Income Protection vs Trauma Insurance: 2025 Comparison Guide

In New Zealand, ACC covers accidents but leaves a significant gap when it comes to serious illnesses and disabilities related to sickness. That’s why comparing income protection vs trauma insurance is so important—each policy fills a different financial need when you can’t work or face a critical health event.

Key Takeaways

- Understand how income protection vs trauma insurance differ in payout structure: ongoing salary replacement versus a one-off, tax-free lump sum.

- Learn which conditions each policy covers and how eligibility criteria vary.

- Discover how waiting periods and benefit durations influence your protection.

- Discover the key factors that influence premium costs for both income protection and trauma insurance.

- Review the main pros and cons of each policy, including tax implications and claim requirements.

- Explore cost-comparison scenarios to gauge real-world premium differences.

- Use our decision framework to determine whether you need income protection alone, trauma insurance alone, or a combination of both.

- Delve into lesser-discussed topics—business continuity, key-person coverage, and policy reviews—to optimise your protection strategy.

- Follow a step-by-step guide to the claims process for income protection and trauma insurance.

Ready to compare live quotes from multiple insurers for quick, no-obligation pricing.

Definitions & Core Features

What Is Income Protection?

Income protection is a disability policy that replaces a portion of your pre-tax income when illness or injury prevents you from working. In most New Zealand policies, you can select a benefit level of up to 75% of your gross salary, subject to a monthly cap determined by the insurer. You’ll also choose a waiting period—commonly 4, 8, 13, or 26 weeks, or up to 2 years—before benefits commence. After the waiting period ends, monthly payments continue until you recover, return to work, reach age 65 or 70, or exhaust the maximum benefit period.

Key features include:

- Benefit Percentage & Cap: Typically up to 75% of gross earnings, capped (e.g., $30,000 NZD/month with some insurers).

- Waiting Period: Options commonly range from 4 weeks to 2 years; longer waits reduce premiums.

- Benefit Period: Usually 2 years, 5 years, to age 65, or to age 70.

- Tax Treatment: Premiums may be tax-deductible for self-employed or company directors; benefit payments are taxed as income.

For more on what income protection does and how it works in the Kiwi market, see What Is Income Protection Insurance in NZ?.

What Is Trauma Insurance?

Trauma insurance (also called critical illness cover) pays a one-off, tax-free lump sum upon diagnosis of a specified critical illness or condition, such as cancer, heart attack, stroke, or Alzheimer’s disease. Instead of replacing income over time, it provides immediate capital that can be used for medical bills not covered by ACC, mortgage payments, specialist treatment, or lifestyle adjustments.

Key features include:

- List of Covered Conditions: Typically around 40 – 50 specified illnesses (e.g., major cancers, heart attacks, strokes, organ transplants, severe burns).

- Lump-Sum Benefit: You choose a sum insured (e.g., $100,000 – $2 million NZD). Once a covered condition is diagnosed and validated, the insurer pays the amount, usually within 2–4 weeks.

- Waiting & Exclusion Periods: There is often an initial 30-day exclusion period for any new condition; after that, no waiting period applies once you are diagnosed.

- Tax Treatment: Lump-sum payouts are tax-free; premiums are not tax-deductible for individuals.

Why Compare Income Protection vs Trauma Insurance?

- Cash Flow vs Lump Sum: Income protection replaces ongoing income if you can’t work, while trauma insurance provides a lump sum upon diagnosis of a specific condition.

- Complementary Gaps in ACC: ACC only covers accidents, not illnesses. Income protection covers sicknesses and accidents that prevent work; trauma cover fills the gap for critical illness costs.

- Decision Drivers: Your health history, occupation, financial commitments, and tolerance for premium costs will influence whether you need one policy, both, or neither.

Covered Conditions & Eligibility

- Own-Occupation Cover: Pays if you can’t work in your specific job, even if you could do lighter duties (e.g., a carpenter with a back injury).

- Accidents & Sicknesses: Covers work-related and non-work injuries (falls, fractures) and illnesses (arthritis, heart disease, severe depression) that prevent you from performing your occupation.

