How to Claim Income Protection Insurance in New Zealand: 2025 Guide

With thousands of income protection claims filed in New Zealand each year, understanding how the system works is more important than ever.”If you’ve invested in income protection insurance, you’re likely aware of its essential role in securing financial stability during challenging times. But when the unexpected happens—whether due to illness, injury, or other circumstances—knowing precisely how to claim income protection insurance can significantly influence your experience. Timely and accurate claims submission speeds up the process and maximises your chances of approval, helping you maintain financial peace of mind when it matters most.

Income protection insurance is designed to replace a portion of your income if you’re temporarily unable to work due to illness or injury. It acts as a safety net, providing regular payments so you can continue to manage essential expenses such as mortgages, bills, and daily living costs. Understanding the claim process thoroughly ensures you receive these critical benefits without unnecessary delays.

This comprehensive guide will walk you through each step of the income protection claim process. You’ll learn:

- Exactly when and how to lodge a claim.

- What essential documentation do you need?

- How the Accident Compensation Corporation (ACC) interacts with your insurance claim.

- Practical tips to overcome common challenges and avoid potential claim rejections.

- Income protection claims statistics and insights from recent New Zealand data.

- A side-by-side comparison of popular insurance providers like KiwiCover, OneChoice, AIA, and Fidelity Life.

Ready to dive deeper? This article will show you exactly how to claim income protection insurance in New Zealand—step by step.

Tip: Always review your policy details regularly so you’re familiar with the terms and conditions before making a claim. If you haven’t yet chosen a policy or are considering switching, now’s a perfect time to Compare Now! to find the best fit for your needs.

Want to refresh your understanding of income protection? Check out our detailed article: What is Income Protection Insurance?.

Understanding Income Protection Insurance

Income protection insurance is specifically designed to provide financial assistance if you’re temporarily unable to work due to illness or injury. Typically, this insurance pays out a monthly benefit, helping you meet essential living costs and financial commitments, thus offering significant peace of mind during tough times. This section will help you understand the basics before you learn how to claim income protection insurance in detail.

Key Benefits of Income Protection Insurance

- Financial Stability: Regular monthly payments ensure that your daily living expenses and commitments, like mortgages and bills, are met even if you cannot work.

- Peace of Mind: Knowing your financial responsibilities are covered lets you focus entirely on your recovery.

- Customisable Options: Policies can be tailored to fit your income needs and lifestyle.

Income Protection vs Other Insurance Types

Understanding how income protection insurance compares to other insurance types can clarify why it’s crucial:

- Health Insurance: Covers medical treatments but doesn’t provide income replacement.

- Life Insurance pays a lump sum to your beneficiaries upon your death, but it doesn’t help if you’re temporarily disabled or ill.

- Critical Illness Insurance: Provides a lump sum upon diagnosis of specific severe conditions but not ongoing monthly income.

Common Misconceptions

- “ACC Covers Everything”: ACC only covers accidental injuries and provides limited support for illnesses, making income protection essential.

- “It’s Expensive”: Premiums are often affordable, and costs can be managed by adjusting coverage or waiting periods.

- “Self-Employed Individuals Don’t Qualify”: Income protection is particularly valuable for self-employed individuals, offering income stability during health setbacks.

Tip: Regularly discussing your coverage details with your provider ensures your policy aligns with your evolving financial needs. Ready to secure your financial future?

When to Make a Claim

Understanding how to claim income protection insurance at the right time is key to avoiding unnecessary delays or rejections. You should consider lodging a claim when you cannot work due to a health-related event, such as an illness, injury, or mental health issue.

Conditions Under Which You Can Claim:

- Serious Illness: If you’ve been diagnosed with a medical condition such as cancer, heart disease, or stroke, and it prevents you from working, you’re likely eligible to claim.

- Accidental Injury: Injuries from accidents, whether at home, work, or elsewhere, that leave you unable to perform your regular job duties.

- Mental Health Conditions: Conditions such as severe anxiety, depression, or stress-related disorders that impair your ability to work.

- Surgery or Recovery Period: Recovery from major surgeries, even planned ones, can qualify you to claim if it prevents regular employment.

Common Exclusions and Misunderstandings:

While income protection insurance provides essential financial support in various circumstances, it’s also crucial to understand what’s typically excluded from most standard policies:

- Redundancy or Job Loss: Income protection insurance does not cover job loss due to redundancy, business closure, or general unemployment.

