ACC vs Income Protection Insurance in New Zealand

ACC vs Income Protection Insurance: Why It Matters for Every Kiwi

ACC vs Income Protection Insurance is a topic every New Zealander should understand, because the difference can mean everything for your financial security. Picture this: Jess, a freelance designer from Christchurch, spends her days helping local businesses and her evenings running after two young kids. One Monday, she wakes up with sharp pains, and after tests, she’s diagnosed with a rare illness that puts her out of work for months. Jess is relieved, thinking, “I pay ACC every year—they’ll help.” But a week later, she learns a hard truth: ACC is only for accidents, not illnesses. Suddenly, there’s no money coming in, and the mortgage won’t wait.

Jess’s story is surprisingly common and highlights a crucial gap in how many New Zealanders understand their financial safety net.

Why Does This Matter?

Whether self-employed, a contractor, or a salaried worker, knowing the difference between ACC and income protection insurance isn’t just about ticking a box. It could be the difference between staying afloat and struggling if illness or injury keeps you from earning.

This article explores ACC vs Income Protection Insurance in New Zealand, helping you understand how both work and which is right for you.

Want to see how income protection stacks up for your situation? Check out our Income Protection Insurance Comparison to explore your options.

Understanding ACC (Accident Compensation Corporation)

What Is ACC?

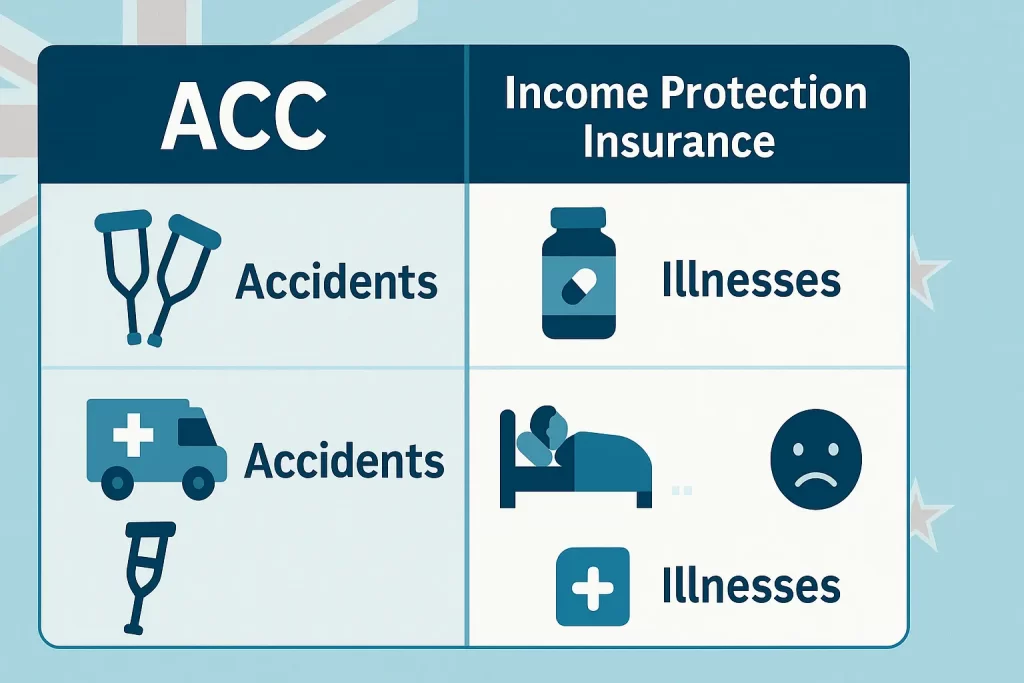

To truly compare ACC vs Income Protection Insurance. It’s important to understand exactly what ACC covers and where its limits lie. The Accident Compensation Corporation—better known as ACC—is New Zealand’s unique, government-run scheme designed to support anyone in Aotearoa who suffers an accidental injury. You’re automatically covered whether you’re a resident, a new arrival, or even a tourist. ACC operates on a no-fault basis, meaning you’re eligible for help regardless of how the accident happened (with a few exceptions).

