Mortgage Protection vs Income Protection in New Zealand

Mortgage protection vs income protection in New Zealand: which keeps your financial future safe?

Imagine this: You’re working hard to build your life—paying the mortgage, supporting your family, and planning for the future. Suddenly, an illness or accident leaves you unable to work. The bills keep coming, but your income stops. For many Kiwis, this is a nightmare scenario—and it’s precisely why understanding the right insurance is crucial.

In this guide, you’ll get a clear, no-fluff breakdown of mortgage protection vs income protection in New Zealand. You’ll discover:

- How each policy works (and its key differences)

- The pros and cons for homeowners and wage earners

- Real-life examples of each in action

- Tips to choose the cover that matches your lifestyle

Let’s dive in—so you can make a wise, informed choice for your peace of mind.

Understanding Mortgage Protection Insurance

What is mortgage protection insurance in New Zealand?

Mortgage protection insurance is a financial safety net designed to keep your home secure, no matter what happens to your income. If you’re unable to work due to illness or injury, this policy steps in and covers your mortgage repayments for a set period. For most New Zealand homeowners, this could mean the difference between staying in your home and facing foreclosure during tough times.

How Does Mortgage Protection Insurance Work?

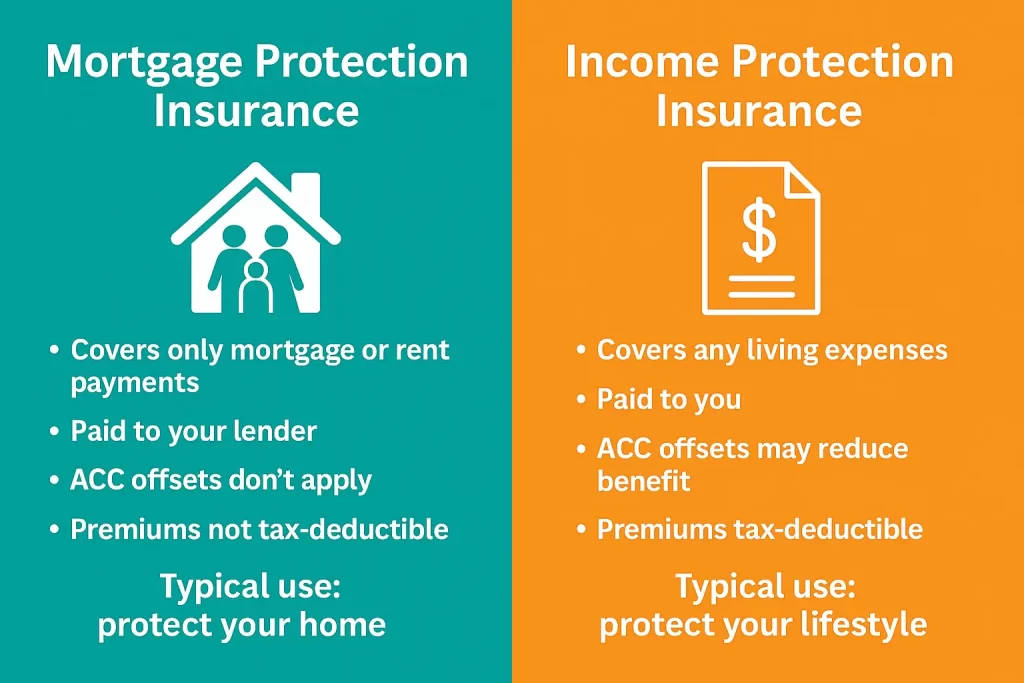

- Pays your mortgage: If you can’t work because of sickness or accident, your insurer pays your mortgage repayments (up to a specified amount, often 115% of your regular mortgage or 45% of your income, whichever is higher).

- Agreed value policies: Many New Zealand policies let you lock in a fixed benefit amount at the start, so you know exactly what you’ll get if you claim—no need to prove income later.

- No ACC offsets: One significant benefit in New Zealand is that, unlike most income protection, mortgage protection often pays out on top of any ACC (Accident Compensation Corporation) benefits you receive after an injury. That means more money in your pocket during recovery.

Who Is It For?

- Homeowners with a mortgage: If your biggest worry is keeping a roof over your family’s head, this policy delivers peace of mind.

- First-time buyers: Mortgage protection can be a key requirement for some lenders or a smart move to protect your new investment.

Pros & Cons

Pros:

- It guarantees your mortgage will be paid, even if you’re out of work for health reasons.

- Payment certainty (especially with agreed value).

- Works alongside ACC benefits.

