Income Protection vs Critical Illness Cover: Best Choice for Kiwis

TL;DR Summary

- Income Protection vs Critical Illness Cover meet different needs: Income Protection replaces income if you can’t work, while Critical Illness provides a tax-free lump sum on diagnosis.

- Inland Revenue confirms Income Protection premiums can be claimed as a non-business expense if payouts are taxable (IRD – Non-business expenses).

- Critical Illness payouts are capital benefits, meaning lump sums are usually tax-free, though premiums are not deductible.

- Oversight from the Financial Markets Authority ensures insurers meet disclosure and fairness standards.

- Compare policies side-by-side today at CompareIncomeProtection.co.nz.

Have you ever wondered whether Income Protection vs Critical Illness Cover is the smarter choice for protecting your family’s financial security? In New Zealand, where many households rely on two incomes to cover mortgages, childcare, and rising living costs, choosing the right insurance type can make all the difference.

The key difference between Income Protection vs Critical Illness Cover lies in how and when the benefit is paid. Income Protection provides regular payments—usually up to 75% of your salary—if you cannot work due to illness or injury. By contrast, Critical Illness Cover pays a tax-free lump sum when you are diagnosed with a listed serious condition, such as cancer, heart attack, or stroke.

This matters because New Zealanders often underestimate their vulnerability to long-term financial disruption. Statistics New Zealand reports that over 40% of working adults would struggle to meet expenses after just one month without income. In this context, the decision between Income Protection and Critical Illness Cover is not about “if” you should be insured, but “which type—or combination—offers the best fit”.

In this article, we’ll explore how both cover work in New Zealand, compare costs and tax implications, review real case studies, and answer the most common questions so you can make an informed decision.

What Are These Covers?

To understand the choice between Income Protection vs Critical Illness Cover, it helps to break each one down into its essential features. Both serve different purposes, and knowing the basics will make it easier to decide which suits your needs.