- Pre-existing Conditions: Conditions you had before taking out the insurance are often excluded or have waiting periods.

- Minor Injuries or Short-Term Illnesses: Some policies include waiting periods—often between 30 to 90 days—meaning short-term absences might not qualify for immediate claims.

Insightful Tip:

Always check your policy documents or discuss them directly with your insurer to clearly understand all terms, conditions, and exclusions. This prevents unpleasant surprises and ensures you’re adequately prepared when a claim becomes necessary.

Read our article about redundancy. Learn why you need it.

For further clarity, you can explore how ACC (Accident Compensation Corporation) complements your insurance for accidental injuries by visiting ACC’s official website.

If you’re unsure whether your policy adequately covers your needs or want to compare options, don’t delay—secure peace of mind today.

Preparing to Lodge a Claim

Before you learn how to claim income protection insurance, you need to understand what documentation and preparation steps matter most.. Proper preparation ensures your claim progresses smoothly, reducing the chance of delays or potential rejections due to incomplete or inaccurate details.

Essential Documentation You’ll Need:

- Completed Claim Form:

Obtain this from your insurer’s website or directly from your case manager. Fill it out thoroughly, providing clear and precise information to avoid delays. Some insurers in New Zealand also offer phone support to guide you through filling out the claim form, especially if you’re unsure about medical or financial documentation. - Policy Number and Details:

Keep your insurance policy documents handy. You’ll need your policy number and specific details about your coverage. - Medical Evidence:

Comprehensive medical evidence is crucial. Include:

○ Doctor’s certificates clearly stating your condition and inability to work.

○ Hospital discharge summaries or medical reports.

○ Any specialist reports supporting your diagnosis and ongoing treatment?

- ACC Claim Information (if applicable):

If your claim involves an injury covered by the Accident Compensation Corporation (ACC), ensure you provide the relevant claim details and documentation from ACC. Your insurer will require this information to evaluate and coordinate your benefits effectively. - Income Verification Documents:

Depending on your employment status, include:

○ Employees: A letter or certificate from your employer detailing your pre-disability income, usually covering the previous 12 months.

○ Self-employed: Recent tax returns, financial statements, or other official income verification documents from the IRD.

- Additional Documentation (based on benefit type):

Depending on the specific conditions outlined in your insurance agreement, some policies might request extra documents such as bank statements or additional financial records.

Importance of Accurate and Complete Information:

Incomplete or inaccurate information can delay your claim approval significantly. Insurers require thorough documentation to verify eligibility and correctly assess the benefits payable. Always double-check the accuracy of your submitted documents, clarify any uncertain points directly with your insurer, and promptly respond to any follow-up requests.

Insightful Tip:

Maintain a personal file or digital folder dedicated solely to your claim documents. This ensures immediate access to all necessary information, simplifies communication, and speeds up the claims process.

Still uncertain about your current policy’s coverage or requirements? Consider reviewing and comparing alternatives to ensure your income protection plan matches your exact needs. Compare Now to find the best options for comprehensive protection.

Related Reading:

Deepen your understanding by exploring our dedicated article, Income Protection Insurance Explained.

