Key Person Insurance in New Zealand: Essential 2025 Guide

Imagine you run a small business here in New Zealand — perhaps you’re a sole trader, or you have a handful of employees. Your business success depends heavily on you and maybe a few key people who bring skills, clients, or leadership to the table. That’s why key person insurance in New Zealand is essential: what happens if one of those key people suddenly can’t work due to illness, injury, or worse?

This type of business insurance provides financial protection if a critical person in your company is unable to work, helping your business stay afloat when you need it most.

At Compare Income Protection, we understand the importance of protecting not only your income but also the financial stability of your business. This guide will walk you through what key person insurance is, why it’s crucial for Kiwi businesses, how it works, and how you can compare and find the best policy for your needs, all with a focus on helping you use our free comparison tools to make an informed decision quickly and confidently.

Why is this important? Because in New Zealand, most businesses are small or micro-sized, meaning they rely heavily on a few people, often just one or two. Losing a key person unexpectedly can disrupt operations, result in lost revenue, or even threaten the business’s survival. Key person insurance serves as a financial safety net, providing your business with the breathing room it needs to recover or adapt.

Throughout this article, you’ll see practical examples tailored to New Zealand’s business landscape, clear explanations of insurance concepts, and helpful tips on getting started with protecting your business.

Ready to take the next step? You can start by checking out key person insurance quotes on Compare Income Protection — click Compare Now to see what’s available.

What is key person insurance in New Zealand?

Key person insurance is a special type of business insurance designed to protect your company if a crucial individual is suddenly unable to work due to illness, injury, or death. Unlike personal income protection, which pays out to an individual, key person insurance pays a benefit directly to your business. This money can help cover lost income, recruit replacements, pay bills, or settle debts, keeping your business running smoothly during a tough time.

Key person insurance typically covers:

- Death or terminal illness: Provides a lump sum to the business if the key person passes away or is diagnosed with a terminal condition.

- Critical illness (trauma cover): Pays out if the key person suffers a serious illness, such as cancer, a heart attack, or a stroke, helping to cover costs while they recover.

- Total and permanent disability: Offers a lump sum if the key person is permanently unable to work.

- Temporary disability or income protection: Some policies provide monthly payments to the business to cover income loss if the key person is temporarily unable to work.

You can choose to cover one or several of these risks depending on your business needs and budget.

By using Compare Income Protection, you can easily compare the best policies from leading insurers tailored to New Zealand’s market. You can view coverage options, prices, and features all in one place, helping you make the best decision for your business.

Want to explore your options?

Who Needs Key Person Insurance in New Zealand?

If your business relies heavily on one or more individuals whose absence would cause significant disruption, you should seriously consider key person insurance. This is especially true for:

- Sole Traders and Self-Employed Professionals: When you’re the main (or only) driver of your business, your ability to work directly impacts the company’s income. Losing your capacity to work means your business income stops, and key person insurance can provide a crucial safety net.

- Small Business Owners: If your business depends on you and a few key employees — maybe your lead salesperson, a technical expert, or your operations manager — losing any of these people can put your business at risk.

- Partnerships: If you have business partners, especially if each partner plays a unique, essential role, key person insurance can protect the company’s future by providing funds if one partner is unable to contribute.

- Businesses with Key Employees: Even if you have a larger team, you might have individuals whose skills, knowledge, or client relationships are vital. Key person insurance can help cover the financial consequences of losing a key person temporarily or permanently.

Assessing Your Business Risks

Ask yourself:

- If you (or a particular team member) were suddenly unable to work for six months or more, how would that affect your revenue and operations?

- Could you afford to hire temporary help or a replacement?

- Would your clients stay loyal, or would they look elsewhere?

- Do you have outstanding business loans or investor commitments that depend on your continued involvement?

If any of these questions raise concerns, key person insurance is a worthwhile consideration.

Statistics to Consider

- In New Zealand, over 90% of businesses have fewer than 5 employees, meaning most companies rely on just a few key people to keep things running. According to Stats NZ

- Research shows that only about 8% of SMEs offer any form of life or income insurance for their employees, leaving many vulnerable to financial shocks.

- ACC covers injuries but doesn’t protect businesses from income loss due to illness, nor does it provide funds to cover lost profits or the cost of hiring replacements.

How Compare Income Protection Helps You

Our comparison tool is designed with Kiwi business owners in mind, helping you quickly identify coverage options tailored to your specific business structure and key people. You can compare multiple providers side by side to find the right balance of cost and protection.