Cons:

- Only covers your mortgage or rent (not other living expenses).

- Premiums aren’t tax-deductible.

- It usually doesn’t cover redundancy (job loss) or health-related income loss.

Example

Let’s say Sarah, a Hamilton homeowner, is injured in a car accident and can’t work for four months. ACC pays her 80% of her usual wage, but it isn’t enough to cover all her expenses. Her mortgage protection insurance kicks in and pays the full monthly mortgage, ensuring her family stays in their home until she’s back on her feet.

Want to compare your options now?

Use Compare Mortgage Insurance NZ for side-by-side policy comparisons from top New Zealand providers.

Understanding Income Protection Insurance

What is income protection insurance in New Zealand?

Income protection insurance is about keeping your paycheque flowing—even when you can’t work due to illness or injury. Instead of just covering your mortgage, this policy pays you a percentage of your regular income, so you can keep up with bills, groceries, childcare, and everything else life throws your way.

How Does Income Protection Insurance Work?

- Replaces lost income: Most New Zealand policies will pay up to 75% of your usual salary if you can’t work for a medically certified reason.

- Flexible benefit periods: You can choose how long you want to be covered—2 years, 5 years, or until age 65 (more coverage means a higher premium).

- Waiting periods: You can set how long you’ll wait after being off work before payments start, typically between 4 and 13 weeks.

- ACC offsets: Unlike mortgage protection, most income protection payouts are reduced by any ACC payments you receive for an injury (but not for illness).

Who Is It For?

- Anyone with dependents or significant financial commitments: This policy is not just for homeowners. If your household relies on your income, this policy is for you.

- Self-employed Kiwis and contractors: If you’re your boss, you don’t have sick leave to fall back on. Income protection gives you a personal financial safety net.

Pros & Cons

Pros:

- Covers a wide range of living expenses, not just the mortgage.

- It can be tailored to how much you need and for how long.

- Premiums (for indemnity policies) are usually tax-deductible.

Cons:

- Your insurance payout is reduced if you get ACC payments after an injury.

- You need to prove your income at claim time with indemnity-style policies.

- Usually, redundancy is not covered unless you add specific options.

Want to see how top policies compare? Compare income protection insurance in NZ here and get quotes from leading providers—all in one place.

Example

Picture Tom, a self-employed graphic designer in Wellington. He’s diagnosed with a serious illness and can’t work for six months. Because he set up income protection insurance, Tom receives 75% of his regular income, so he can keep paying rent, groceries, and even his business expenses while he recovers.

Key Differences Between Mortgage Protection and Income Protection Insurance

On the surface, mortgage protection vs income protection insurance sounds similar. Both kick in when you can’t work. But digging deeper, you’ll find some critical differences—knowing them could save you thousands (or your home).

1. What They Cover

- Mortgage Protection:

Only your mortgage (or sometimes your rent). Payments go directly toward your lender, ensuring your house is safe from repossession.

- Income Protection:

A percentage of your regular income is paid straight to you. Use it for anything—mortgage, rent, food, car payments, school fees, you name it.

2. How Benefits Are Calculated

- Mortgage Protection:

Usually, an “agreed value” (e.g., your regular mortgage payment or a fixed portion of your income) is set when you start the policy.

- Income Protection:

Usually, a percentage of your pre-disability income, commonly up to 75%. Some policies require proof of income at claim time (indemnity), while others lock in a set amount (agreed value).

Learn more about How Much Income Protection Cover In NZ Do You need?

3. What Happens If You Get ACC Payments

- Mortgage Protection:

You get your full insurance benefit and your ACC payout. No deductions.

- Income Protection:

ACC payments reduce your insurance payout, so you don’t “double dip.”

4. Tax Treatment

- Mortgage Protection:

Premiums are not tax-deductible, but any payouts you receive are tax-free.

- Income Protection:

Premiums for indemnity policies are tax-deductible (a win at tax time), but payouts are taxed as income. For agreed-value policies, premiums are not tax-deductible, but payouts are tax-free.

5. Flexibility and Usage

- Mortgage Protection:

Keeps your home safe, but doesn’t cover living costs beyond your mortgage.

- Income Protection:

Far more flexible—you choose how to spend the payout.

6. Who Should Consider Each?

- Mortgage Protection:

Perfect if your main worry is losing your house and you want to lock in those payments.

- Income Protection:

This is ideal if you want more control over your finances during tough times, especially if you have dependents or big expenses beyond your mortgage.