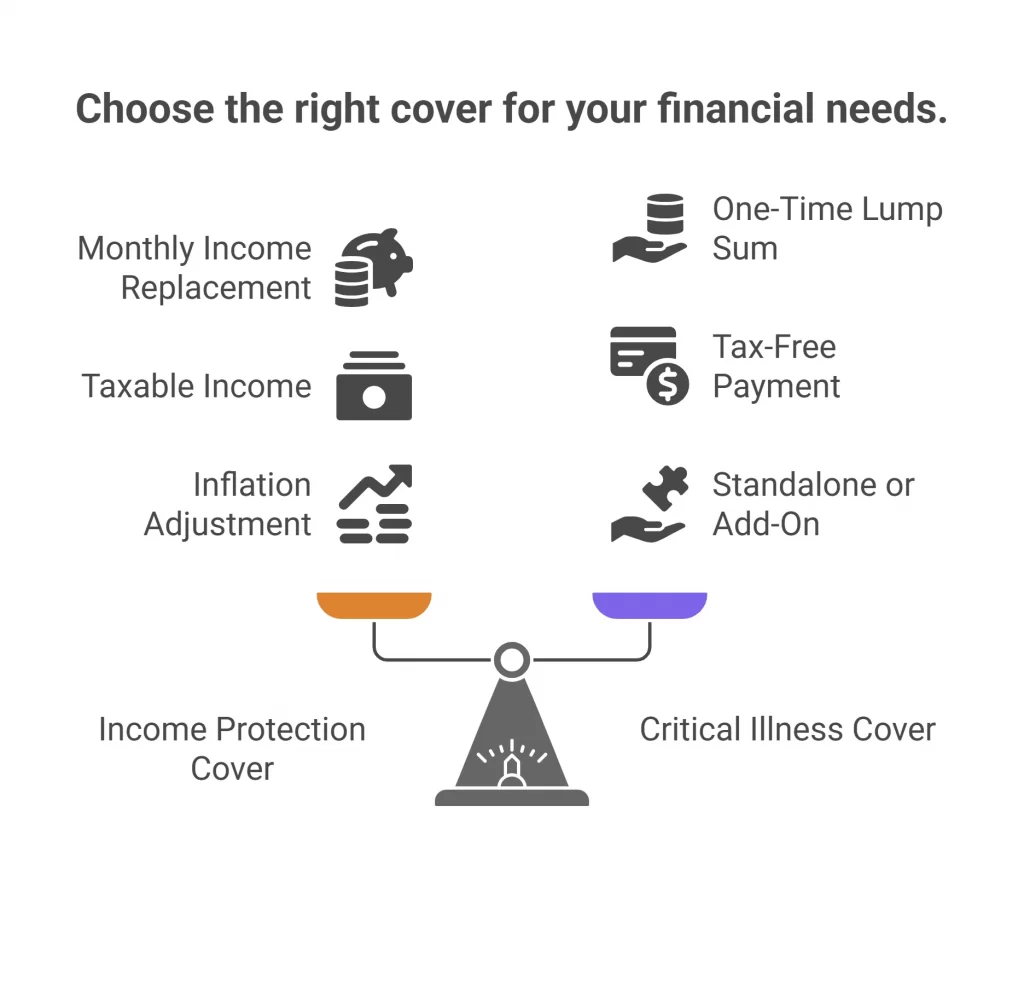

Income Protection Cover

Income Protection is designed to keep your household running when you’re unable to work. In New Zealand, it is one of the most widely recommended forms of personal insurance. Key points include:

- Purpose: Replaces up to 75% of your pre-tax salary if you cannot work due to illness or injury.

- Payment type: Monthly benefit paid for as long as you’re incapacitated, up to the policy’s maximum benefit period (often age 65).

- Waiting period: Payments begin after a waiting period you select—commonly 30, 60, or 90 days.

- Tax Treatment: Payouts are generally taxable as income. Premiums may be deductible in limited cases, such as for some self-employed policyholders, if the policy is classified as ‘loss of earnings’ insurance (Inland Revenue). For most employees, premiums are not deductible.

- Flexibility: The cover adjusts with inflation and can sometimes include add-ons, such as rehabilitation support.

Critical Illness (Trauma) Cover

Critical Illness Cover is also known as Trauma Insurance in New Zealand. Rather than replacing income, it provides a lump sum you can use however you wish. Key points include:

- Purpose: Pays a one-off, tax-free lump sum on diagnosis of a covered serious condition, such as cancer, stroke, or heart attack.

- Payment type: Lump sum delivered shortly after medical confirmation of diagnosis.

- Uses: Funds may be applied to mortgage repayments, medical costs, or lifestyle adjustments.

- Tax treatment: Lump sums are usually tax-free because they are considered capital payments, not income.

- Flexibility: Can be bought standalone or added to life insurance for broader protection.

By understanding these two products — Income Protection and Critical Illness Cover — the debate becomes easier to navigate. One ensures a steady income, while the other provides a financial cushion at a critical moment.

Key Differences in Coverage

When weighing up Income Protection vs Critical Illness Cover, the clearest way to see the contrast is by comparing how they operate in practice. Each has distinct features that shape when and how it supports you.

