necessities:

| Expense Category | Example Amount (NZD) |

| Mortgage or Rent | $2,000 – $3,000 |

| Utilities (Power, Water, Internet) | $400 – $600 |

| Groceries | $800 – $1,000 |

| Insurance (car, health, contents) | $250 – $400 |

| Transport (fuel, bus, etc.) | $300 – $500 |

| School Fees & Childcare | $500 – $1,000 |

| Debt Repayments (loans, credit cards) | $400 – $800 |

💡 2025 Insight: In most NZ households, essential expenses sit between $4,500 – $6,000 per month, especially in Auckland, Wellington, and Christchurch.

📌 Step 2: Add a Safety Buffer (25%)

Unexpected costs pop up — medical bills, appliance repairs, fuel spikes, etc. Add 25% to your base expenses for flexibility.

Formula:

Essential Expenses x 1.25 = Ideal Monthly Cover

✅ Example:

If your monthly expenses = $5,000,

Then: $5,000 x 1.25 = $6,250 in recommended monthly income protection

Get a free NZ income-protection quote in 2 minutes.

To know more, read our article about What Is Income Protection Insurance in NZ?

📌 Step 3: Compare With the Insurer’s Cap (Usually 75% of Gross Income)

NZ insurers generally let you cover up to 75% of your gross income. That means if you earn:

| Annual Salary (Gross) | Max Cover (Monthly) |

| $60,000 | $3,750 |

| $90,000 | $5,625 |

| $120,000 | $7,500 |

🧠 Check Your Fit:

● If your calculated cover ($6,250) is less than 75% of your gross, ✅ you’re in the safe zone.

● If it exceeds the insurer’s limit, consider cutting extras or using savings for the remainder.

Check your income tax calculator on the Insurance Council of NZ.

📌 Step 4: Adjust for Waiting & Benefit Periods

Your income protection premium also depends on how long you:

● Wait before payments begin (waiting period)

● Receive payments (benefit period)

Choose these based on your savings and job risk level.

📊 Real Kiwi Example: Meet Sarah

Sarah is a 38-year-old teacher in Hamilton.

| Income | $90,000/year (gross) |

| Monthly Take-Home | ~$5,000 (after tax) |

| Expenses | $4,000 (mortgage, kids, food, etc.) |

| Buffer (25%) | $5,000 x 1.25 = $6,250 target |

| Max Allowed (75%) | $5,625 (per insurer rules) |

🎯 Sarah’s strategy:

● Gets a $5,500/month cover (close to cap)

● Chooses 60-day wait (uses savings buffer)

● Opts for a 5-year benefit period (balance of cost and coverage)

🔁 Review and Reassess Annually

Adjust your policy:

● After a job change

● When you buy a home

● After starting a family

● Every 12–18 months

💡 Pro Tip: Use NZ budgeting tools like Sorted’s Budget Planner to recalculate expenses before policy updates.

✅ Key Factors That Affect Your Income Protection Cover in nz (and Cost)

Once you’ve estimated how much income protection cover you need, the next step is to understand the key variables that influence how much your cover will cost — and how secure it will be.

These factors will shape your policy choices, premium amount, and your ability to customise the plan around your budget and lifestyle.

🔍 1. Lifestyle Level: Essentials-Only vs Lifestyle Cover

When choosing your benefit amount, ask yourself:

● Do I just want to survive financially (cover basic bills)?

● Or do I want to maintain my current lifestyle (hobbies, Netflix, gym, holidays)?

💡 Pro Tip: Most Kiwis underestimate the emotional stress of living on a “survival budget”. If your mental well-being depends on comfort items (like streaming services or outings), include a buffer for them.

🕒 2. Waiting Period (Stand-Down Time)

This is how long you wait before benefits kick in.

| Waiting Period | Pros | Cons | Best For |

| 30 Days | Fast payments start | Higher premiums | Those without much savings |

| 60 Days | Balanced cost vs speed | Must self-fund 2 months | Kiwis with moderate savings |

| 90 Days | Cheapest premiums | Long wait to claim | Those with strong savings or leave |

💬 Tip: Match your waiting period to your emergency savings. If you can cover 2 months from savings or sick leave, go with 60 or 90 days.

📅 3. Benefit Period (How Long You’ll Receive Payments)

This is how long your insurer will continue paying if you’re off work.

| Benefit Period | Pros | Cons | Best For |

| 2 Years | Lower premiums | Limited protection | Young, healthy Kiwis |

| 5 Years | Good middle ground | Moderate premiums | Families, mid-career earners |

| To Age 65 | Maximum long-term security | Highest premium | Self-employed or high-risk jobs |

🧠 Insight: According to Fidelity Life (2025), the average NZ income protection claim lasts 18–24 months, but longer cover protects against severe illnesses like cancer or MS.