- Partial Disability: If you return to work part-time, many policies pay up to 50 % of your full benefit.

- Multiple Claims: Once you recover and return to work, you can claim again for a new disabling event (subject to any continuity clause).

- Underwriting:

- Age & Occupation: Typically offered from 18–64 years. High-risk jobs carry premium loadings.

- Health Questionnaire & Medicals: Required for all applicants; paramedical exams or specialist reports may be requested for larger benefit amounts.

- Exclusions: Pre-existing conditions may be excluded or subject to additional charges. Self-inflicted injury, drug/alcohol misuse, war/terror, and high-risk activities are excluded. Mental health claims often have sub-limits.

See How to Claim Income Protection Insurance in New Zealand – 2025 Guide for claim details.

Trauma Insurance Scope

- Specified Critical Illnesses: Typically covers around 40 – 50 conditions, such as major cancers (with partial payments for early-stage), heart attack, stroke, organ transplants, Alzheimer’s, severe burns, and limb loss.

- Partial Payouts: Some insurers pay a reduced amount for procedures such as angioplasty or in situ cancer treatment.

- Age & Child Cover: Standalone adult cover usually for ages 16–64; can attach as an accelerated benefit on a life policy up to age 69. Many policies include free child cover (ages 2–20) at 20 % of the parent’s sum insured.(varies by provider)

- Underwriting:

- Medical Questionnaire: For sums up to a threshold (e.g., $200,000), a health declaration may suffice; larger amounts or older ages trigger paramedical exams or specialist reports.

- 30-Day Exclusion Period: Any condition diagnosed within 30 days of the policy start or reinstatement is excluded. Pre-existing conditions are usually excluded or priced with a loading.

- Exclusions: Self-inflicted injury, substance misuse, war/terror, certain congenital illnesses, and, in some cases, mental health conditions.

Payment Structures, Waiting & Benefit Periods

Income Protection Payment Mechanics

- Benefit Amount: Choose up to 75% of your gross salary, capped by the insurer (e.g., Fidelity Life caps at NZD 30,000/month).

- Payment Frequency: Paid monthly to match your pay cycle.

- Waiting Period: Common options are 4, 8, 13, 26 weeks, or up to 2 years. Longer waits lower premiums but require self-funding until benefits start. (For premium-saving tips, see How to Save on Income Protection Insurance Premiums in 2025

- Benefit Period: Select 2 years, 5 years, to age 65, or to age 70. “To age” options continue until you return to work, retire, or reach the specified age.

- Tax Treatment: Premiums are generally tax-deductible for self-employed individuals or those with company-owned policies; however, employees cannot deduct them. Benefit payments are taxed as income in the year received.

Trauma Insurance Payment Mechanics

- Lump-Sum Benefit: One-off, tax-free payment of your chosen sum insured within 2–4 weeks of claim approval.

- Use of Funds: Flexible—cover medical bills, specialist treatment, rehab equipment, mortgage/rent, carer wages, or home modifications.

- Exclusion Period: Any condition diagnosed within 30 days of policy start or reinstatement is excluded. After 30 days, a confirmed diagnosis of a covered condition qualifies.

- Tax Treatment: Payouts are 100 % tax-free. Premiums are not tax-deductible for individuals (business owners may structure cover under a company).

Comparing “Income Protection vs Trauma Insurance”

| Feature | Income Protection | Trauma Insurance |

| Proof Required | Ongoing proof of incapacity (medical certificates, specialist reports) | Only confirmed diagnosis of a covered condition |

| Payment Structure | Monthly payments (taxed as income) | One-off, lump-sum payment (tax-free) |

| Use of Funds | Funds living costs over time (mortgage, rent, bills, groceries) | Covers large, immediate costs (specialist treatments, medical out-of-pocket expenses, debt clearance) |

| Ideal For | Maintaining household cash flow during extended recovery | Handling upfront expenses after a critical illness diagnosis |

Cost Comparison & Sample Scenarios

Major Premium Drivers

Whether you choose income protection or trauma insurance, the cost depends on:

- Age & Gender: Older applicants pay more; gender loadings vary by insurer (some now offer gender-neutral rates).