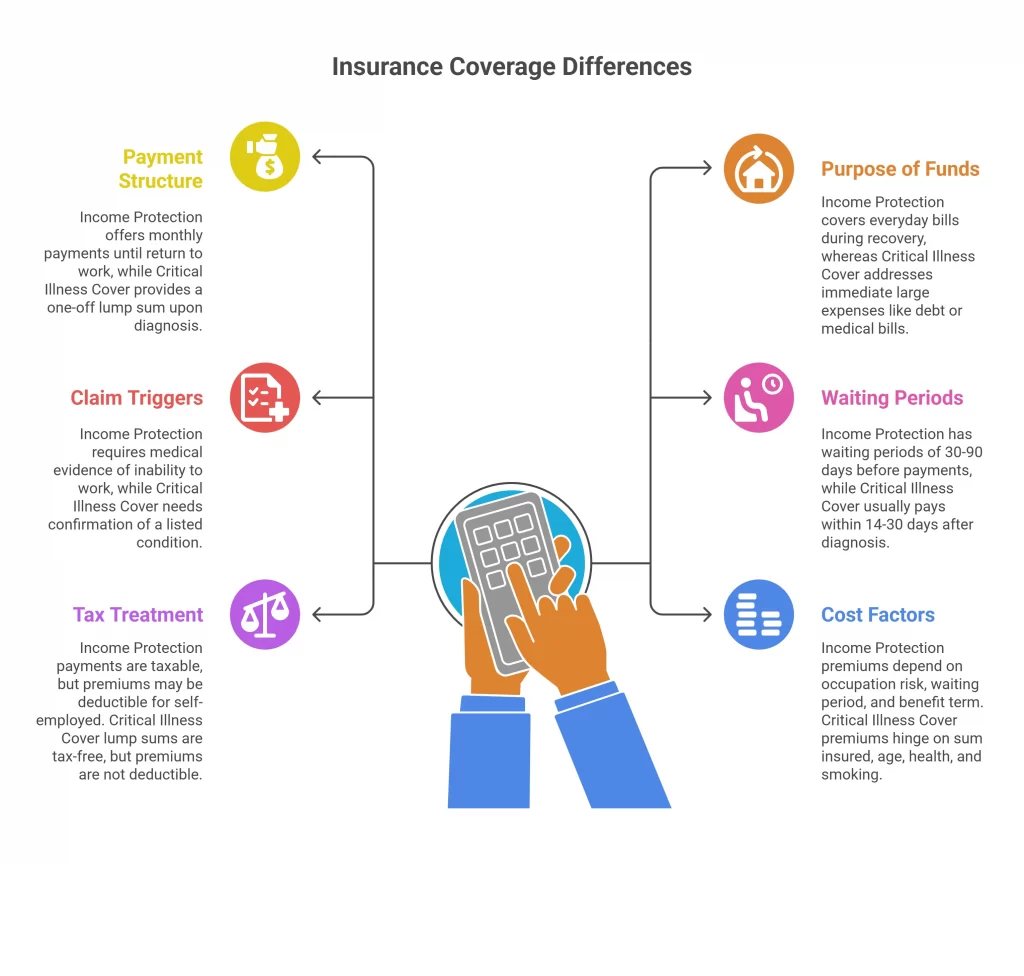

Payment Structure

- Income Protection: Provides ongoing monthly payments, usually 75% of your income, until you return to work or the benefit period ends.

- Critical Illness Cover: Pays a one-off lump sum on diagnosis of a covered condition, regardless of whether you return to work quickly or not.

Purpose of Funds

- Income Protection: Keeps everyday bills, mortgage repayments, and school fees covered during recovery.

- Critical Illness Cover: Designed for immediate large expenses such as clearing debt, paying medical bills, or making home adjustments.

Claim Triggers

- Income Protection: Claim requires medical evidence proving the inability to work due to illness or injury.

- Critical Illness Cover: A claim depends on medical confirmation of a listed condition, such as a heart attack, stroke, or cancer.

Waiting Periods

- Income Protection: Waiting periods range from 30 to 90 days before payments begin—shorter waits result in higher premiums.

- Critical Illness Cover: Usually pays within 14–30 days of diagnosis once claim conditions are satisfied.

Tax Treatment in New Zealand

- Income Protection: Payments are treated as taxable income. Premiums may be deductible for self-employed policyholders (Inland Revenue).

- Critical Illness Cover: Lump-sum payments are tax-free as they are considered capital, though premiums are not deductible.

Cost Factors

- Income Protection: Premiums depend on occupation risk class, chosen waiting period, and benefit term.

- Critical Illness Cover: Premiums hinge on sum insured, age, health history, and smoking status.

Ultimately, the choice of Income Protection or Critical Illness Cover comes down to whether you value ongoing income stability or a tax-free lump sum at a crucial moment.