📊 4. Agreed Value vs Indemnity Value (How Your Benefit Is Calculated)

| Policy Type | What It Means | Best For |

| Agreed Value | Locks in your monthly payout based on declared income (even if income later drops) | Self-employed or variable income |

| Indemnity Value | Payout based on income at claim time | Salaried workers with stable income |

💬 Pro Tip: Self-employed Kiwis should opt for Agreed Value. It gives peace of mind and avoids payout delays.

➕ 5. Optional Add-Ons (Riders)

Some riders are useful — others add cost without much benefit.

| Add-On | Value | Worth It? |

| Waiver of Premium | No premiums while claiming | ✅ Yes |

| Partial Disability Benefit | If returning to part-time work | ✅ Yes |

| Indexation (CPI Increase) | Keeps payout up with inflation | ✅ Yes |

| Redundancy Cover | Covers involuntary job loss | ✅Talk to an advisor first |

| Future Increase Option | Adjust the cover without new health checks | ✅ Especially for growing incomes |

🧠 Insight: Inflation protection (indexation) is more valuable in 2025 as NZ faces rising household costs.

📋 Summary Table: Matching Factors to Your Needs

| Factor | Choose If… |

| Essentials-Only Cover | You want the lowest possible premium |

| 30-Day Wait | You have no or minimal savings |

| Age 65 Benefit | You rely heavily on your income to support a household |

| Agreed Value | Your income fluctuates (e.g., self-employed) |

| Indexation | You want payouts to keep pace with inflation |

🧪 Real-Life Kiwi Scenarios: How Different People Choose the Right Cover

One of the best ways to understand income protection is to see how different New Zealanders approach it based on their lifestyle, income level, and financial responsibilities.

Below are real-world examples of how people in different life stages and financial situations determine how much income protection they need — and why it matters.

🎓 Sophie — Uni Student

● Income: $2,000/month

● Expenses: $1,200

● Cover Needed: $1,200/month

✅ Why it works: Sophie lives simply and just needs to cover rent and food.

👨💼 Young Professional (First Flat, Student Loans)

● Name: Dylan

● Age: 28

● Income: $5,500/month

● Expenses: $3,800 (student loan, rent, car, power, internet)

● Suggested Cover: $4,000/month

✅ Why it works: Dylan covers essentials and allows for a slight lifestyle buffer. He selects a 60-day waiting period and a 2-year benefit to keep premiums affordable.

💡 Tip: Flatting professionals often underestimate living costs. Include loan repayments and digital subscriptions in your total.

🔧 Tamati — Self-Employed Tradie

● Income: $7,000/month

● Expenses: $5,200

● Cover Needed: $5,500–$6,000/month

✅ Why it works: Tamati has no sick leave, so he locks in his cover with an agreed value policy.

How to Choose the Right Income Protection Policy

Choosing the right policy isn’t about picking the cheapest — it’s about what works for you.

✅ Step 1: Choose the Right Waiting & Benefit Period

| Feature | What It Means | Tip |

| Waiting Period | Time before payments start (e.g., 30–90 days) | Longer wait = cheaper premium |

| Benefit Period | How long payments last (e.g., 2 years, 5 years, to age 65) | Longer = better protection |

💡 Example:

If you have emergency savings, choose a 60- or 90-day waiting period to reduce cost.

✅ Step 2: Decide Between Agreed vs Indemnity Value

| Type | Best For | What It Means |

| Agreed Value | Self-employed, variable income | Fixed benefit, based on income when you apply |

| Indemnity | Salaried workers | Based on actual income at claim time |

✅ Step 3: Check for Must-Have Features

Look for:

● Coverage for illness and injury (not just accidents)

● Option to adjust cover later

● Indexation to keep up with inflation

● Partial disability benefit (if you return part-time)

● Waiver of premiums during claims

✅ Step 4: Use a Licensed NZ Adviser

A financial adviser can:

● Help compare options tailored to your income.

● Get better pricing or flexible terms

● Explain tricky policy terms clearly

💬 Pro Tip:

Don’t just Google a policy and apply. A licensed NZ adviser is free and gives personalised help.

💸 How Much Does Income Protection Insurance Cost in New Zealand?

Now that you understand how much cover you might need, the next natural question is, How much will it cost me?

The good news? Income protection insurance in NZ is flexible and customisable, which means you can often shape it around your budget, as long as you understand the key pricing factors.