- Occupation Loading: High-risk jobs (construction, forestry, mining) carry premium loadings for both IP and TI.

- Benefit Amount: Higher monthly IP benefits or larger TI sums insured increase premiums.

- Waiting and Benefit Periods (IP): Shorter waiting periods and longer benefit periods result in higher IP premiums.

- Add-On Options: Inflation-linked benefits (CPI indexation), partial disability, and guaranteed increase options all add to policy cost.

Sample Cost Table (Illustrative Figures in NZD/month)

| Profile | TI $150k Sum Insured | IP $5k/month Benefit, 8-Week Wait | TI $200k Sum Insured | IP $8k/month Benefit, 4-Week Wait |

| Age 30, Non-Smoker, White-Collar | $22/mo | $50/mo | $28/mo | $165/mo |

| Age 45, Smoker, Manual Occupation | $42/mo | $160/mo | $52/mo | $275/mo |

Note: These figures are illustrative. Premiums vary significantly based on health history, exact occupation, insurer underwriting, and policy features. Always Compare Now for up-to-date quotes.

Long-Term Cost Implications

- Trauma Insurance: Premiums remain level until age 65 or 70. If you add CPI indexation (e.g., 3 % annual increases), your payment rises each year. At age 65, most insurers let you stop CPI increases and keep the same premium, but your sum insured won’t grow further.

- Income Protection: Uses step-rated premiums that increase annually or at age milestones (40, 50, 60). As you get older, rates rise—your IP premium at 60 can be 3–4 times what you paid at 30 for the same benefit and waiting period.

Use of Online Calculators & Adviser Comparisons

Instead of relying on generic calculators that assume “average” health and occupation, use our comparison tool to get tailored premium quotes. At Compare Income Protection, you can enter your exact job, health history, and desired features from multiple insurers. Simply click Compare Now to view personalised quotes and choose the best policy for your needs.

Pros & Cons at a Glance

Income Protection

| Pros | Cons |

| • Ongoing Cash Flow: Replaces up to 75% of gross earnings for months or years, depending on policy. | • Taxable Benefits: Monthly payments are taxed as income, reducing your net benefit. |

| • Broad Cover: Applies to a wide range of injuries and illnesses, from mental health conditions (e.g., severe depression) to chronic diseases (e.g., arthritis). | • Higher Premiums Than TI: Because it covers both injury and sickness over time, premiums are generally higher than trauma. |

| • Multiple Claims: You can claim again after recovery if another disabling event occurs (no limit on the number of claims). | • Ongoing Proof Required: You must regularly provide medical evidence (GP or specialist certificates) to continue payments. |

| • Flexible Options: Choice of waiting periods, benefit periods, partial disability cover, and inflation protection riders. |

Trauma Insurance

| Pros | Cons |

| • Tax-Free Lump Sum: A one-off payment upon diagnosis of a specified condition, without income tax. | • Limited to Listed Conditions: Only pays for specified critical illnesses; no payout for non-covered events (e.g., broken leg, chronic fatigue). |

| • Immediate Access: Funds typically paid within 2–4 weeks of claim approval; ideal for urgent medical or living expenses. | • One-Off Payout: Once you receive the lump sum, you must budget carefully; no further payments if funds deplete during a long recovery. |

| • Lower Premiums Initially: For younger, healthier applicants, TI premiums are often lower than IP for similar ages. | • Non-Deductible Premiums: Premiums are not tax-deductible for individuals (though self-employed may sometimes structure cover under a company). |

| • No Proof of Incapacity: Only a confirmed diagnosis is required; you could still be working part-time or full-time when you get paid. |

How to Choose: Decision Framework

1. Assess Your Financial Situation

- Family & Expenses: If you have a high mortgage, rent, or school fees, prioritise income protection to maintain a steady cash flow.

- Debt & Savings: With limited savings or a large mortgage, trauma insurance’s lump sum can clear debt or cover major treatment costs.

- Health & Family History: A family history of cancer, heart disease, or stroke may make trauma insurance more valuable.