Real-Life Comparisons

The debate about Income Protection and Critical Illness Cover becomes clearer when we see how real New Zealanders have used these policies during life’s toughest moments. Case studies provide powerful insights into the practical differences.

Case Study 1: Jenny from Auckland

- Situation: Jenny, a 34-year-old primary school teacher in Auckland, slipped and broke her ankle badly while on a hiking trip. She needed surgery and a long recovery, meaning she couldn’t return to her classroom for nearly four months.

- Outcome with Income Protection: Jenny’s Income Protection policy kicked in after her 30-day waiting period. She received 75% of her salary each month, which allowed her to keep paying rent, cover groceries, and avoid dipping into savings.

- Lesson: For Jenny, the steady flow of Income Protection payments gave her the breathing space to recover fully, rather than rushing back to work prematurely. Without it, she admitted she would have relied on credit cards and personal loans.

Case Study 2: Tom from Wellington

- Situation: Tom, a 45-year-old electrician in Wellington, was diagnosed with early-stage bowel cancer. His treatment involved chemotherapy, time off work, and lifestyle changes.

- Outcome with Critical Illness Cover: Tom’s Critical Illness policy provided a lump sum of $200,000. He used this to clear his mortgage, cover treatment costs not fully funded by the public system, and make adjustments to his home.

- Lesson: For Tom, the lump sum allowed him to focus on health without financial anxiety. Even though he was eventually able to return to work, the upfront payout gave him long-term peace of mind.

The Takeaway

These examples illustrate that It’s not about one being “better” than the other. Instead, it’s about which type aligns with your personal circumstances—steady monthly income or immediate financial relief.

See which option works for your lifestyle and budget by comparing policies side-by-side today at CompareIncomeProtection.co.nz.

Cost Considerations in New Zealand

When comparing Income Protection vs Critical Illness Cover, cost is often the deciding factor for many Kiwi households. Both policies protect your financial security, but the way insurers calculate premiums differs significantly.

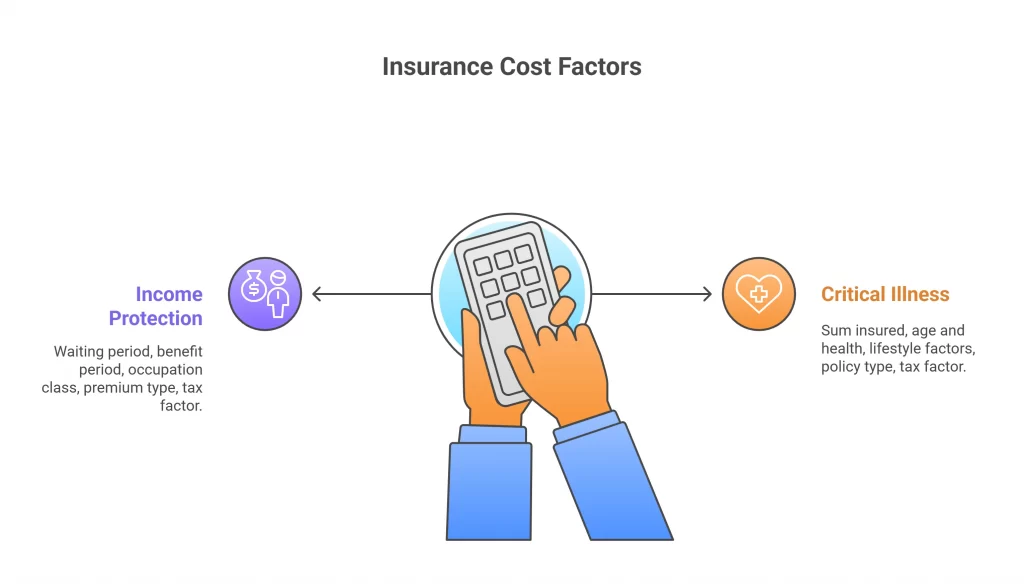

Income Protection Costs

- Waiting period: The shorter your waiting period before benefits start (e.g. 30 days vs 90 days), the higher the premium.

