How to Save on Income Protection Insurance Premiums in 2025

Why Income Protection Insurance Premiums Matter in NZ

Income Protection Insurance Premiums are a small price to pay when compared to the financial risk of losing your income. For many New Zealanders, their ability to earn an income is their greatest financial asset. If an illness or injury prevents you from working, it could cause major financial stress, with bills, mortgage payments, and everyday expenses continuing even if your income stops.

This is where income protection insurance becomes essential. A well-structured policy can cover up to 75% of your regular income, helping you and your family stay financially secure during difficult times.

It’s also important to know that ACC only covers injuries, not illnesses, and many of the most common reasons for income protection claims in NZ are illness-related.

The good news is:

👉 Smart policy design can significantly lower your Income Protection Insurance Premiums — without sacrificing essential cover.

In this article, you’ll learn:

✅ The core factors that influence premiums

✅ Proven ways to reduce costs

✅ Advanced strategies most articles miss

✅ How to structure your cover for maximum value

✅ Common mistakes to avoid

✅ Where to compare quotes easily — with no obligation

If you’re ready to start exploring your personalised options, you can Compare Now — it only takes a few minutes.

Understanding Income Protection Insurance Premiums

When it comes to saving money on your income protection insurance, understanding how Income protection insurance premiums are calculated is key.

Many New Zealanders overpay — not because they chose the wrong insurer, but because they didn’t structure their policy optimally.

What Factors Influence Your Premiums

Several key factors affect how much you’ll pay for your income protection insurance. The great news? Many of these can be adjusted to help you save.

✅ Age

- The older you are, the higher your premiums.

- Premiums rise sharply from age 40+.

✅ Occupation

- Low-risk jobs (office/professional) = cheaper

- High-risk (trades/manual labour) = more expensive

Example: A roofer may pay 2x what an accountant pays for the same cover.

✅ Health & Lifestyle

- Smokers pay 50–100% more

- Higher BMI or health conditions can add loadings

- Some hobbies can also affect premiums

Pro Tip:

💡 If you quit smoking or improve your health, ask for a policy review — you could save.

✅ Benefit Period & Amount

- Benefit period = how long the policy pays out (e.g. 2 years, 5 years, to age 65)

- Benefit amount = % of income insured

Shorter benefit period = lower premiums.

✅ Waiting Period

- The delay before payments start (4, 8, 13, or 26 weeks)

- Longer wait = cheaper premiums.

Example: Extending from 4 to 13 weeks can save 25–40%.

✅ Policy Structure (Level vs Stepped Premiums)

- Stepped premiums: cheaper at first, rise every year

- Level premiums: stay flat → cheaper long term.

Pro Tip:

💡 If you plan to keep coverage for 5+ years, level premiums usually save you money.

✅ CPI Indexing

- Increases your cover (and premiums) with inflation each year.

- You can opt out to keep premiums stable.

✅ Payment Frequency

- Annual payments often come with a 5–8% discount compared to monthly.

Core Strategies to Reduce Income Protection Insurance Premiums (Proven Tips)

When it comes to income protection insurance, smart policy structuring can make the difference between an expensive plan and one that’s both affordable and effective.

In this section, we’ll explore 10 proven strategies that financial advisers regularly use to help clients save 20-50% or more on their income protection premiums — all without sacrificing essential cover.

1. Extend the Waiting Period

How it works:

Your waiting period is how long you must be off work before benefits start — usually 4, 8, 13, or 26 weeks.

Why does it save?

✅ The longer you wait, the cheaper your premium.

Example:

Moving from a 4-week wait to a 13-week wait can cut premiums by 25-40%.

Pro Tip:

💡 If you have an emergency fund, ACC cover, or sick leave, this is one of the quickest ways to lower costs.

2. Shorten the Benefit Period

How it works:

Your benefit period is how long payments will continue if you can’t work (2 years, 5 years, or to age 65).

Why does it save?

✅ Shorter benefit periods = lower risk for the insurer = lower premiums.

Example:

A 2-year benefit period is typically 30-50% cheaper than “to age 65”.

Pro Tip:

💡 Many claims last less than 2 years — combine a shorter benefit period with trauma cover for long-term protection.

3. Lower the Benefit Amount

How it works:

You can choose to insure up to 75% of your income, but you may not need that much.

Why does it save?

✅ Lower benefit amount = lower premiums.