Quick Table for Mortgage Protection vs Income Protection

| Feature | Mortgage Protection | Income Protection |

| Covers | Mortgage/rent only | Any expenses (up to 75% of income) |

| Payout Type | Fixed amount (agreed value) | Indemnity or agreed value |

| ACC Offsets | No | Yes |

| Premiums Tax Deductible | No | Indemnity: Yes / Agreed: No |

| Who Gets Paid | Lender (or you for rent) | You |

Now, readers know the details of the differences to determine which policy (or combination) best suits them.

Want a tool to help decide?

See Compare Mortgage Insurance NZ for the latest mortgage cover, or Compare Income Protection for NZ’s top income protection quotes.

Factors to Consider When Choosing Insurance

Understanding the policies is one thing, but how do you choose the right cover for your life? Here’s what you need to weigh before signing on the dotted line.

1. Your Financial Priorities

- Is your mortgage your #1 stress point?

If losing your home is your biggest fear, mortgage protection is a direct solution.

- Do you have lots of other expenses?

Income protection offers broader coverage if your family relies on your income for groceries, utilities, schooling, and more.

2. Your Income and Employment Type

- Self-employed or contractor?

Fluctuating income is tricky at claim time. Agreed value income protection policies can lock in what you’ll receive—no messy paperwork later.

- Full-time employee?

Indemnity income protection is often cheaper and can fit well with a stable salary.

Read more about self-employed income protection.

3. Your Current Coverage and Safety Nets

- Do you have other insurance?

Double-check you’re not overlapping with employer benefits, life insurance, or trauma cover.

- Relying on ACC?

Remember, ACC only covers accidents, not illnesses. If you get sick, mortgage or income protection steps in.

4. Family and Dependents

- Are you supporting a partner, kids, or ageing parents?

The more people relying on your income, the more critical it is to protect it.

5. Tax Implications

- Looking for a tax break?

Indemnity income protection premiums are usually tax-deductible—this could reduce your tax bill, especially if you’re self-employed.

6. Policy Flexibility

- Waiting and benefit periods:

Can you survive a few weeks without pay, or do you need coverage to start immediately?

Would you rather be covered for 2 years or until retirement age?

(Longer benefit periods = higher premiums, but more security.) - How much cover do you need?

Work out your budget: mortgage, bills, food, school, car. The right policy fills the gaps.

7. Cost vs. Peace of Mind

- Can you afford the premiums?

The best policy in the world won’t help if you can’t keep up the payments. Find a balance that gives you peace of mind, not extra stress.

Quick Action Step

List your most significant financial risks, current insurances, and what you want most from a policy. Bring it to your adviser—they’ll help you map out the best cover for your unique needs.

Combining Both Insurances: Is It Beneficial?

Here’s a common mistake: People think they must pick just one—mortgage or income protection. But the truth is that combining both can create a robust financial shield for many New Zealanders.

Why Combine Both?

- Double-layered security:

Mortgage protection guarantees the safety of your home. Income protection ensures the rest of your life (groceries, utilities, school fees, car payments) keeps running, too.

- Bridges the gaps:

If you’re out of work, your mortgage may be your biggest expense—but not your only one. Income protection covers everything else, so you’re not scrambling to pay for basic needs.

- Works with your budget:

You can tailor the level of each cover to fit your priorities and what you can afford.

Who Should Consider Both?

- Homeowners with dependents:

This combo covers your bases if you have a family, a mortgage, and bills to pay.

- Self-employed or high-earners:

Combining both insurances can provide a more predictable safety net if your income is inconsistent or above the average ACC payout.

- Anyone who wants maximum peace of mind:

If you never want to worry about “what if I can’t work?” again, doubling up is the way to go.

Real-Life Example

Joe and Hana are a young couple in Auckland with a hefty mortgage, two kids, and busy careers.

- Joe takes out mortgage protection so the house is safe no matter what.

- Hana gets income protection to cover household bills and their kids’ school fees.

When Joe gets a serious illness and can’t work, the mortgage insurance covers their home loan, while Hana’s income protection pays for day-to-day living, keeping their family stable during a tough year.

Tips for Making the Combo Work

- Don’t over-insure:

Talk to a qualified adviser to ensure your total benefits don’t exceed what you need (or what insurers will pay out).

- Review annually:

Your mortgage will change, and so will your income. Update your cover as your life evolves.

- Understand exclusions:

Ensure you know when each policy kicks in—and if there’s any overlap or waiting period.

Combining both types of insurance is like having seatbelts and airbags: you hope you’ll never need them, but when life throws the unexpected your way, you’ll be glad you’re protected from every angle.