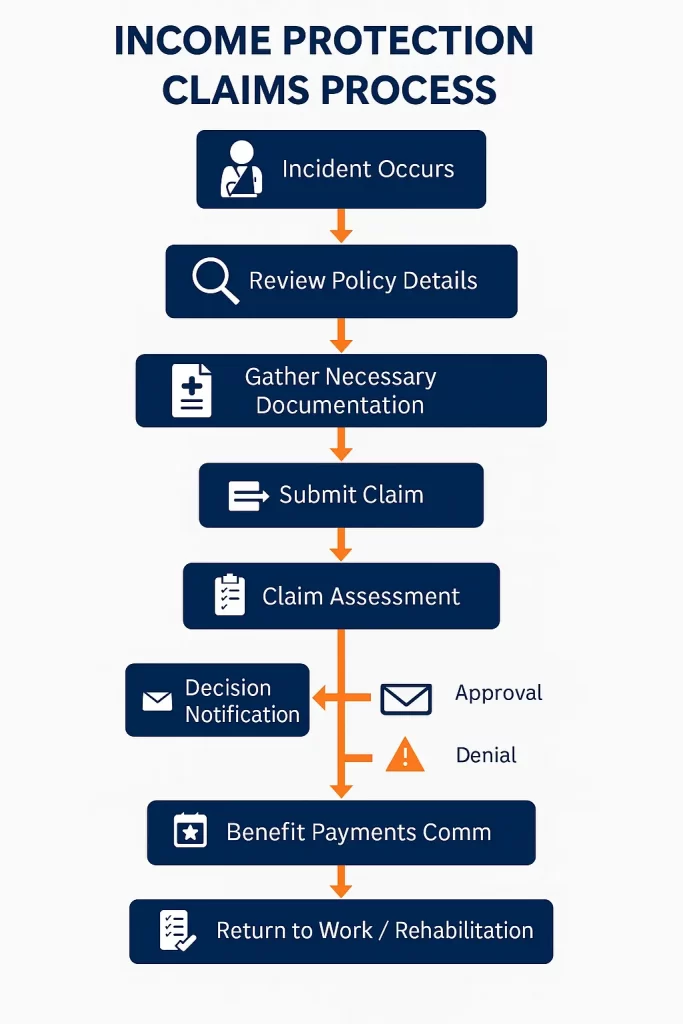

The Claims Process Explained

Let’s walk through how to claim income protection insurance from start to finish, with practical insights, ensuring you know exactly what to expect and when.

🔹 Real-Life Example:

Sarah, a freelance designer from Wellington, suffered a repetitive strain injury that required surgery and three months off work. She submitted her completed claim form, specialist’s letter, and income verification documents within two weeks of her diagnosis. Because everything was accurate and submitted on time, her insurer began payments shortly after the 30-day waiting period.

Step-by-Step Guide to the Claims Process:

Step 1: Submission of the Claim

Once you’ve gathered all necessary documentation (claim form, medical evidence, income verification, and relevant ACC details), submit your claim directly to your insurer. Most insurers accept claims via email, online portals, or by mail. It’s wise to confirm receipt of your claim by contacting your insurer soon after submission.

Step 2: Assignment of a Dedicated Case Manager

After your claim is received, your insurer will typically assign you a dedicated Case Manager. This person will be your primary contact throughout your claims journey. They’ll keep you informed, guide you through any necessary steps, and answer questions regarding your claim status.

Step 3: Assessment of Your Claim

The insurer’s assessment team will carefully review your submitted documentation and medical evidence. During this phase, the insurer might request further details or clarification, such as:

- Additional medical reports or specialist assessments.

- Further income documentation.

- Clarification regarding your job duties and responsibilities.

- Updates on any ongoing treatment or rehabilitation plans.

Promptly providing requested information will help prevent delays in processing your claim.

Step 4: Decision and Communication of the Outcome

Upon completing their assessment, the insurer will formally communicate their decision to you, typically through your Case Manager via phone, email, or formal letter. The decision will either approve your claim, specifying your benefit amount and payment schedule, or provide clear reasons if your claim is declined or requires further investigation.

Step 5: Commencement of Benefit Payments

Your insurer will begin regular payments if approved according to your policy terms. Payments usually start after the waiting period specified in your policy, often ranging from 30 to 90 days after you stop working.

Typical Timelines:

- Initial Submission to Case Manager Assignment: 1-5 business days.

- Assessment Period: It usually takes 2-6 weeks, depending on the complexity of your case and the documentation provided.

- Decision Communication: Typically within 4-8 weeks of initial claim submission.

- Commencement of Payments: Immediately after the specified waiting period (check your policy).

What to Expect at Each Stage:

- Regular updates from your Case Manager.

- Possible requests for additional information.

- Transparent explanations of all decisions and any policy details involved.

Insightful Tip:

Maintain regular communication with your Case Manager. Proactively asking about progress and promptly responding to requests can significantly accelerate your claim’s progression.

Not sure your policy’s waiting period or benefits match your current financial needs? Take the time now to ensure your coverage provides adequate protection. Compare Now to explore better options.

Ongoing Requirements During the Benefit Period

Once your income protection claim has been approved and your benefit payments have commenced, you must fulfil essential ongoing responsibilities. Staying informed and proactive about these requirements will ensure your payments continue smoothly, helping you remain financially secure throughout your recovery period.

Monthly Obligations

Medical Certificates Completion

Each month, your insurer will typically require you to provide updated medical certificates or reports from a registered medical practitioner. These documents confirm your ongoing inability to work and detail the current status of your recovery. Promptly submitting these certificates ensures no disruption to your benefit payments.