Example:

Reducing cover from 75% to 60% of income can save 15-25%.

Pro Tip:

💡 Focus on covering essential expenses, not your entire lifestyle spend.

4. Choose Level Premiums for Long-Term Savings

How it works:

✅ Stepped premiums start cheap, rise every year

✅ Level premiums stay constant — often cheaper over time

Example:

At year 10+, level premiums are usually 30-50% cheaper than stepped.

Pro Tip:

💡 If you’re under 40 or plan to keep your cover 5+ years, level premiums are a smart investment.

5. Remove CPI Indexing If Appropriate

How it works:

CPI indexing automatically increases your cover each year and your premiums.

Why does it save?

✅ Removing CPI can stop the annual 3-5% premium creep.

Pro Tip:

💡 If your income is stable (e.g., nearing retirement), you may not need CPI indexing anymore.

6. Bundle Policies with One Insurer

How it works:

✅ Combine income protection with life, trauma, or TPD insurance through the same provider.

Why does it save?

✅ Insurers offer 5-10% bundling discounts.

Pro Tip:

💡 Bundling also simplifies admin → one policy, one provider = easier at claim time.

7. Conduct Regular Policy Reviews

How it works:

Life changes — and so should your cover.

✅ Mortgage paid off?

✅ Kids finished school?

✅ New job?

Why does it save?

✅ Removing unneeded cover after life changes can save 20-30%.

Pro Tip:

💡 Review your policy every 1-2 years or after any major life event.

8. Use an Independent Adviser / Broker

How it works:

✅ Independent brokers compare policies across multiple insurers.

✅ Bank-sold policies are typically less flexible and more expensive.

Why does it save?

✅ Many clients save 10-20% or more by switching away from bank policies.

9. Pay Annually Instead of Monthly

How it works:

✅ Insurers offer 5–8% discounts for annual payment.

Pro Tip:

💡 If cash flow allows, pay annually — easy savings every year.

10. Take Advantage of Loyalty Discounts

How it works:

✅ Some insurers reward long-standing or claim-free customers with loyalty discounts over time.

Pro Tip:

💡 Ask your adviser if your insurer offers a loyalty or no-claim bonus — many Kiwis miss out because they simply never ask!

Advanced Strategies to Reduce Income Protection Insurance Premiums

Most articles stop at basic tips like extending the waiting period, but experienced advisers know that more advanced strategies can unlock even greater savings, often with zero downside.

Here’s a deeper look at 8 proven advanced tactics to lower your premiums, enhance your policy flexibility, and stay ahead of the curve.

👉 Want to see how these could apply to YOUR policy? Compare Now — personalise your savings today.

1. Use Wellness Programs and Health Incentives

Some NZ insurers (like AIA with AIA Vitality) offer wellness programs that reward a healthy lifestyle with premium discounts.

✅ Up to 5–15% immediate discount for joining

✅ Further discounts for ongoing participation (tracked via smart watches, medical checkups, gym visits)

Example:

A healthy 35-year-old office worker cut their premium from $85 to $72/month via AIA Vitality participation.

Pro Tip:

💡 If you already use Fitbit, Garmin, or Apple Watch, you’re halfway to qualifying.

2. Understand Occupation Risk Classifications — and If You Can Change

NZ insurers classify jobs into occupation risk categories, and this can have a major impact on premiums:

✅ Class 1 (office/professional) → lowest premium

✅ Class 4 (high-risk/manual labour) → highest premium

Why it matters:

If your job role has changed (e.g., moving from field to office-based), you may now qualify for a lower-risk category, → potential savings of 15–25%.

3. Tax Treatment of Income Protection Premiums (Self-Employed)

Self-employed Kiwis can often claim premiums as a business expense, making them tax deductible — if the policy is structured correctly (indemnity-style).

Example:

At a 33% tax rate → $200/month premium → after tax = approx $134/month net.

Pro Tip:

💡 Work with your adviser AND accountant to structure the policy correctly — and check IRD guidance here: IRD

4. Employer-Sponsored Income Protection — Cheaper Group Rates

Some larger NZ employers offer group income protection schemes:

✅ 20–40% cheaper than retail premiums

✅ Often, no personal underwriting required

✅ Cover can sometimes be continued privately if you leave the employer

Pro Tip:

💡 Ask your HR/benefits team — many people don’t realise their employer offers this!