- Occupation Risk: In high-risk trades (e.g., construction, plumbing), income protection covers disabling injuries.

2. Coverage Strategy

- Income Protection Only: Best if you need reliable monthly income replacement (professionals, self-employed).

- Trauma Insurance Only: Suitable if you have emergency savings but need a lump sum for specialist treatments not covered by ACC.

- Combined Income Protection and Trauma Insurance: Trauma insurance provides immediate funds on diagnosis; income protection maintains your lifestyle during recovery.

3. Budget & Premium Choices

- Income Protection Waiting & Benefit Periods: A longer waiting period (e.g., 26 weeks) lowers premiums; ensure savings cover initial months before benefits start.

- Trauma Insurance Sum Insured: Choose a lump sum (e.g., $100,000) that covers treatment and debts without paying for excessive coverage.

- Inflation Riders: CPI indexation preserves benefit value but increases premiums by around 3 – 5 % annually.

For guidance on selecting the right cover amount, see How Much Income Protection Cover in NZ Do You Really Need?.

4. When to Consult a Financial Adviser

- Complex Needs: If you’re self-employed, run a small business, require key-person cover, or have unique health considerations, consult a financial adviser.

- Side-by-Side Comparison: Use our comparison platform—Compare Now—then confirm policy details and exclusions with an adviser.

This framework helps you decide between income protection, trauma insurance, or both, balancing cost and coverage to match your personal circumstances.

Lesser-Discussed but Essential Topics

Tax Implications & Estate Planning

- Income Protection Premiums: Self-employed individuals and company directors can claim income protection premiums as a tax deduction—see detailed IRD guidance on deductible insurance premiums at Inland Revenue (IRD)..

- Trauma Insurance Payouts: Lump sums are 100 % tax-free and don’t affect most government benefits. If you plan to leave the payout to dependents, consider how it fits into your estate plan—consult a solicitor or trustee.

Policy Review & CPI Indexation

- Guaranteed Increase Options: After life events (marriage, new home, new child), most insurers let you boost your sum insured—usually within 60 days—without medical evidence.

- CPI Indexation: Adding inflation protection increases your benefit by a set percentage (typically 3 – 5 %) each year; premiums rise accordingly.

- Regular Review: Life changes (new job, pay rise, growing family) can leave your cover inadequate. Revisit your policy every 2 – 3 years or after any significant event.

Mental Health & Partial Disability Considerations

- Mental Health Claims (Income Protection): Insurers often cap mental health payouts (e.g., 12 months for anxiety/depression). Review each policy’s definitions and sub-limits before signing.

- Partial Disability Payments: If you return to work part-time, many policies pay a pro-rata benefit (e.g., 50 % of your full IP benefit for half-time work).

- Continuity Clauses: If you relapse within a defined period (often 3 months), some insurers waive a new waiting period and resume benefits immediately.