🔍 What Affects the Price?

| Factor | Impact |

| Age | Older = higher risk = higher premium |

| Occupation | Risky jobs (e.g. tradies) cost more than office work |

| Health & Smoking | Health conditions or smoking raise your premium |

| Benefit Amount | Higher monthly benefit = higher cost |

| Waiting Period | Longer wait = lower cost |

| Benefit Period | “To age 65” costs more than a 2-year benefit |

📊 Typical Premium Estimates (2025)

| Monthly Benefit | Estimated Monthly Premium | Based On |

| $2,500 | $20–$40 | Young, healthy office worker |

| $4,000 | $40–$70 | Mid-30s, salaried professional |

| $6,000+ | $70–$120+ | Older, self-employed or tradie |

💬 Note: Always get a personalised quote — these are estimates only.

💡 Tips to Save on Premiums

● Choose a longer waiting period (e.g., 60–90 days)

● Select a 2-year benefit (good starting point)

● Insure only what you need (match expenses, not full income)

● Bundle with life/mortgage cover for discounts.

● Use a licensed NZ adviser for free, tailored advice

🔄 Example: John’s Savings Strategy

John earns $90,000/year. He chooses:

● 90-day waiting period

● 2-year benefit

● $4,000/month cover

This combo keeps him well protected — and his premium stays under $50/month.

Common Mistakes Kiwis Make When Choosing Income Protection

Getting income protection is smart, but choosing the wrong setup can cost you later. Here are the top pitfalls to avoid:

🚫 1. Underestimating Monthly Expenses

Many people only account for rent or mortgage. But what about food, insurance, school fees, and transport?

Fix: List out your real monthly essentials — don’t guess.

🚫 2. Picking the Cheapest Cover

Lower premiums can mean:

● Very short benefit periods

● Excluded health conditions

● Limited mental health coverage

Fix: Balance affordability with actual protection. Cheap isn’t helpful if it doesn’t pay when you need it.