5. How Credit Score or Claims History Can Affect Premiums

Insurers sometimes do a soft credit check as part of underwriting, and a strong credit profile can improve acceptance and terms.

✅ A clean credit record may lead to more favourable underwriting and avoid loadings.

✅ Claims history also matters — frequent past claims can trigger loadings or exclusions with some insurers.

Pro Tip:

💡 If your credit score has improved, or you’ve been claim-free for several years, ask your adviser if you now qualify for better terms.

6. How to Negotiate Premiums When Renewing or Switching Insurers

✅ Premium increases at renewal are not always set in stone.

✅ A good adviser can:

✅ Negotiate loyalty discounts

✅ Restructure the cover for savings

✅ Shop competing providers

Example:

One NZ client switched from a bank-sold policy → leading to $600/year savings and better cover terms.

Pro Tip:

💡 Never auto-renew without checking market rates first!

7. Combining Trauma, TPD, and Income Protection to Lower Total Cost

✅ Layering cover is often cheaper than over-relying on income protection alone:

✅ Trauma + TPD cover can provide lump sums, allowing you to:

✅ Choose shorter income protection benefit periods

✅ Lower your income protection benefit amount → saving $$

Example:

One client reduced their income protection premium by 40% by adding trauma cover and reducing the income protection benefit period.

Pro Tip:

Ask an adviser to help you design a layered protection strategy that gives more cover for less overall cost.

Special Situations — Tailored Tips to Save on Income Protection Premiums

Not everyone needs the same type of income protection. Your career stage, income, and personal situation all affect how you should structure your cover and how you can save.

Here are specific tips for common situations Kiwis face.

1. Tips for Freelancers, Contractors, and Gig Workers

✅ Income often fluctuates — so flexible, indemnity-style cover is key.

✅ Extend waiting period → lower cost.

✅ Consider trauma cover to complement income protection.

✅ ACC CoverPlus Extra may also help: ACC CoverPlus Extra

Pro Tip:

💡 Many freelancers can cut premiums by 30–50% with the right policy structure.

2. Tips for Self-Employed Business Owners

✅ Structure premiums to be tax deductible (check with your accountant).

✅ Consider adding Business Expenses Insurance to cover fixed business costs.

✅ Use level premiums if planning to stay self-employed long term.

Pro Tip:

💡 Annual payment = easier tax deduction + 5–8% savings.

3. Tips for Young Professionals (Under 35)

✅ Lock in level premiums now — huge savings long term.

✅ Start with a lower benefit amount, then increase as your income grows.

✅ Use a 13-week waiting period if you have sick leave or savings.

Example:

A 28-year-old can lock in $50/month level premiums that could cost $150+ later if they delay.

4. Tips for Pre-Retirees (Age 50+)

✅ Premiums rise fast in your 50s — time for a policy review.

✅ Do you still need a benefit period to age 65? If not, shortening it can save $1,000+ per year.

✅ Consider removing CPI indexing.

✅ Trauma cover can sometimes provide better value at this stage.

Pro Tip:

💡 Many pre-retirees are over-insured — review your policy!

5. Tips for Those with Pre-Existing Conditions

✅ Not all insurers treat pre-existing conditions the same — shop the market.

✅ Group cover (via employer) can sometimes bypass full underwriting.

✅ Layer trauma + income protection for flexibility.

✅ After 2–5 years of stability, some conditions can be reassessed and loadings removed.

