The Income Protection Insurance Tax Deduction -2025 Guide

In life, unexpected illnesses or accidents can prevent you from working and earning an income, and that’s where income protection insurance comes in. This type of policy is designed to replace a portion of your income if you’re unable to work due to health-related issues, helping you cover day-to-day expenses and maintain financial stability.

One important aspect that many Kiwis overlook is the income protection insurance tax deduction. In New Zealand, under certain conditions, the premiums you pay for this kind of insurance may be tax-deductible, reducing your overall tax burden. But there are key rules and distinctions to understand, especially depending on your employment type and the structure of your policy.

Whether you’re a salaried employee, a self-employed freelancer, or a contractor, understanding how the income protection tax-deductible system works could make a noticeable difference at tax time.

🔗 For more information on how income protection works and who it’s right for, read What Is Income Protection Insurance in NZ

What Is Income Protection Insurance?

Income protection insurance is designed to pay you a monthly benefit if you’re unable to work due to illness or injury. In New Zealand, it’s commonly used by both employees and self-employed individuals to ensure that essential bills, like rent or mortgage, groceries, and utilities, can still be paid even when income stops.

Policies typically cover up to 75% of your usual income, and payments usually begin after a waiting period (such as 4 or 8 weeks) and continue for a set benefit period — anywhere from 6 months to several years, depending on your policy. Understanding how the income protection insurance tax deduction works is a crucial aspect of managing this valuable coverage

Types of Cover: Indemnity vs Agreed Value

When choosing an income protection policy, you’ll typically select from one of two structures:

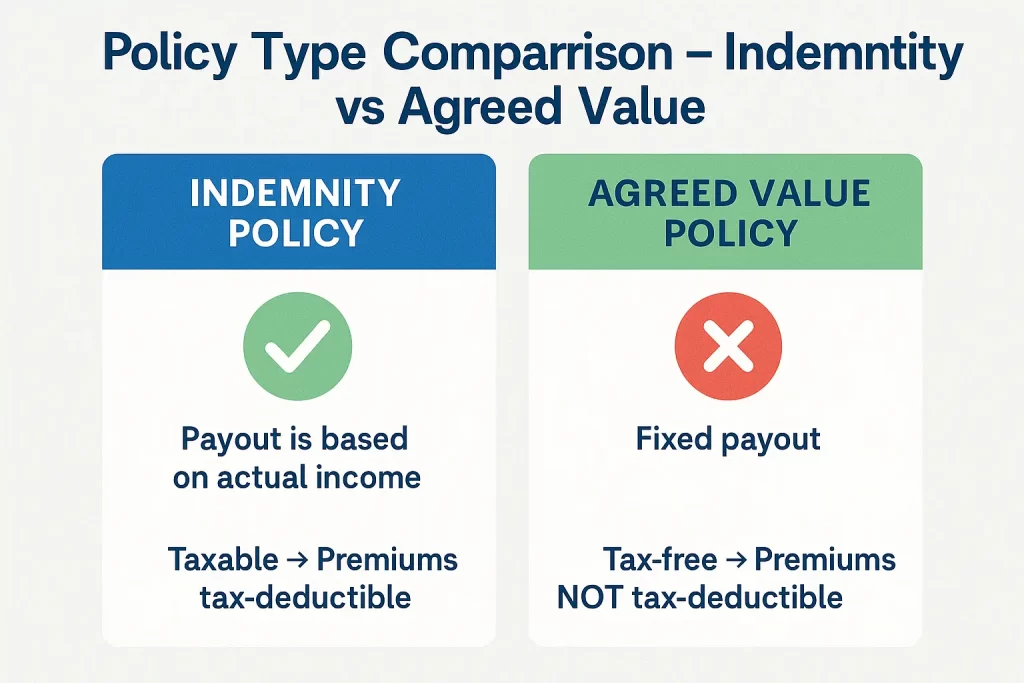

- Indemnity Value: The benefit amount is based on your actual income at the time of the claim. This type of policy is often more affordable, and in most cases, the premiums are income protection tax-deductible because payouts are taxable.

- Agreed Value: You agree on a benefit amount when you take out the policy, regardless of fluctuations in your income. While this offers more predictability, it’s usually more expensive, and the premiums are often not tax-deductible because payouts may be tax-free.