- Benefit period: Cover until age 65 is more expensive than a two- or five-year benefit term.

- Occupation class: High-risk jobs such as construction or electrical work attract higher premiums than office-based roles.

- Level vs. stepped premiums: Level premiums stay consistent but are costlier upfront, while stepped premiums rise with age.

- Tax factor: Inland Revenue allows certain ‘loss-of-earnings’ insurance premiums to be claimed as non-business expenses if payouts are taxable. This typically applies to some self-employed policyholders. For salaried employees, premiums are usually not deductible.

Critical Illness (Trauma) Cover Costs

- Sum insured: The higher your lump-sum payout, the higher your premium.

- Age and health: Older applicants and those with pre-existing conditions pay more.

- Lifestyle factors: Smokers often face significantly higher premiums than non-smokers.

- Policy type: Standalone trauma policies cost more than add-ons bundled with life insurance.

- Tax factor: Premiums are not deductible, but the payout is tax-free as it is considered capital.

Example Scenario

- A 35-year-old non-smoking office worker might pay around $50–$70 per month for $4,000 of monthly Income Protection (with a 90-day wait).

- The same person could pay $40–$60 monthly for $100,000 of Critical Illness Cover.

- Costs rise steeply with age, meaning the earlier you lock in cover, the more affordable it is long term.

Use the free tools at CompareIncomeProtection.co.nz to compare cost scenarios tailored to your occupation, age, and coverage needs.

When Might You Choose One, or Both?

The decision between Income Protection vs Critical Illness Cover is rarely black and white. Each policy serves different needs, and the right choice depends on your personal circumstances, financial responsibilities, and risk tolerance.

When Income Protection Makes Sense

- Regular expenses matter: If your mortgage, rent, and household bills depend heavily on your income, Income Protection ensures continuity.

- Gradual recovery expected: For long-term illnesses or injuries where you might return to work part-time before fully recovering, ongoing payments provide flexibility.

- Self-employed or contractors: Without employer sick leave, Income Protection can replace the safety net you otherwise lack.

- Preference for stability: Some people feel more comfortable with monthly benefits that mimic a salary, rather than a one-off payout.

When Critical Illness Cover Is Better

- Lump-sum needs: If clearing a mortgage, paying for private treatment, or supporting dependants is your main concern, Critical Illness provides immediate funds.

- Short-term shock protection: Even if you expect to recover, the upfront cash can ease financial stress during treatment or rehabilitation.

- Flexibility of use: Unlike monthly benefits, a lump sum gives full discretion on how to allocate funds.

When Combining Both Works Best

- Layered protection: Many financial advisers recommend holding both, as they cover different risks—IP for income flow, CI for large expenses at diagnosis.

- Example: A family in Christchurch may use Income Protection to keep bills paid during an illness while relying on Critical Illness to clear debt and cover medical costs.

- Peace of mind: Having both ensures you won’t need to gamble on which risk is “more likely.”

If you’d like to explore How Much Income Protection Cover In NZ Do You Really Need, see our guide on that for tailored strategies.

Tax & Regulatory Insights in New Zealand

When deciding between income protection and critical illness cover, it’s essential to understand how New Zealand tax law and regulations affect each policy. The rules influence both affordability and the value you ultimately receive.

Tax Treatment

- Income Protection premiums: Inland Revenue may allow certain ‘loss of earnings’ insurance premiums to be claimed as a non-business expense if payouts are taxable. This generally applies to some self-employed Kiwis. For employees, premiums are usually not deductible,

- Income Protection payouts: Treated as assessable income, meaning you’ll pay tax at your marginal rate. This is important to remember when budgeting how much cover you actually need.

- Critical Illness premiums: Generally not deductible, since the payout is considered a capital benefit rather than income.

- Critical Illness payouts: Lump sums are typically tax-free, making them useful for debt repayment or large medical costs.