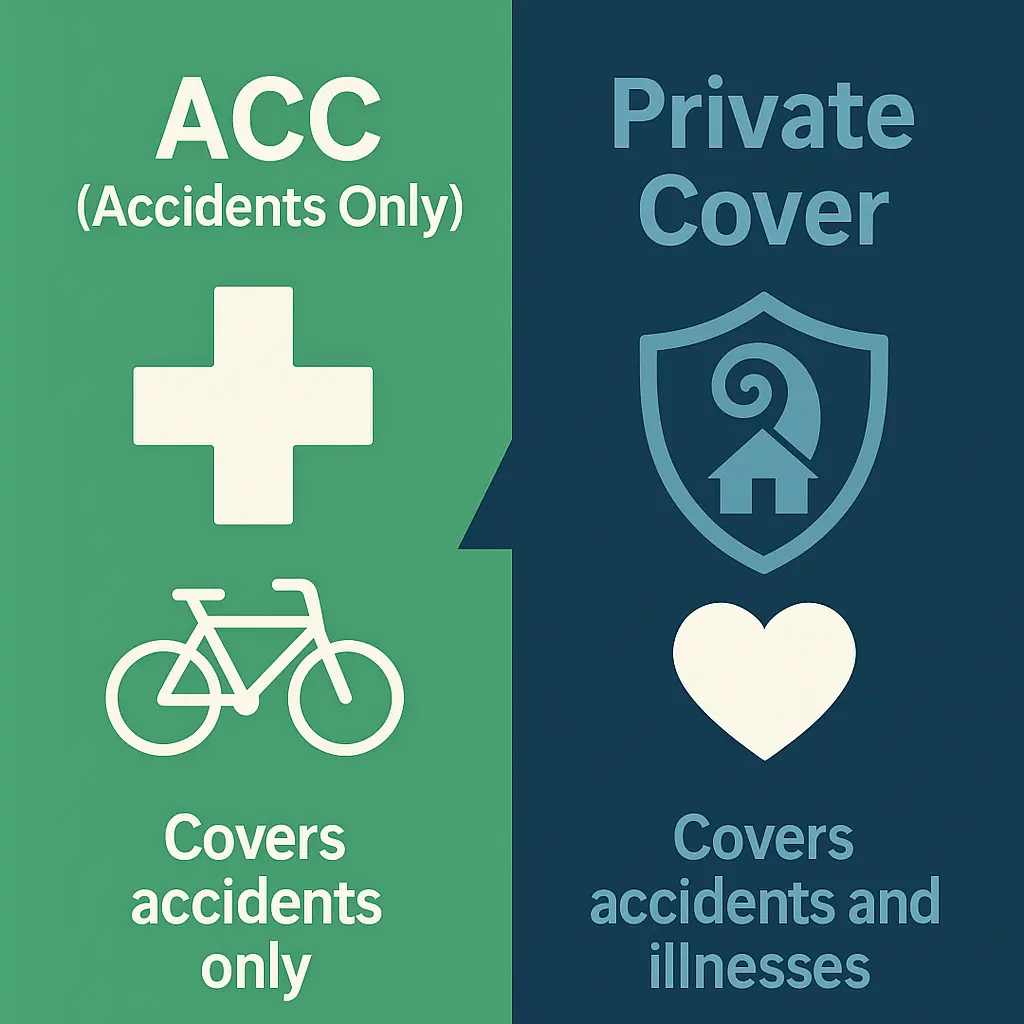

🚫 3. Assuming ACC Covers Everything

ACC covers accidents only. Most time off work in NZ is due to illness.

Fix: Make sure your private income protection policy includes illness and mental health — that’s the real gap.

🚫 4. Forgetting to Update Your Cover

Big life changes? You need to update your policy.

Examples:

● Got a new job?

● Bought a house?

● Had a child?

Fix: Review your cover every 12 months or after major life events.

🚫 5. Not Disclosing Medical History

This is the #1 reason claims are declined in New Zealand.

Fix: Always disclose your full history when applying. It may raise your premium, but it ensures you’re actually covered.

✅ Quick Recap: Mistake Fixes

| Mistake | Fix |

| Estimating expenses | List real monthly costs |

| Choosing the cheapest plan | Check coverage terms carefully |

| Relying on ACC alone | Add private cover for illness and mental health |

| Not updating the policy | Review yearly or after life events |

| Hiding medical conditions | Full disclosure = reliable claims |

👤 Real Kiwi Story: How Income Cover Helped Jordan

Jordan, 39, a freelance designer in Christchurch, was diagnosed with a rare nerve condition and couldn’t work for six months.

But because he had an agreed-value policy covering $5,000/month:

● He kept up with rent and groceries.

● He maintained subscriptions for his business

● He didn’t touch his savings.

💬 “It gave me breathing room to focus on recovery — not financial stress.”

💬 Pro Tip: Your income protection should grow with your life. It’s not “set and forget”.

FAQs: How Much Income Protection Cover Do You Really Need?

- Is 75% income cover the best choice for everyone?

Not always. It’s a common benchmark, but your real needs might be higher or lower depending on debt, lifestyle, and dependents. - Can I change my income protection amount later?

Yes — many policies offer a future increase option without medical checks. You can also request a reassessment if your income changes. - What if I have sick leave or an emergency fund?

You may not need full cover right away. Choose a longer waiting period or a smaller benefit amount to reduce premiums. - Do I need income protection if I already have ACC?

Yes — ACC only covers accidents. Income protection includes illnesses and mental health, which account for most time off work. - How is my cover calculated if I’m self-employed or have a variable income?

You’ll need to show income evidence from the past 12 months. If your income fluctuates, an “agreed value” policy gives more certainty.

✅ Final Thoughts: Don’t Guess — Get the Cover That’s Right for You

Life can change in an instant. Whether it’s an illness that keeps you off work for months or a long recovery from injury, your income is what holds everything together — from your home to your daily essentials.

Income protection cover in NZ gives you the confidence that even if you can’t work, your bills can still be paid, your family supported, and your lifestyle preserved.

Here’s what we’ve learnt:

● Most Kiwis underestimate how much income protection they need.

● The ideal cover = essential expenses × 1.25.

● 75% of your pre-tax income is the typical limit (but you may need less).

● ACC doesn’t cover illness, and that’s the biggest reason people miss work.

● Real people like Jordan and Sarah have relied on their cover to stay afloat

Learn more about policy fundamentals.

🧭 What Should You Do Now?

✅ Step 1: Work out your essential monthly expenses.

✅ Step 2: Add a buffer (around 25%) for peace of mind.

✅ Step 3: Compare that with the 75% cap and check what you’re eligible for.

✅ Step 4: Talk to a licensed NZ adviser — especially if you’re self-employed or have fluctuating income

📣 Ready to Find the Right Cover?

Use our free comparison tool to:

●🔍 Estimate how much income protection cover you need

● 🔄 Compare quotes from trusted NZ providers

●💬 Chat with licensed Kiwi advisers — with no pressure or hidden fees

👉 Compare NZ Income Protection Options Now

🛡️ Protect your income. Protect your lifestyle. Protect your future.

{kind=link}

{kind=link}

{kind=link}

{kind=link}