What Does ACC Cover?

- Medical Treatment & Rehabilitation:

ACC will pay for necessary medical treatment after an accident, which might include GP visits, surgery, physio, and rehab costs.

- Compensation for Lost Earnings:

If your injury prevents you from working, ACC can pay up to 80% of your pre-injury income, though there is a cap (as of 2024, this is $2,355 per week before tax). This can be a lifesaver for families suddenly missing a regular paycheque, especially when other support options are limited.

- Support for Long-Term Recovery:

ACC can help with home modifications, support workers, or retraining if your injury leads to long-term disability.

Key Limitations

- ACC is for Accidents Only:

Illnesses, mental health conditions (unless triggered by a physical accident), or chronic diseases aren’t covered. If you’re unable to work due to cancer, heart disease, or any other non-accidental health issue, ACC can’t help. - Strict Acceptance Criteria:

Your claim must clearly relate to a physical accident. The process includes paperwork, medical reports, and sometimes a waiting period.

- You Might Have to Take a Different Job:

ACC can encourage you to return to any work you’re capable of doing, not just your previous job, even if it means a pay cut.

Pro Tip:

ACC is a great foundation, but it isn’t a catch-all. If your risk of illness is higher than your risk of injury (which is true for most Kiwis), ACC alone won’t protect your income.

Learn more straight from the source at the ACC Official Website.

What Is Income Protection Insurance?

Income protection insurance is your financial safety net. It pays you a regular income if you’re unable to work due to either illness or injury, not just accidents. Unlike ACC, which only kicks in after an accident, income protection steps up for a whole range of health setbacks, including serious illnesses or mental health issues.

What Does It Cover?

- Accidents and Illnesses:

Whether you’re injured mountain biking or sidelined by a long-term illness like cancer or depression, income protection can help keep your household running. - Mental Health Conditions:

Many policies now recognise that mental health is as important as physical health. If you’re signed off work due to stress, anxiety, or burnout, you may still be eligible for payments.

- Customisable Benefit & Waiting Periods:

You can choose how long you want payments to last (e.g., 2 years, 5 years, or until you reach age 65/70) and set a waiting period (the time you’ll wait before payments start, like 4, 8, or 13 weeks). A longer waiting period often means lower premiums.

Types of Policies

- Agreed Value:

The payout is based on your income when you took out the policy, regardless of any changes since then. This offers certainty, especially for self-employed or variable earners.

- Indemnity Value:

The payout is based on your income at claim time. This is usually cheaper, but if your income drops before a claim, so does your benefit. - Add-ons and Riders:

You can enhance your policy with extras, such as redundancy cover, premium waivers during claims, or additional cover for specific medical conditions.

What Does It Cost?

Premiums vary for everyone, depending on:

- Your age, health, and occupation

- How much coverage do you want and for how long

- Your chosen waiting and benefit periods

- The type of policy (agreed vs. indemnity value)

Pro Tip:

Consider what you’d realistically need to pay the bills, cover your mortgage, and keep the kids in school if you couldn’t work for six months or longer. Start by comparing options and getting quotes—prices and features can vary greatly.

Want to see what’s available and compare providers? Head to our Income Protection Insurance Comparison page to get started.

Comparative Analysis: ACC vs Income Protection Insurance

When protecting your income in New Zealand, it’s easy to think, “ACC has me sorted.” But that’s only half the story. Here’s how ACC and income protection insurance compare, side by side.

Coverage Comparison

- ACC:

Covers only accidents and injury-related events. Funded by levies from employees, employers, and the self-employed—so everyone’s in, but only for physical mishaps.

- Income Protection Insurance:

It covers accidents and illnesses, as well as many mental health conditions. It is privately purchased, so you choose the provider and the features that matter to you.

Benefit Limits

- ACC:

Pays up to 80% of your regular income before your injury, but it’s capped (currently up to $2,355 per week before tax as of 2024). If you earn above the cap, you could face a shortfall.