Ready to protect your business key people?

Start comparing policies now — click and get your personalised quotes.

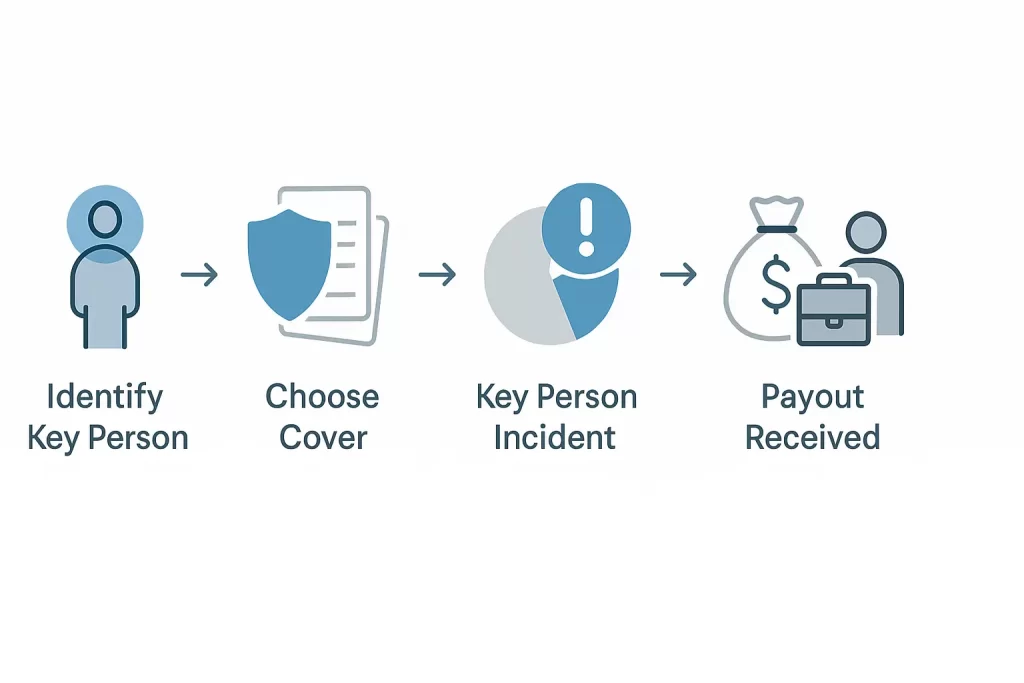

How Key Person Insurance Works

Understanding how key person insurance works can help you appreciate its vital role as a key tool for small businesses. Here’s the straightforward breakdown:

- The Business Owns the Policy

Unlike personal insurance, key person insurance is owned by the business, not the individual. Your company pays the premiums, and in the event of a claim, the payout goes directly to the industry. This setup ensures that the funds can be used to keep the business running smoothly.

- Choosing the Key Person(s) and Coverage

When you apply for key person insurance, you nominate the individuals you want to cover—this could be yourself, a partner, or any employee whose loss would impact the company. You’ll also decide on the amount of cover, which typically reflects the financial loss the business would experience if that person were unable to work.

The type of cover you choose depends on your needs and budget:

- Lump Sum Cover: Pays out a single sum if the key person dies or is diagnosed with a terminal illness.

- Critical Illness Cover: Pays a lump sum if the key person is diagnosed with a serious illness.

- Total and Permanent Disability (TPD): Provides a lump sum if the key person is permanently disabled.

- Income Protection: Pays monthly benefits to the business if the key person is temporarily unable to work due to illness or injury.

Many businesses opt for a combination of these to cover different scenarios.

- Medical and Financial Underwriting

The key person will need to provide health information, which may include a medical examination. For larger cover amounts, financial underwriting may also be required to ensure the coverage amount is appropriate, based on the business size and the individual’s role.

- Claiming and Using the Payout

If the insured key person dies, becomes critically ill, or is unable to work, the business can file a claim. After approval, the insurer pays the benefit directly to the business. Unlike ACC or personal insurance payouts, there’s no restriction on how the business can use the funds — they can cover lost revenue, pay employees, recruit replacements, or reduce debt.

How does this benefit your business?

Key person insurance provides your company with a financial buffer during the worst possible time. Instead of scrambling for cash or taking on debt, you have funds to manage operations, cover costs, and plan your next steps without panic.

Use our tool to see how key person insurance could work for your business.