🔹 Real-Life Scenario:

James, a high school teacher from Christchurch, went on claim for clinical depression. Each month, his GP completed updated medical certificates and James submitted a short activity declaration. Because he maintained excellent communication with his insurer, his payments continued without interruption.

Individual Declaration of Activities

You may also need to submit monthly declarations that detail your daily activities and overall health status. These declarations help insurers verify that your claim remains valid, providing transparency about your condition and daily routine.

Reporting Changes in Work Status or Income

It is vital to immediately inform your insurer of any changes in your work situation or income status during the benefit period. Common scenarios include:

- Returning to work part-time or on reduced duties.

- Receiving payments from ACC, employer sick leave, or other income sources.

- Start a new job, even if it differs from your previous role.

Factors That May Affect Your Benefit Payments

Several factors can influence the continuity and amount of your income protection payments, including:

- Partial Work Capability: If you can work part-time, your insurer may adjust your benefit accordingly.

- Receipt of ACC Payments: Benefits may be reduced if you receive payments from the Accident Compensation Corporation.

- Changes in Medical Condition: Significant improvement or deterioration in your medical condition could alter benefit assessments and payments.

- Non-compliance: Failure to provide the required monthly documentation or notify about changes promptly could pause or stop payments.

Insightful Tips for Smooth Benefit Management:

- Keep all medical appointments and maintain consistent communication with your healthcare providers.

- Create a reminder system (calendar alerts, digital reminders) for monthly documentation submissions.

- Always proactively inform your Case Manager of any employment or health status changes to avoid unexpected payment adjustments.

Are you concerned about how well your policy handles these ongoing requirements? Now’s an excellent opportunity to reassess your options. Compare now to ensure your income protection aligns with your current needs.

Rehabilitation and Returning to Work

Income protection insurance doesn’t just offer financial support, but is designed to help you gradually return to the workforce when ready. As your recovery progresses, insurers often provide access to rehabilitation programs and occupational support to ease the transition back into employment, especially if your former role is no longer suitable.

Support from Your Case Manager

Your assigned Case Manager plays a pivotal role during this stage. They’ll:

- Regularly check in on your recovery progress.

- Coordinate with healthcare providers to understand your current capabilities.

- Initiate conversations about a realistic and supported return-to-work timeline.

- Help tailor a rehabilitation plan that aligns with your physical and mental readiness.

These plans are personalised and consider medical advice and your specific job responsibilities or limitations.

Occupational Specialist Involvement

When needed, your insurer may engage occupational specialists to:

- Assess your work capacity and environment.

- Recommend workplace modifications to accommodate your recovery.

- Identify roles or tasks that are better suited to your post-recovery abilities.

- Develop a return-to-work strategy that prioritises your health and long-term well-being.

This collaborative approach ensures that your transition back to work is safe, sustainable, and well-supported.

Vocational Retraining Options

Vocational retraining may be offered if returning to your previous job isn’t feasible due to lasting physical or cognitive limitations. This could include:

- Enrolment in short courses or certifications.

- Skills training for alternative industries.

- Career counselling to explore new, suitable employment paths.

Some insurers, like AIA with its 360 Care program, are known to offer extended recovery services and job-readiness support as part of their claim benefits.

🔹 Case Example:

Anita, a project manager, returned to work part-time after spinal surgery. Her insurer arranged an occupational therapist to help adjust her workstation and developed a gradual return-to-work plan. Her benefit was adjusted to supplement her part-time income until she was fully recovered.

Tip for a Successful Return:

Stay engaged in the process and voice any concerns or limitations early. Your feedback will help shape a plan that works for you, not against you. Also, document everything related to your rehabilitation for easier communication and compliance with your insurer.

Thinking about whether your current policy includes these types of rehabilitation benefits? Don’t leave it to guesswork—Compare Now and find out which providers offer the most comprehensive post-claim support.

Common Challenges and How to Overcome Them

Even with a comprehensive income protection policy, navigating the claims process isn’t always smooth sailing. Several common hurdles can delay or derail claims if you’re not well-prepared. The good news? Most of these challenges are avoidable with proactive planning and a clear understanding of your responsibilities.