Real-Life Scenarios: How the Right Insurance Saves the Day

Let’s get real: Insurance jargon can make anyone’s head spin. So, here are three scenarios that show precisely how Mortgage Protection vs Income Protection play out in the real world for New Zealanders like you.

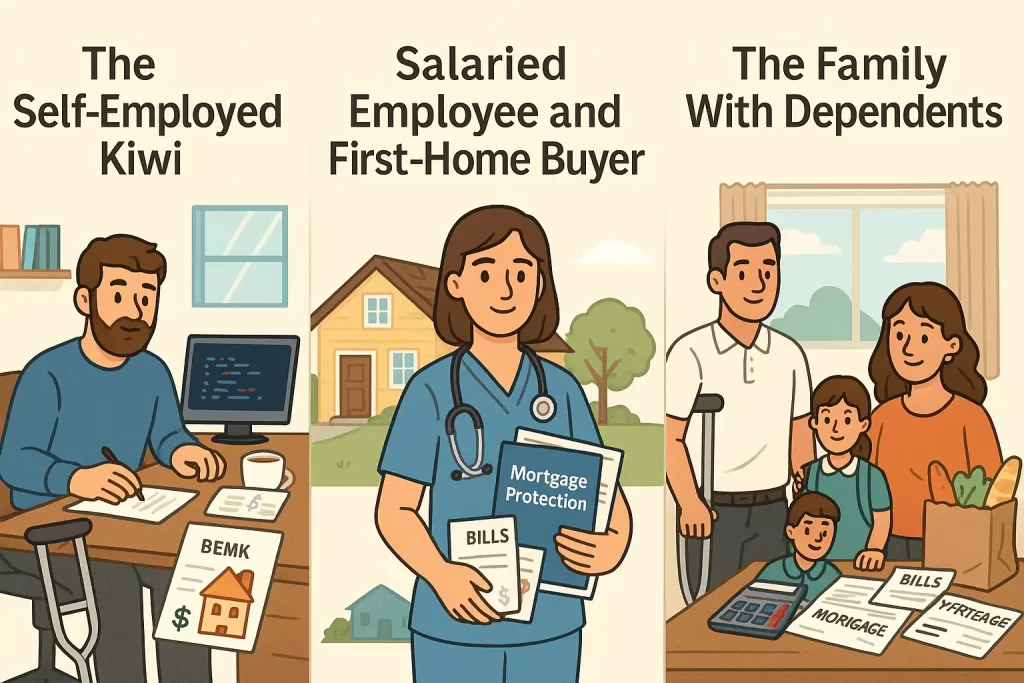

Scenario 1: The Self-Employed Kiwi

Meet Alex.

Alex is a freelance web developer in Tauranga. He works from home, has a home office, and pays a monthly mortgage.

- What goes wrong:

Alex falls off his mountain bike and fractures his leg. He can’t work for three months. - How the insurance works:

- Mortgage protection: Pays Alex’s mortgage, so he doesn’t worry about losing his home.

- Income protection: Pays 75% of his regular earnings, covering groceries, utilities, and business expenses.

Takeaway:

Self-employed Kiwis need both policies for complete coverage, especially when sick leave or employer benefits aren’t an option.

Scenario 2: The Salaried Employee and First-Home Buyer

Meet Sophie.

Sophie just bought her first home in Christchurch. She’s a salaried nurse who wants to ensure nothing jeopardises her most significant investment.

- What goes wrong:

Sophie is diagnosed with a severe illness and needs to stop working for several months. - How the insurance works:

- Mortgage protection: Takes care of her mortgage payments directly.

- Income protection (if she chooses it): The government pays her a portion of her income, which she can use for medical bills, groceries, and day-to-day costs.

Takeaway:

If you’re focused on keeping your home, mortgage protection is key. But income protection fills the gaps and helps you stay afloat.

Scenario 3: The Family With Dependents

Meet the Ngatai Family.

Parents Mark and Lisa live in Hamilton, where they have two kids, a mortgage, and plenty of monthly bills.

- What goes wrong:

Mark suffers a back injury and can’t work for a year. - How the insurance works:

- Mortgage protection: Keeps their mortgage paid, so the family home is secure.

- Income protection gives them extra cash to pay for their children’s school fees, groceries, transportation, and other expenses.

Takeaway:

Both policies can be a lifesaver for families, reducing stress during a challenging time.

Pro Tip

Think about your own life:

Are you self-employed, a first-home buyer, or supporting a family? Picture which scenario fits you best, then match your insurance to your real risk.