- Income Protection:

Usually pays up to 75% of your income. The amount is flexible—tailor it to your needs, within policy limits. The benefit period can be short-term or until retirement, depending on your policy.

Tax Implications

- ACC:

Any payments you receive from ACC are considered taxable income. The amount you receive may be less than you expect.

- Income Protection Insurance:

Tax can get complicated. Generally, your benefit payments are taxable if you claim your premiums as a tax deduction (possible with indemnity-style policies). Your benefits are tax-free if you don’t claim the deduction (usually with an agreed value). It pays to check with an accountant or adviser.

Claim Process

- ACC:

Only covers claims that are directly linked to an accident. The process is strict: you’ll need medical evidence that your injury is due to an accident, and claims for illness will be declined.

- Income Protection Insurance:

Broader criteria—covering most health conditions that prevent you from working. You’ll need medical evidence and sometimes additional forms, but the range of what’s covered is much wider than ACC.

Pro Tip:

Don’t wait to figure out these differences until you’re in a crisis. For most Kiwis, illness is far more likely to keep you off work than a serious accident. That’s where income protection insurance is an absolute game-changer.

How Do ACC and Income Protection Insurance Work Together?

The most innovative approach isn’t choosing one or the other—it’s understanding how they combine to create a stronger safety net. Here’s how it works for Kiwis:

Integration Strategy:

Consider ACC your built-in accident safety net, while income protection insurance covers the much broader risks, like illnesses, mental health setbacks, and longer-term inability to work. If you’re injured in an accident, ACC kicks in first; income protection picks up the slack if an illness strikes you down.

- For Accidents:

ACC pays first, covering your medical care and up to 80% of your usual income (to the cap). If you have income protection insurance, it may “top up” the shortfall, depending on your policy settings.

- For Illness:

ACC won’t help, but your income protection policy can step in and keep your income flowing.

Offset Considerations:

Income protection insurers in NZ usually take ACC payments into account to avoid overcompensation. So, if you’re already getting 80% of your income from ACC, your insurer may only pay the difference between that and your insured benefit amount. The details depend on your policy, so it pays to check the fine print or ask your adviser.

Pro Tip:

When setting up income protection, ensure your adviser knows about your ACC status. Some policies are structured so you pay a lower premium because ACC will cover accidents, while the insurance focuses on illnesses and any shortfall.

Example:

Sarah, a self-employed photographer in Wellington, has both ACC CoverPlus Extra and income protection insurance. She broke her leg in a mountain biking accident. ACC pays 80% of her usual income. Since her income protection policy is set up to only “top up” accident-related claims, her insurance only pays out if ACC’s payment is less than her insured benefit. However, if Sarah were off work for a serious illness instead, her income protection policy would pay her full agreed benefit (up to her policy limits) because ACC wouldn’t apply.

Pro Tip:

Ask your insurer or adviser about “ACC offsets” and “ACC reduction options” to ensure your policy is optimised for your needs and your premiums aren’t higher than they need to be.

Check out our article about how much income protection you need.

Tax Considerations

Understanding the tax treatment of income protection insurance is crucial—it can affect both your take-home benefit and the affordability of your cover.

Premium Deductibility

- Indemnity Policies:

If you choose an indemnity policy (where your payout is based on your actual income at claim time), your premiums are generally tax-deductible in New Zealand. This can make the cover more affordable, especially for self-employed or contract workers.

- Agreed Value Policies:

For agreed value policies (where your payout is fixed based on your income when you took out the policy), premiums are not usually tax-deductible. The exception is that deducting the premiums will make your benefit taxable.

Benefit Taxation

- Indemnity Policies:

Since premiums are typically claimed as a tax deduction, any benefits paid out are treated as taxable income. That means you’ll need to budget for tax on your payout, just like normal salary or wages.

- Agreed Value Policies:

If you haven’t claimed a tax deduction for your premiums, the benefit is generally paid out tax-free. This can mean more certainty about what you’ll actually receive if you need to claim.