Why It Matters for Employees and the Self-Employed

For salaried employees, income protection can supplement employer-provided sick leave or accident compensation, such as that provided by the Accident Compensation Corporation (ACC). However, for contractors, freelancers, and small business owners, this coverage is often essential, as there is no fallback income if they’re unable to work.

Explore your income protection options and learn more about self employed income protection

Is Income Protection Insurance Tax Deductible in NZ?

A common question Kiwis ask is whether they can claim an income protection insurance tax deduction.

The short answer is: yes, but only under specific conditions.

According to Inland Revenue (IRD), income protection insurance premiums in New Zealand can be tax deductible only if the benefit you receive is taxable income. This usually applies to Indemnity value policies, where the payout reflects your actual earnings at the time of the claim. Since those payouts are taxed as income, the premiums can generally be claimed as a non-business expense on your individual tax return.

✅ When Are Income Protection Premiums Tax Deductible?

You can claim premiums if:

- You have an indemnity policy, and

- The policy benefit is treated as taxable income when paid out.

This is particularly common for self-employed individuals, sole traders, and contractors whose income varies and who rely on indemnity-based policies to match their earnings.

❌ When Are They Not Deductible?

If your policy is an agreed value policy — where the payout is fixed and typically tax-free — you cannot claim the premiums. IRD’s position is straightforward: if the payout isn’t taxed, the premium isn’t deductible.

📌 Real-Life Example

- Emma (Salaried Employee)

She holds an indemnity policy replacing 75% of her income. Her benefit is taxed, so she claims the premiums as a deduction each year. - Jason (Freelancer)

Opted for a more expensive agreed value policy for a fixed benefit. Because his payout is tax-free, he cannot deduct the premium.

If you’re unsure about your policy type or tax status, consult your insurance provider or a tax advisor to ensure you’re claiming correctly.

🔗 Ready to explore policies that may qualify for a tax deduction? Visit Compare Income Protection NZ to compare your options.

Self-Employed: How to Claim a Tax Deduction

If you’re self-employed in New Zealand — whether you’re a sole trader, freelancer, or contractor — the rules around claiming deductions for income protection insurance are especially important to understand.

For many sole traders and freelancers, the income protection insurance tax deduction offers a valuable tax saving each year

Because you don’t receive employer-provided sick leave or accident compensation beyond ACC, income protection insurance can serve as a vital safeguard. In many cases, your premiums may also be eligible for a tax deduction, providing you with both protection and a potential tax refund.

✅ When You Can Claim

Suppose your policy is structured so that any benefit you receive is taxable. In that case, you can typically claim your premiums as a non-business expense on your personal income tax return. This applies to most indemnity-style policies.

💼 How to Claim

- Log in to your myIR account on the IRD website

- Navigate to your income tax return (IR3 or IR3NR for self-employed individuals)

- Go to the “Other Deductions” or “Non-Business Expenses” section

- Enter the total annual premium paid for eligible income protection insurance

Be sure to keep a certificate or summary of premiums from your insurer in case the IRD requests documentation.

🧾 GST Considerations

If you’re GST-registered, you can’t claim GST back on your premiums unless your income protection insurance is used strictly for business income (which is rare). Most individuals should treat these premiums as personal expenses, not business costs, even if you’re self-employed.

🔍 Pro Tip

Always review your policy details carefully. If the benefit is not taxable, such as with many agreed value policies, your premiums won’t be deductible, regardless of your employment status.

📎 For broader self-employment financial planning, check the FMA – Self-Employed Financial Guidelines

🔗 Compare income protection plans tailored for the self-employed at Compare Income Protection NZ

Step-by-Step: How to Claim Your Deduction

Once you’ve confirmed that your income protection insurance premiums are tax deductible — typically because the benefit is taxable — the next step is to ensure you claim them correctly with Inland Revenue (IRD).