Regulation and Oversight

- Financial Markets Authority (FMA): The FMA oversees insurers in New Zealand, ensuring product disclosure statements (PDS) are accurate and fair. This helps consumers compare policies on an informed basis.

- Policy wordings: Standardisation across the industry for conditions like heart attack, stroke, and cancer reduces ambiguity when making claims.

- Occupation classes: Insurers classify jobs into risk categories, which heavily affects Income Protection premiums. High-risk roles like builders, electricians, or forestry workers pay more than office-based professionals.

Understanding these tax and regulatory settings ensures that when you compare Income Protection vs Critical Illness Cover, you’re making decisions based not only on premiums and benefits, but also on long-term financial planning.

Read our Income Protection Insurance Tax Deduction guide

Frequently Asked Questions (FAQ)

Choosing between Income Protection vs Critical Illness Cover raises common questions. Here are the answers, tailored for Kiwi policyholders.

Q1: What is the main difference between Income Protection and Critical Illness Cover?

A: Income Protection pays regular monthly benefits if you can’t work due to illness or injury, while Critical Illness Cover provides a tax-free lump sum on diagnosis of a listed serious condition.

Q2: Can I have both Income Protection and Critical Illness Cover?

A: Yes. Many New Zealanders choose to hold both, since Income Protection ensures ongoing cash flow and Critical Illness provides immediate capital for large expenses.

Q3: Are payouts taxed in New Zealand?

A: Income Protection payouts are treated as taxable income, but premiums may be deductible if the cover is classified as loss-of-earnings insurance (Inland Revenue). Critical Illness payouts are generally tax-free, but premiums are not deductible.

Q4: How long is the waiting period for Income Protection?

A: Waiting periods typically range from 30 to 90 days. A shorter wait increases premiums, while a longer wait lowers costs.

Q5: Do I need medical evidence to claim?

A: Yes. For Income Protection, insurers require medical proof that you cannot work. For Critical Illness, diagnosis must meet the specific definition outlined in the policy.

Q6: Is Critical Illness Cover the same as life insurance?

A: No. Life insurance pays on death, while Critical Illness pays during your lifetime if you’re diagnosed with a covered condition. Some insurers allow you to bundle both for efficiency.

Final Thoughts and CTAs

The decision between Income Protection vs Critical Illness Cover is one of the most important financial choices a Kiwi household can make. Both options are designed to protect you when life takes an unexpected turn, but they do so in very different ways.

- Income Protection delivers consistent monthly payments, helping you maintain financial stability when you’re unable to work. It’s particularly valuable if your family relies heavily on your income for ongoing expenses like mortgages, rent, and day-to-day bills.

- Critical Illness Cover provides a tax-free lump sum, giving you the flexibility to pay off debts, fund private treatment, or adapt your lifestyle following a serious diagnosis.

Rather than asking which cover is “better,” the smarter question is: Which one fits my personal circumstances best? For some, a single policy provides the right level of reassurance. For others, combining both products creates a layered safety net—one that covers both immediate shocks and long-term income loss.

New Zealand families are increasingly realising that one type of cover doesn’t fit all. Rising living costs, high mortgage levels, and limited savings mean financial protection is not just an option—it’s a necessity. The peace of mind that comes from knowing your household could cope with either illness or injury is invaluable.

Ready to compare tailored Income Protection policies? Use the free tool at CompareIncomeProtection.co.nz to see options side-by-side.

Methodology (excluded from body word count)

- Tax guidance: Based on Inland Revenue – Non-business expenses.

- Technical ruling: Supported by IRD Tax Technical QB18/04.

- Regulatory oversight: Standards and insurer disclosure requirements from the Financial Markets Authority.

- Case studies: “Jenny” and “Tom” are anonymised composite examples based on common claim scenarios in New Zealand.

- Internal resources: Supporting guides and comparisons from CompareIncomeProtection.co.nz.

{kind=link}

{kind=link}

{kind=link}

{kind=link}