Pro Tip:

Always check with your accountant or a specialist adviser before claiming premium deductions or setting up your policy. The right tax structure could make a real difference to your cash flow if you ever need to claim.

Example:

Lisa, an Auckland IT contractor, takes out an indemnity policy and claims her premiums as a tax deduction. When she makes a claim, her monthly benefit is taxed as income. Her friend Sam chooses an agreed-value policy and pays a slightly higher premium, but his benefit is tax-free if needed.

Special Considerations for Self-Employed Individuals

Running your own business or freelancing in New Zealand has plenty of perks, but it also means your income protection needs are unique, especially since there’s no sick leave safety net if you’re out of action. Check out our income protection for self-employed Kiwis guide for a deep dive into tailored cover and policy options.

ACC CoverPlus Extra (CPX)

- Customisable ACC Protection:

CPX lets self-employed people and contractors agree on a set weekly compensation level in advance, regardless of fluctuating earnings. This provides certainty and can help speed up the claims process.

- Combining with Income Protection:

Many self-employed Kiwis pair CPX with private income protection insurance for truly comprehensive protection. CPX covers you for accidents, while income protection insurance picks up the slack for illnesses or extends the payout period.

Pro Tip:

If your income varies yearly (as it often does for the self-employed), review your CPX cover annually to ensure it reflects your actual earning needs.

Why Income Protection Insurance Matters for the Self-Employed

- Covers Both Illness and Injury:

Unlike ACC (which is only for accidents), income protection insurance pays out for any medical reason that stops you working, including illnesses or mental health issues.

- Vital for Solo Operators:

With no employer-funded sick leave or long-term disability benefits, a bout of illness could mean zero income—unless you’re covered.

Example:

A Wellington tradie breaks his arm on-site. ACC CPX pays his pre-agreed weekly income until he’s back on the tools. A few years later, he’s diagnosed with a heart condition—ACC can’t help, but his income protection insurance covers the bills while he recovers.

Pro Tip:

For many self-employed Kiwis, the smartest move is to structure CPX for accidents and lean on income protection insurance for everything else. This combo gives peace of mind—and a real financial safety net.

Ready to compare your options? Visit our Income Protection Insurance Comparison page to get started.

Case Studies and Real-Life Scenarios

Sometimes the best way to understand the importance of income protection is through real-world examples. Here’s how these choices can play out in everyday Kiwi life: These real-life stories show how ACC vs Income Protection Insurance decisions play out when Kiwis face illness or injury.

Scenario 1: Self-Employed Success – Covering All the Angles

Sophie runs her own catering business in Hamilton. She’s set up ACC CoverPlus Extra (CPX), so if she’s injured in an accident, she knows exactly how much she’ll get each week. But Sophie goes a step further—she also has income protection insurance. One winter, she’s hospitalised with pneumonia. ACC can’t help because it’s not an accident. Luckily, her income protection policy pays out, covering her mortgage and business costs until she’s back on her feet.

Insight:

Having both CPX and income protection gave Sophie true peace of mind—she was protected no matter what stopped her working.

Scenario 2: The Employee Who Relied on ACC Alone

Mark is a full-time warehouse worker in Auckland. He’s never really considered income protection, assuming ACC has him covered. But when Mark is diagnosed with a heart condition, ACC declines his claim—no accident, no payout. Mark uses all his sick leave, and his savings quickly run out, forcing him to cut back on essentials until he can return to work.

Insight:

ACC only helps after accidents. Illnesses (which are much more common) can expose even hard-working Kiwis.

Scenario 3: The Difference Income Protection Makes

Emma and James both work in Wellington, earn similar salaries, and are both diagnosed with cancer within months of each other. Emma has income protection insurance; James does not.

- Emma’s Experience: She receives 75% of her monthly income, covers her rent, and focuses on recovery.

- James’ Experience: He burns through his savings, relies on family, and faces stress about bills on top of his health battle.