Common Issues Claimants Face

- Delays in Obtaining Medical Documentation

Doctors and specialists are busy, and medical documentation can take time, especially if additional reports or updates are needed during the benefit period. This often causes processing delays. - Incomplete or Inaccurate Information

Submitting forms with missing fields, incorrect policy details, or outdated income records is a fast track to stalled claims. Insurers rely on precise documentation to assess eligibility and calculate benefits. - Misunderstanding Policy Terms or Waiting Periods

Many claimants assume income protection starts immediately after stopping work. However, most policies include a waiting period (commonly 30 to 90 days) before benefits begin. Others may misinterpret exclusions, such as coverage for redundancy or pre-existing conditions. - Lack of Communication

Not staying in touch with your Case Manager—or failing to update them about changes in condition, income, or employment—can lead to confusion, missed documentation deadlines, or payment pauses.

Tips to Navigate and Overcome These Challenges

✅ Be Proactive With Medical Providers

Let your doctor know in advance what documentation is needed and follow up regularly. Ask if their practice can complete the forms electronically for faster submission.

✅ Triple-Check Your Documents

Before lodging a claim, review all paperwork for completeness and accuracy. Missing a signature, date, or medical clarification can set you back weeks.

✅ Understand Your Policy

Familiarise yourself with your policy’s fine print. If needed, ask your insurer for a plain-English summary of your waiting period, benefit amount, exclusions, and any offsets (like ACC or part-time income).

✅ Stay Organised

Keep all claim-related emails, receipts, forms, and medical records in one digital folder. This will make it easier to respond quickly to insurer follow-ups.

✅ Maintain Regular Contact

Check in with your Case Manager weekly (or as advised) and notify them of any updates—even if you think they’re minor.

Tip:

Ask your insurer at the start for a checklist of exactly what’s required and when. Meeting deadlines and responding quickly shows you’re engaged and responsible—a positive signal during claim reviews.

Are you still unsure whether your current policy offers clear guidance or responsive support? Take action today to ensure your plan won’t disappoint you when it matters most.

Income Protection Claims Statistics in New Zealand

Understanding how income protection insurance performs in real life, not just in policy documents, can give you a crucial perspective. Claims statistics provide insight into how often people claim, how long benefits last, and why some claims get denied. These figures not only set realistic expectations but also help you choose the right insurer based on actual outcomes.

Recent Data on Income Protection Claims

While New Zealand-specific data on income protection insurance is not as publicly robust as life insurance, industry insights and insurer disclosures provide a valuable snapshot. According to the Financial Services Council (FSC NZ) and reports from insurers like AIA and Fidelity Life:

- Thousands of income protection claims are lodged annually in New Zealand, with a significant portion stemming from mental health-related conditions and musculoskeletal injuries.

- Top reasons for claims:

○ Depression and anxiety

○ Back injuries and chronic pain

○ Cancer and cardiovascular conditions

📊 Fidelity Life’s 2023 claims snapshot reported that over 50% of its disability claims were related to mental health, showing a growing trend in psychological claims.

Approval Rates and Claim Denials

Most reputable insurers in New Zealand have relatively high claim approval rates:

- Approval rates typically range between 85% and 95% for valid income protection claims.

- Common reasons for declined claims include:

○ Non-disclosure of pre-existing conditions.

○ Insufficient medical documentation.

○ Attempting to claim for uncovered situations like redundancy or short-term illnesses during the waiting period.

Trends in Claim Durations and Payout Amounts

- Depending on the condition and occupation, the average duration of a claim ranges from 3 months to over 1 year.

- Monthly benefit payouts can vary significantly based on income level, but most policies cover up to 75% of pre-disability earnings.

- Mental health claims have longer recovery periods, leading to extended payout durations.

Insightful Tip:

When choosing an insurer, look for those with transparent claims data, high approval rates, and a track record supporting mental health conditions. These metrics are just as important as pricing when you’re comparing policies. These statistics highlight why understanding how to claim income protection insurance successfully can make a big financial difference.

👉 Ready to review policies with proven claims performance? Choose the most likely to deliver when you need it.

Sources for Statistics:

- Financial Services Council NZ

- AIA NZ and Fidelity Life public claims disclosures

Comparing Income Protection Insurance Providers

When choosing an income protection insurance provider, it’s essential to go beyond pricing and assess the quality of support you’ll receive when you need it most. Let’s compare four of New Zealand’s leading insurers—AIA, Asteron Life, Fidelity Life, and Partners Life—to help you evaluate the right fit for your needs.

Major Providers Overview

Here’s a quick snapshot of each insurer:

- AIA New Zealand

A well-established global insurer with local presence. Offers one of the most structured and transparent claims processes, bolstered by its 360 Care Program that supports rehabilitation and return-to-work services.