Get started by clicking Compare Now to view tailored quotes instantly.

Key Benefits for Your Business

Key person insurance in New Zealand provides a range of vital benefits that can help keep your business resilient in the event of the unexpected. Here’s how it supports your company:

- Maintaining Cash Flow and Operations

When a key person is unable to work, your revenue might take a hit. Insurance payouts can cover day-to-day expenses like rent, utilities, and staff wages, ensuring your business continues to operate smoothly without financial stress.

- Funding Replacement Staff or Contractors

Hiring and training new staff takes time and money. Key person insurance can provide the funds needed to bring in temporary or permanent replacements without straining your cash reserves.

- Protecting Client Relationships

Clients value consistency. If your business can maintain service levels even when a key person is absent, it helps retain customer confidence and loyalty — a crucial factor in business survival.

- Meeting Loan Obligations and Creditor Confidence

If you have business loans or creditors, a key person insurance payout reassures them you can meet your obligations, reducing the risk of defaults or penalties.

- Buying Time to Strategise

Having financial support allows you to pause and make informed decisions about the future of your business, whether that means hiring new talent, restructuring, or gradually returning to full capacity.

Real-World Example:

Consider a small IT firm in Wellington where the lead developer falls ill unexpectedly. The insurance payout helps cover lost income and pays for a contractor to maintain ongoing projects, keeping clients happy and the business afloat until the developer returns.

Ready to protect your business with these benefits?

Take action now by clicking to explore your options.

Cost Factors of Key Person Insurance

Understanding what influences the cost of key person insurance helps you make an informed choice that fits your budget and business needs. Here are the main factors that affect premiums:

- Coverage Amount

The higher the sum insured, the higher the premium. You should select an amount that reflects the potential financial impact of losing the key person, often calculated as one or two years’ worth of their contribution to business profits or the costs involved in hiring a replacement.

- Policy Duration

Policies can be short-term (e.g., 5 years) or long-term (10, 20 years, or until a certain age is reached). More extended coverage generally costs more but provides peace of mind for a greater period.

- Type of Cover

Including critical illness and total permanent disability cover increases premiums compared to life-only policies because these conditions are more common and can result in payouts without death occurring.

- Age and Health of the Key Person

Younger, healthier individuals cost less to insure. Smoking, pre-existing conditions, and risky hobbies or occupations can increase premiums or result in exclusions.

- Occupation and Lifestyle

High-risk occupations (like construction or manual labour) may attract higher premiums than office-based roles. Similarly, hobbies like skydiving or motorsports may affect the cost.

How to Manage Costs

- Choose appropriate cover levels rather than over-insuring.

- Opt for more extended waiting periods before income protection benefits kick in (e.g., 8 weeks instead of 4).

- Select a benefit period that aligns with your business needs — sometimes shorter terms reduce premiums substantially.

Use our tool to get personalised quotes and compare costs from multiple insurers: Compare Now.

Key Person Insurance vs Shareholder Protection

While key person insurance and shareholder protection seem similar, they serve different but complementary purposes in safeguarding your business.

Key Person Insurance:

- Protects the business from financial loss when a vital individual (often a key employee or owner) cannot work due to illness, injury, or death.

- The business is the beneficiary, and the payout is used to cover lost income, hire replacements, or manage operational costs.

Shareholder Protection:

- Ensures smooth ownership transition if a shareholder dies or becomes disabled.

- Often linked to buy-sell agreements, where surviving shareholders buy out the deceased’s shares using insurance proceeds.

- Typically owned by shareholders individually, not the business.

Why both matter:

If your business has multiple owners or investors, combining key person insurance with shareholder protection creates a full safety net, covering operational risks and ownership continuity.

Not sure which you need?

Our comparison tool focuses on key person and income protection insurance, but can also serve as a good starting point for discussing your broader protection needs with an adviser. You can always start here:

Common Mistakes to Avoid

Protecting your business with key person insurance is smart, but there are some common pitfalls that Kiwi business owners should watch out for:

- Underestimating the Financial Impact

Many underestimate the cost to their business of losing a key person. It’s not just about salary — consider lost profits, recruitment costs, training, and operational disruption. - Relying Solely on ACC or Personal Insurance

ACC covers accidents but won’t pay out for illnesses or cover your business’s lost revenue. Personal income protection helps individuals but doesn’t directly support the business financially. - Incorrect Policy Ownership

Ensure the business owns the policy, not the individual. Otherwise, payouts may not go to the company when you need them most. - Not Reviewing Coverage Regularly

As your business grows, the importance and impact of key individuals may change. Review your policies at least annually to ensure coverage remains appropriate. - Not Considering Multiple Key People

Don’t just insure the business owner. If other employees or partners are critical, consider insuring them too.