Frequently Asked Questions about Mortgage Protection vs Income Protection

1. What’s the difference between mortgage protection vs income protection insurance in New Zealand?

Mortgage protection pays your mortgage if you can’t work due to illness or injury.

Income protection replaces a percentage of your regular income, so you can pay for everything—mortgage, rent, bills, groceries, and more.

2. Do I need both mortgage protection and income protection?

Both policies are smart if you want your mortgage and other living expenses covered, especially if you have dependents or big financial commitments. Some people choose just one, but combining the two gives more complete protection.

3. Will these policies pay out if I lose my job?

Usually, no. Both mortgage and income protection in New Zealand are designed for loss of income due to illness or injury, not redundancy or dismissal. Some insurers offer optional redundancy cover, but it’s less common and may have stricter terms.

4. How do ACC payments affect my insurance payout?

- With mortgage protection, you typically get the full benefit, even if you also receive ACC.

- With income protection, whatever ACC pays you for an accident usually reduces your insurance payout. Your full insurance benefit kicks in for illness (not covered by ACC).

5. Are the premiums tax-deductible?

- Income protection (indemnity policies): Premiums are usually tax-deductible, but payouts are taxed as income.

- Mortgage protection: Premiums are generally not tax-deductible, but payouts are tax-free.

6. How long do the payments last?

You choose your benefit period—from 2 to 5 years or even to age 65. The longer the period, the higher the premium.

7. What if my income changes after I take out a policy?

- Agreed value policies lock in your benefit amount, even if your income drops.

- Indemnity policies will pay out based on your actual income when you claim, so if your earnings go down, your payout may too.

8. How do I decide how much cover I need?

Add up your non-negotiable monthly expenses (mortgage/rent, food, power, school fees, insurance). Choose a policy—or combination—that will cover these essentials if you cannot work.

9. How do I make a claim?

Contact your insurer when you know you’ll be off work longer than your policy’s waiting period. You’ll usually need a doctor’s note and paperwork proving your income (for income protection).

10. Can I change or cancel my policy later?

Absolutely! You can review ” How Does [Policy] Insurance Work?, adjust, or cancel your insurance anytime. It’s smart to check your policies yearly or after any significant life change.

Still have questions?

Speak with a licensed insurance adviser or visit trusted New Zealand insurance comparison sites for up-to-date, personalised advice.

Conclusion & Action Steps: Protect Your Future Today

You’ve just learned the real-world differences between mortgage protection vs income protection in New Zealand. Here’s the big takeaway:

Mortgage protection protects you against losing your home when you’re too sick or injured to work.

When life hits pause on your paycheque, income protection is your safety net for everything else—from bills to groceries to the kids’ activities.

The smartest move?

Choose the cover that fits your biggest risks. If your income is your foundation, income protection is crucial. If keeping your home is priority #1, mortgage protection deserves a look. For many Kiwis, a combination is the golden ticket to true financial peace of mind.

Here’s How to Take Action Right Now:

- Review your own situation:

- What would happen if your income stopped tomorrow?

- Could you keep paying your mortgage? Your bills? Support your family?

- Make a simple list:

- What are your monthly non-negotiables? (Mortgage, rent, power, food, insurance, school costs, etc.)

- Do you have sick leave or employer coverage?

- Is your income steady, or does it go up and down?

- Talk to a pro:

Don’t go it alone. A licensed insurance adviser can help you work out precisely what you need—no more, no less. They’ll explain the fine print and find ways to save on premiums. All financial advisers in New Zealand are now regulated under the Financial Markets Conduct Act (since 2021) to ensure high standards and consumer protection. You can check your adviser’s licence and credentials on the Financial Markets Authority’s register. - Review regularly:

Your life will change. Get in the habit of checking your cover each year (or after big life changes like buying a house, changing jobs, or having a baby).

Final Thought

Don’t let uncertainty threaten your hard work. You can weather any storm with the right insurance strategy, knowing your home, income, and family are protected.

Ready to take the next step?

Book a chat with a trusted New Zealand insurance adviser today—and get peace of mind for whatever tomorrow brings.

Disclaimer

The information provided in this article is for general informational purposes only and is not intended as financial, insurance, or legal advice. While every effort has been made to ensure accuracy, insurance policies and regulations may change, and individual circumstances vary. Before making any insurance decisions, please consult a qualified insurance adviser or financial professional who can provide guidance tailored to your needs and situation. The author and publisher accept no responsibility for any loss, claim, or liability that may result from the information provided.

{kind=link}

{kind=link}

{kind=link}