- Asteron Life

A trusted brand with a reputation for clear communication and efficient claims handling. Known for supporting advisers and policyholders throughout the claims lifecycle, with a strong focus on prompt updates and client advocacy.

- Fidelity Life

100% New Zealand-owned, Fidelity Life combines local insight with strong personal service. Their Claims Hub provides an easy, guided process, and their high claim acceptance rate reflects their customer-first approach.

- Partners Life

An innovative insurer focused on delivering comprehensive coverage and high-value extras. Partners Life is known for flexible underwriting, strong adviser partnerships, and transparent claims performance reporting.

Comparison of Claim Processes & Support

| Provider | Claim Process Experience | Support Services & Unique Features |

| AIA NZ | Streamlined & digital-friendly | 360 Care Program, dedicated Case Managers, return-to-work rehab |

| Asteron Life | Communicative & fast-tracked | Adviser-driven support, clear client updates, flexible engagement |

| Fidelity Life | Personalised & transparent | NZ-based service team, online Claims Guide, strong acceptance stats |

| Partners Life | Detailed & adviser-supported | Transparency in claims stats, wellness benefits, and flexible terms |

Insightful Tip:

When comparing providers, look at the whole picture—claims support, transparency, and customer outcomes, not just monthly premiums. A cheaper policy may cost more in the long run if the claims process is confusing or slow.

Want to see how these providers stack up based on your specific needs and income?

👉 Compare Income Protection Insurance Providers now and secure peace of mind for your future.

Need help narrowing down your options?

Frequently Asked Questions (FAQs)

Navigating income protection insurance claims can come with a lot of uncertainty. Here are answers to some of the most frequently asked questions to help you feel confident and informed throughout the process.

Can I claim if I’m self-employed?

Self-employed individuals can claim income protection, provided your policy is active and meets the criteria. You must provide financial documentation such as tax returns and IRD assessments to verify your income. Income protection is especially valuable for the self-employed since you don’t receive sick leave or employer-paid benefits.

How does ACC affect my income protection claim?

If your time off work is due to an accident covered by ACC, your income protection insurer will likely reduce (or “offset”) your benefit payments by the amount you receive from ACC. Sharing all ACC documentation with your insurer is essential to avoid overpayment or delays.

What happens if I return to work part-time?

Most insurers allow for partial benefits if you return to work part-time or in a reduced capacity. Your payments may be adjusted based on how much you’re earning. Always notify your insurer of any return-to-work arrangements to comply with your policy.

Are mental health conditions covered?

Yes, many income protection policies cover claims related to mental health, including depression, anxiety, and stress-related disorders. However, you may be subject to specific terms, such as exclusions or waiting periods. It’s best to check your policy wording or contact your insurer for details.

How long does it take to receive payments?

Once your claim is approved, payments generally start after your policy’s waiting period, usually between 30 and 90 days from the date you became unable to work. The processing time also depends on how quickly you submit documentation and how complex your case is.

What’s the easiest way to learn how to claim income protection insurance?

Review your insurer’s claims guide and follow a structured resource like this article. Having all documents prepared before filing can dramatically speed up your approval process.

Still have questions about how your policy stacks up?

👉 Compare Now and get the clarity you need to make confident, informed choices about your financial safety net.

Conclusion

Filing an income protection insurance claim doesn’t have to be complicated, especially when you know what to expect. In this guide, we’ve walked you through the entire claims process: from understanding when and how to claim, gathering the right documentation, working with your case manager, to managing ongoing requirements and navigating potential challenges.

We’ve also shown how leading New Zealand providers like AIA, Asteron Life, Fidelity Life, and Partners Life approach claims, giving you a real-world perspective on customer support and satisfaction.

Key Takeaways:

- Start early: Don’t wait to lodge your claim. Timely submissions matter.

- Be prepared: Accurate documentation and regular communication with your insurer are key to faster approvals.

- Know your policy: Understanding your waiting period, exclusions, and support services gives you control over the process.

- Stay engaged: Keep up with medical updates, declarations, and rehabilitation requirements during your benefit period.

Income protection is more than a policy—it’s your financial safety net when life throws a curveball. But having the right provider makes all the difference.

Are you unsure if your current cover meets your needs or how other insurers compare?

Understanding your policy terms is a crucial first step if you’re researching how to claim income protection insurance effectively.

Knowing how to claim income protection insurance helps avoid the common pitfalls many first-time claimants face.

{kind=link}

{kind=link}

{kind=link}