Here’s a simple, step-by-step guide to help you through the process:

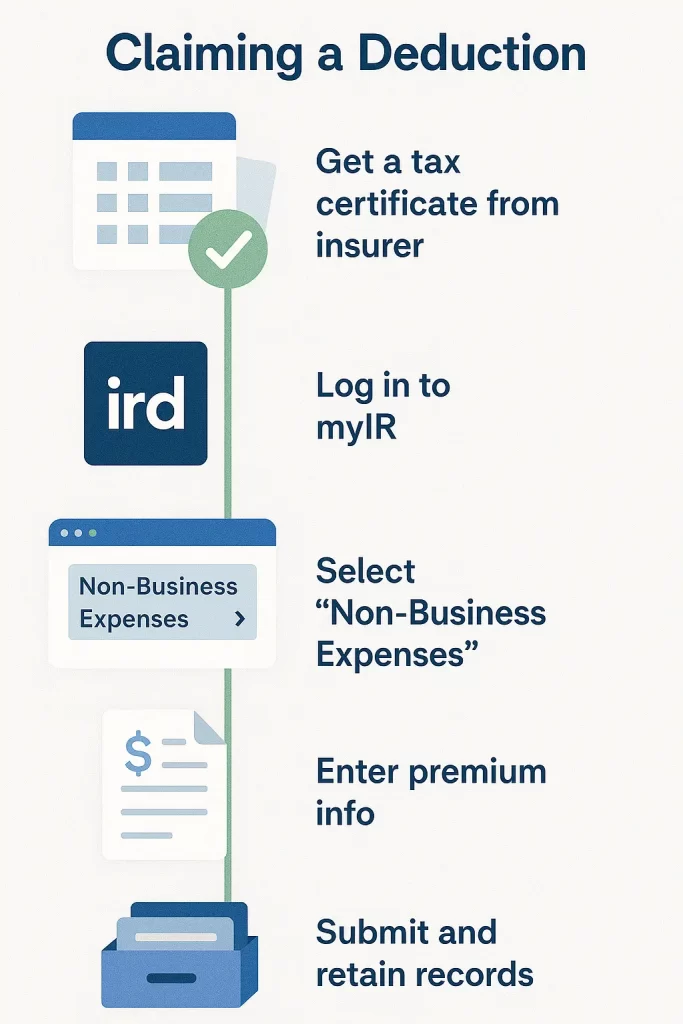

✅ Step 1: Get a Premium Certificate from Your Insurer

At the end of the financial year, most insurers will issue a statement or certificate showing the total premiums you paid. This document is necessary for record-keeping and required if IRD requests proof of your claim.

- Tip: Ask your insurer directly if they don’t send it automatically.

✅ Step 2: Log in to your myIR Account

Head to myIR and log in using your IRD credentials. This is where you’ll file your individual tax return (usually the IR3 form for self-employed people or those with extra income).

✅ Step 3: Locate the “Non-Business Expenses” or “Other Deductions” Section

Within your return, scroll to the section for non-business expenses (for individuals) or “other deductions.” This is where income protection premiums that meet IRD’s criteria can be entered.

- Make sure you only claim the portion of the premium related to taxable benefits.

- Do not include life insurance or non-taxable policy costs — these are not deductible.

✅ Step 4: Submit and Retain Records

After entering the deduction, submit your return and retain all supporting documents for at least seven years, in case of an audit or IRD query.

🔗 Need help choosing a policy with tax-deductible benefits? Visit Compare Income Protection NZ to find the right income protection coverage for your situation.

What If Your Employer Pays for It?

If your employer pays for your income protection insurance, the tax treatment is different compared to when you pay for the policy yourself. While the cover still provides valuable financial protection, the implications for deductions and taxable income shift, and Fringe Benefit Tax (FBT) may come into play.

🧾 Employer-Paid Premiums and Fringe Benefit Tax (FBT)

When an employer pays premiums on your behalf, those payments are generally considered a fringe benefit unless the cost is passed back to you. That means the employer is responsible for paying FBT to Inland Revenue, not you.

In this case:

- You cannot claim the premium as a personal tax deduction.

- The employer may need to account for the cost in their FBT return, depending on the policy’s structure.

🔄 PAYE vs FBT

There are two possible scenarios for employer-paid policies:

- Fringe Benefit Tax (FBT) Applied

- The employer pays the premium.

- It is treated as a fringe benefit.

- Employer pays FBT; the benefit is not included in your PAYE income.

- PAYE Applied Instead

- If the premium is added to your salary or wage, it becomes part of your taxable income, subject to PAYE.

- In this case, you’re effectively paying for it, and you may be able to claim a deduction if the benefit is taxable.