Avoid these mistakes by using trusted advice and comparing options through Compare Income Protection. Our platform makes it easy to identify the policies that are right for your business. Don’t leave your business exposed — start protecting it today:

How to Choose and Apply for a Policy

Choosing and applying for key person insurance might seem complex, but it’s easier than you think, especially with the right guidance and tools. Here’s a step-by-step approach tailored for Kiwi business owners:

- Identify Your Key Person(s)

List the individuals whose absence would have the most significant financial impact on your business. This often includes owners, partners, and employees with unique skills or client relationships. - Calculate the Cover Amount

Estimate the financial loss if the key person couldn’t work. This can include lost revenue, replacement costs, training expenses, and debt obligations. Many businesses insure for one to two years’ worth of the key person’s contribution. - Decide on Coverage Type

Choose between lump sum cover, income protection-style monthly payments, or a combination. Consider what risks your business faces and what would help most during a loss. - Compare Quotes

Use the Compare Income Protection tool to get tailored quotes from multiple insurers quickly. This saves time and ensures you find the best balance of price and cover. - Complete the Application

The key person will likely need to answer health questions and undergo a medical exam. You may also need to provide financial details about your business, especially for larger cover amounts. - Review and Finalise

Before signing, check all policy terms, including waiting periods, benefit duration, and exclusions. Keep your accountant or insurance adviser involved to ensure the policy fits your tax and business needs.

Why use Compare Income Protection?

Our free, no-obligation comparison tool helps you make confident decisions by showing options side-by-side — no more guesswork, just clear choices.

Ready to find the right policy?

Conclusion

Protecting your business from the unexpected is one of the smartest decisions you can make as a Kiwi business owner. Key person insurance in New Zealand provides a vital safety net that helps your company survive and thrive even when a crucial individual is no longer able to work.

From maintaining cash flow and covering replacement costs to protecting client relationships and meeting loan obligations, key person insurance is about giving your business the financial strength to weather any storm.

At Compare Income Protection, we make it easy for you to explore your options and find the best key person insurance policy tailored to your unique business needs. With our free comparison tool, you can view quotes from multiple trusted insurers side by side, saving time and giving you confidence in your choice.

Don’t leave your business vulnerable. Take control today:

Frequently Asked Questions (FAQs) About Key Person Insurance in New Zealand

Q1: Who qualifies as a key person in my business?

A key person is anyone whose absence would significantly impact your business operations or revenue. This could be you as the owner, a co-founder, a top salesperson, or a specialist with unique skills or client relationships.

Q2: Can I insure more than one key person?

Yes! Many businesses insure multiple key people to protect against the loss of several critical contributors.

Q3: How much key person insurance coverage do I need?

Coverage should reflect the financial loss your business would face if the key person couldn’t work. A common approach is to insure for one to two years of the person’s contribution to profit or revenue, plus recruitment and training costs.

Q4: Is key person insurance expensive?

Premiums vary based on factors like coverage amount, the key person’s age and health, and the type of cover chosen. Using a comparison tool like ours can help you find affordable options that fit your budget.

Q5: Are premiums for key person insurance tax-deductible?

Generally, if the policy protects business revenue or profits, premiums are tax-deductible as a business expense in New Zealand. However, tax treatment can vary, so it’s best to consult your accountant.

Q6: What happens if the key person leaves the business?

If the insured person leaves or retires, you should update or cancel the policy accordingly. Keeping coverage aligned with your current business structure is important.

Q7: How quickly can a claim be paid?

Claims processing times vary by insurer but most strive to handle claims promptly, especially for critical illnesses or death. Having all the required documentation ready can help speed things up.

Q8: Can I apply for key person insurance without medical underwriting?

Most insurers require health information or medical checks, especially for higher coverage amounts. Some may offer simplified underwriting for lower amounts or younger individuals, but medical checks are common.

Q9: What’s the difference between key person insurance and income protection insurance?

Key person insurance in New Zealand is owned by the business and pays out to the business if a key individual is unable to work. Income protection insurance is owned personally and pays out to an individual to replace their income.

{kind=link}

{kind=link}

{kind=link}

{kind=link}