Insight:

Income protection insurance’s presence (or absence) can be the difference between financial resilience and real hardship.

Pro Tip:

Most Kiwi households are just a few missed paydays from real financial pressure. Don’t wait until you’re in one of these stories—review your cover today.

Want more comparisons? See Income protection compare for a breakdown of different approaches.

Frequently Asked Questions About ACC vs Income Protection Insurance (FAQs)

1. Do I still need income protection insurance if I have ACC?

Yes. ACC covers injuries from accidents but doesn’t cover illnesses. Income protection insurance complements ACC by covering situations where you’re unable to work due to illness, ensuring a more comprehensive safety net.

2. What types of situations does income protection insurance cover?

Income protection insurance covers you if you’re unable to work due to illness or injury. This includes conditions like cancer, heart disease, or mental health issues that ACC doesn’t cover.

3. How much of my income can income protection insurance replace?

Income protection insurance can typically replace up to 75% of your pre-disability income. The exact amount depends on your policy and provider.

4. How do ACC payments affect my income protection insurance benefits?

Suppose you’re receiving ACC payments due to an accident. In that case, your income protection insurance may adjust its payments to ensure you don’t receive more than the agreed-upon percentage of your income. This coordination ensures you receive adequate support without overcompensation.

5. Is income protection insurance tax-deductible in New Zealand?

Yes, premiums for income protection insurance are generally tax-deductible in New Zealand. However, any benefits you receive from the policy are typically considered taxable income. It’s advisable to consult with a tax professional for specifics related to your situation.

6. Does income protection insurance cover mental health conditions?

Many, but not all, income protection policies in New Zealand cover mental health conditions. There may be extra limits, waiting periods, or exclusions. Always check your policy details.

7. Can self-employed individuals get income protection insurance?

Absolutely. Income protection insurance is especially beneficial for self-employed individuals who don’t have access to employer-provided sick leave or benefits. It ensures a steady income stream if you’re unable to work due to illness or injury.

Conclusion

ACC is essential to every Kiwi’s safety net, providing valuable help after accidents. But the reality is, most long-term work absences in New Zealand are caused by illness, not injury. This is where income protection insurance steps in, offering a crucial layer of security for you and your family.

Choosing between ACC vs Income Protection Insurance —or combining both—can significantly impact your financial security.”

Our recommendation:

Take a good look at your situation—your job, family, finances—and consider what would happen if you couldn’t work for several months. The right protection isn’t one-size-fits-all.

Ready to compare your options and find the cover that fits your life?

Visit our Income Protection Insurance Comparison to get started today.

Additional Resources

Tools and Calculators

Take the guesswork out of choosing your cover. Some online tools and calculators can help you determine how much income protection you might need, what your premiums could look like, and how long your finances might last if you couldn’t work.

Tip: When reviewing options, always use up-to-date New Zealand figures for income, ACC limits, and living expenses.

Ready to start comparing? Visit our Income Protection Insurance Comparison to get real quotes and see what’s available for your situation.

Personalised Advice

Income protection isn’t a one-size-fits-all product. For advice tailored to your unique circumstances—whether you’re self-employed, a contractor, or have a family depending on your income—consider speaking to a financial adviser or insurance specialist. They can help you:

- Understand the fine print (including offsets and waiting periods)

- Structure your policy for maximum tax efficiency

- Review your cover as your life changes.

You can reach out to our team or connect with a trusted local adviser through our Contact page.

For more guides, tips, and the latest updates, keep exploring Compare Income Protection—your New Zealand income protection experts.

Disclaimer

The information provided in this article is for general guidance and informational purposes only. It does not constitute personalised financial, insurance, or tax advice. While every effort has been made to ensure accuracy, income protection insurance products, tax rules, and ACC entitlements can change, and individual circumstances will vary. Before making any decisions about your insurance or financial needs, we strongly recommend you consult a qualified financial adviser or insurance specialist familiar with New Zealand law and your personal situation.

{kind=link}

{kind=link}

{kind=link}