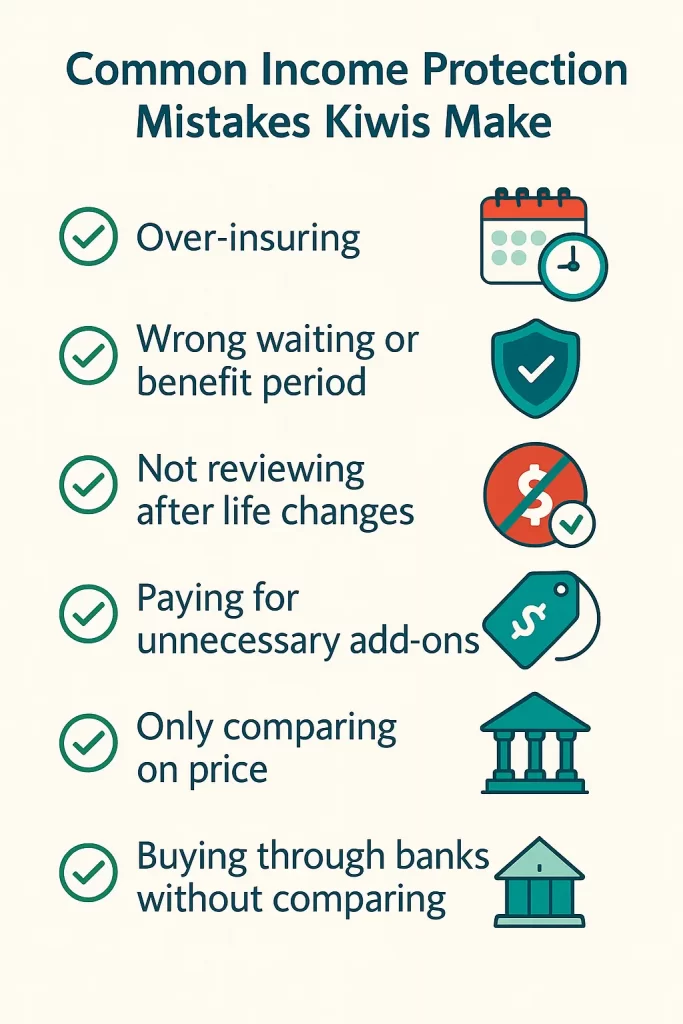

Common Mistakes to Avoid

Even smart Kiwis can accidentally pay too much or end up with cover that doesn’t suit them.

Here are the most common mistakes about Income Protection Insurance Premiums and how you can avoid them.

Over-Insuring (Buying More Cover Than You Need)

✅ Many people default to 75% cover, but don’t account for:

✅ Emergency savings

✅ Partner’s income

Choosing the Wrong Waiting or Benefit Period

✅ Too short a waiting period → high premiums.

✅ Too long a benefit period when you don’t need it → unnecessary cost.

Not Reviewing Policies After Major Life Changes

✅ Big changes = time to review:

✅ Paid off mortgage

✅ Kids grow up

✅ Career change

✅ Income change

Pro Tip:

💡 Failing to review could mean you’re paying $1,000+ per year more than needed.

Paying for Unnecessary Add-Ons

✅ Some add-ons sound good but aren’t always worth the cost:

❌ Premium waivers

❌ Redundant CPI indexing

❌ Reinstatement benefits

Pro Tip:

💡 Review add-ons with an adviser — strip out what you don’t truly need.

Only Comparing Policies on Price (Not Features)

✅ Cheap is good — but quality matters too:

✅ Strong definitions of disability

✅ Partial disability cover

✅ Mental health cover

✅ ACC offsets

FAQs — Income Protection Insurance Premiums

1. Is income protection insurance tax deductible in NZ?

If you’re self-employed or a contractor, your income protection premiums can often be tax deductible, as long as the policy is structured correctly. Employees generally can’t claim this deduction.

2. How much should I expect to pay per month?

Premiums vary, but most Kiwis pay between $30 and $350 per month, depending on age, occupation, benefit period, waiting period, and health. Using the right policy structure can save you a lot.

3. What is the average saving from extending the waiting period?

Extending your waiting period from 4 weeks to 13 weeks can typically reduce your premiums by 25% to 40%, especially if you have sick leave, savings, or ACC cover to rely on initially.

4. Can I change my policy later?

Yes — you can adjust your waiting period, benefit period, benefit amount, CPI indexing, or even switch insurers at any time if a better option becomes available.

5. What happens if my occupation changes?

If you move to a lower-risk job (such as from manual work to office-based), you may qualify for cheaper premiums, but you need to notify your adviser or insurer to request the change.

6. Is it worth switching insurers?

Often yes — newer policies can offer stronger features, loyalty discounts, and lower premiums compared to older or bank-sold policies. Many Kiwis save hundreds per year by switching.

👉 Want personalised savings tips or a free policy review?

Conclusion

Saving on income protection insurance premiums doesn’t have to be difficult.

By making a few smart adjustments — like choosing the right waiting period, benefit period, and premium structure — you can often save 30–50% without losing valuable cover.

It also pays to review your policy regularly and work with an independent adviser who can help you find the best options.

✅ Small changes today can save you thousands in the years ahead.

👉 If you’d like help reviewing your policy or comparing current deals, you can start here → Compare Now — it’s free, quick, and there’s no obligation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}