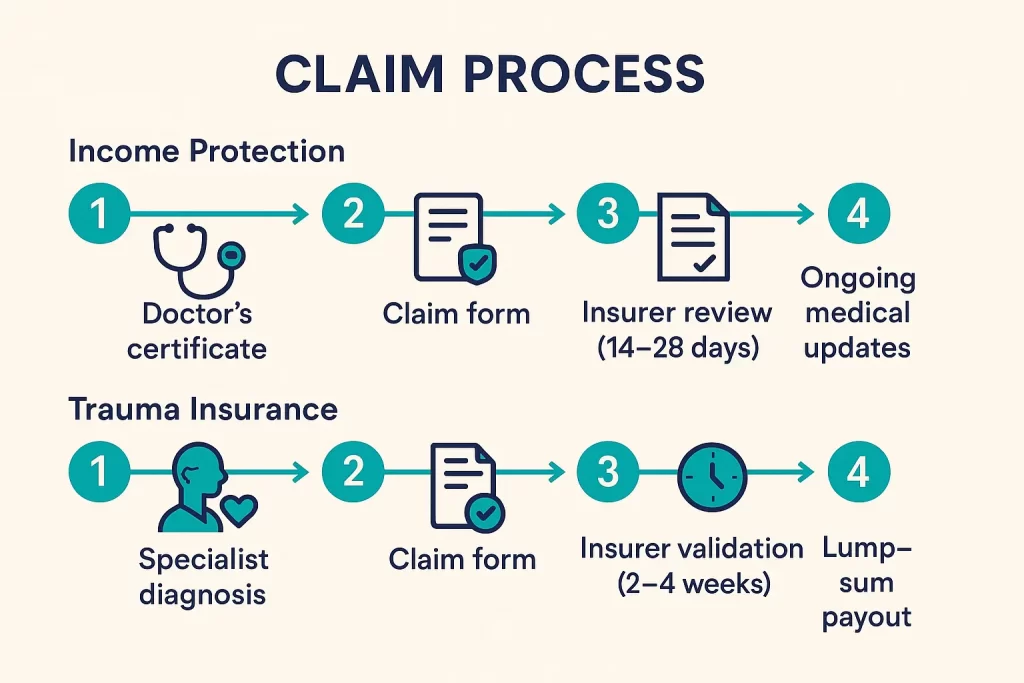

Claim Process & Real-Life Examples

Claiming Income Protection

- Obtain a Medical Certificate: Your treating GP or specialist certifies that you’re unable to work in your own occupation due to illness or injury.

- Submit a Claim Form: Complete the insurer’s IP claim form, attach the medical certificate, proof of earnings, and your employment details.

- Insurer Assessment: The insurer reviews your documentation—this may include a Paramedical Exam (PME) or additional specialist reports. Processing typically takes 14 – 28 days if the paperwork is complete.

- Ongoing Reviews: To continue receiving payments, you must provide periodic medical updates (typically every 3–6 months) until you have fully returned to work.

For a detailed walkthrough, see How to Claim Income Protection Insurance in New Zealand – 2025 Guide.

Claiming Trauma Insurance

- Confirm Diagnosis: Obtain a formal diagnosis report from a registered specialist (e.g., oncologist, cardiologist, neurologist) with test results or pathology confirmation.

- Submit a Claim Form: Complete the insurer’s trauma claim form and attach all medical evidence—this may include imaging scans, pathology reports, hospital discharge summaries, and specialist notes.

- Insurer Review & Payout: Once the insurer validates the diagnosis against policy definitions, they generally approve and pay the lump sum within 2 – 4 weeks. Some insurers may request additional reports if the diagnosis is borderline or involves partial benefit triggers (e.g., in situ cancer).

Case Study A: Anna, 35, Teacher

Anna, a primary school teacher from Wellington, noticed persistent fatigue and diagnosed herself with early-stage breast cancer after a routine mammogram. She held trauma insurance with a $150,000 sum insured. After submitting her claim with pathology and specialist letters, she received her lump sum in 3 weeks. She used $40,000 for private oncology treatments not covered by ACC, $60,000 to pay down her mortgage, and $20,000 as living expenses while she took six months of medical leave. Anna continued working part-time throughout treatment, so she did not claim income protection.

Case Study B: Brad, 48, Builder

Brad, a Hamilton-based builder, slipped off a scaffold and suffered a severe ankle fracture. ACC covered his initial rehabilitation, but his weekly ACC payment capped at $1,000 NZD was insufficient to cover his $5,500 monthly mortgage and family expenses. He had income protection with an 8-week waiting period and $8,000 monthly benefit. After waiting 8 weeks post-surgery, his IP policy paid $8,000 per month for 9 months until he returned to full duties. He did not qualify for trauma insurance because a broken ankle is not a covered critical illness.

Conclusion & Call to Action

Navigating income protection vs trauma insurance can feel daunting, but understanding the core differences—ongoing cash-flow replacement versus immediate lump-sum payouts—will help you choose the right cover for your situation. If you have significant ongoing living costs, prioritising income protection may be wise. If you or your family has a history of critical illness, trauma insurance could provide crucial medical funds. Many Kiwis find that a layered approach—owning both policies—offers the most comprehensive protection.

Ready to compare policies and find the best fit? For instance, no-obligation quotes from leading New Zealand insurers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}