📌 Who Reports the Income?

- Employer: Reports and pays FBT if the policy is a fringe benefit.

- Employee: If the premium is passed on to you (as PAYE income), it should be visible in your payslip or earnings summary, and you may be able to claim if applicable.

This setup highlights the importance of understanding how the policy is structured and whether it’s classified as an employer-paid benefit or taxable income.

🔗 Want to compare personal vs employer-funded policies? Use the comparison tool at Compare Income Protection NZ

Mistakes to Avoid

When it comes to claiming tax deductions on income protection insurance in New Zealand, minor oversights can lead to missed refunds — or worse, incorrect filings that raise red flags with Inland Revenue (IRD). Here are some of the most common mistakes to watch out for:

❌ Claiming the Wrong Type of Policy

Not all income protection policies are tax deductible. The most common error is trying to claim premiums from Agreed Value policies, where the benefit is typically tax-free. Remember, the IRD only allows a deduction if the payout is taxable income, which is usually the case with Indemnity policies.

If you’re unsure, ask your insurer for clarification or check your annual premium certificate — it should indicate whether the benefit is taxable or not.

❌ Failing to Report Payouts as Income

If you do receive income protection payments from a taxable policy, you must report them as part of your annual income. Forgetting to do so can result in under-reporting, penalties, or issues during an audit.

Keep all claim payout records and include them in your income section when filing your tax return via myIR.

❌ Confusing Life Insurance with Income Protection

Life insurance and income protection are distinct, and their tax treatment differs significantly. Life insurance premiums are generally not tax-deductible in New Zealand, and the benefits are paid upon death, not during a period of disability or illness.

Income protection, on the other hand, is about maintaining your income while you recover, and only some policies qualify for a tax deduction.

It’s essential to understand the rules around the income protection insurance tax deduction to avoid incorrect claims

🔗 Compare tax-deductible income protection options at Compare Income Protection NZ

FAQs

Here are answers to some of the most frequently asked questions about income protection insurance and tax deductions in New Zealand:

1. Is income protection insurance tax deductible in NZ?

Yes, if the policy’s payouts are taxable income, typically with indemnity value policies.

2. Can self-employed individuals claim income protection premiums?

Yes, self-employed individuals can claim premiums if the policy’s benefits are taxable income.

3. How do I claim a deduction for income protection premiums?

Obtain a tax certificate from your insurer and enter it in ‘non-business expenses’ in your myIR account.

4. Do I need to pay tax on income protection payouts?

Yes, if the premiums were tax-deductible, the payouts are considered taxable income.

5. Is agreed value income protection insurance tax deductible?

Generally, no; since the benefits are tax-free, the premiums aren’t deductible.

6. Can I claim income protection premiums if my employer pays them?

If the employer-paid premiums are considered a fringe benefit, they may be subject to FBT, and you cannot claim them.

7. Is income protection insurance subject to GST?

Yes, premiums include GST; if you’re GST-registered, you may be eligible to claim it back.

8. Can I claim premiums for life insurance or trauma cover?

No, premiums for life or trauma insurance aren’t tax-deductible in New Zealand.

9. What documentation do I need to claim the deduction?

A tax certificate from your insurer detailing the premiums paid and confirmation that the benefits are taxable.

10. Does income protection insurance cover mental illness?

Yes, most NZ income protection policies include cover for mental health conditions like anxiety and depression, if they stop you from working.

Conclusion

Understanding the rules around the income protection insurance tax deduction in New Zealand can make a real difference in how you manage both your risk and your finances. While not all policies qualify, knowing when your income protection tax-deductible status applies, especially for self-employed Kiwis and contractors, empowers you to make smarter insurance and tax decisions.

To recap:

- Indemnity policies with taxable benefits are generally deductible.

- Agreed-value policies with tax-free payouts are usually not.

- Always check your policy type and consult IRD guidelines before filing a claim.

- Maintain proper documentation and consider professional tax advice to avoid errors.

If you’re unsure whether your current policy is eligible, or you’re just getting started, comparing the right plan can save you money now and at tax time.

✅ Ready to compare the best income protection insurance policies in NZ?

Compare policies now to find the right cover and see what you can claim on tax.

{kind=link}

{kind=link}

{kind=link}