How to Choose the Best Income Protection Policy in New Zealand

Key Takeaways

- Low Uptake of Income Protection

Private income protection coverage in New Zealand is very low, with only 14% of people holding either income or mortgage protection insurance, according to MBIE research on social insurance. - ACC Doesn’t Cover Illness

ACC provides cover only for injury-related income loss. Illnesses are excluded, meaning Kiwis must rely on private policies. - Tax Treatment of Premiums and Payouts

When an employer pays premiums, they may claim a deduction, and the premiums are not subject to PAYE or FBT. However, claim payouts are taxable income, according to IRD’s official tax guidance (QB 18/04). - Tax Deductibility for Individuals

Individuals may claim the cost of income protection insurance as a non-business expense, but only if any payout is taxable, per IRD’s non-business expenses guide. - Underinsurance Concerns

Māori and other groups in New Zealand are disproportionately underinsured. The Retirement Commission confirms Māori have the lowest levels of insurance uptake in the country.

Choosing the best income protection policy is one of the most important financial decisions Kiwis can make. In New Zealand, only 14% of people hold income or mortgage protection insurance, leaving most households vulnerable to sudden income loss. With ACC covering accidents but not illness , private policies fill a crucial gap. This guide explains how to compare providers, features, and tax rules to secure your financial future.

Curious about policies tailored for your situation? Compare income protection policies now and find your best match

What ‘Best’ Means for Income Protection in NZ

The best income protection policy in New Zealand is not a one-size-fits-all choice—it depends on personal income, occupation, health, and household commitments. Income protection insurance provides regular payments if you’re unable to work due to illness or injury, ensuring you can continue covering essentials such as housing, food, and debt repayments.

Unlike ACC, which only covers accidents, private income protection policies extend coverage to illnesses, mental health conditions, and other non-accident causes of lost income. This distinction makes private insurance a vital safety net for many working New Zealanders.

When defining what “best” means, Kiwis should weigh:

- Waiting period: How long before payments begin?

- Benefit period: The duration of the payments.

- Payout level: The percentage of your income replaced.

- Exclusions: Conditions or circumstances not covered.

The best income protection policy is ultimately the one that strikes a balance between affordability and comprehensive coverage tailored to your lifestyle, family, and financial responsibilities.

NZ Market Snapshot — Uptake, Waiting Periods & Benefit Options

An income protection policy must be considered in light of the broader New Zealand market. Despite the financial risks of losing income, uptake remains low. Research commissioned by MBIE found that only a few of New Zealanders hold income or mortgage protection insurance. This indicates that most households would need to rely on savings or limited government support if their earnings stopped.

Policy design is another defining factor. Submissions on the proposed New Zealand Income Insurance Scheme reveal that waiting periods—the time before payments begin—commonly sit around 13 weeks. Some proposals suggest extending this to seven months, which could lower premiums by 10–20%. For many families, however, a longer wait could leave them vulnerable if savings are already stretched.

Benefit periods, or the duration during which income is replaced, also vary significantly. The most common options range from two years up to age 65, ensuring long-term protection for those facing extended illness or disability. Choosing the right benefit period is one of the most critical decisions when evaluating the best policy.

Another pressing issue is underinsurance among Māori and other communities, who face both lower levels of insurance uptake and higher financial vulnerability. The Retirement Commission confirms that Māori have the lowest insurance participation rates in the country (Retirement Commission). This highlights the need for culturally sensitive financial advice and policies that better serve diverse communities.

In summary, the New Zealand market exhibits both low uptake and high variability in policy design, making a careful comparison essential for finding the income protection policy that suits individual circumstances.

With only a short percentage of Kiwis protected, now’s the time to compare and close the coverage gap—Start comparing policies here

Why Every Kiwi Should Consider a Policy

The best income protection policy isn’t just a luxury—it’s a financial safeguard that many New Zealand households urgently need. Despite the risks, only 14% of people currently hold income or mortgage protection insurance (according to MBIE). This leaves the majority of Kiwis financially exposed if they can’t work due to illness or disability.

New Zealand’s high cost of living makes this gap particularly concerning. According to Statistics New Zealand (Stats NZ), over 45% of renting households and more than 26% of owner-occupiers spend 30% or more of their income on housing costs . With household debt sitting at historically high levels relative to disposable income (RBNZ), even a few weeks without income can push families into hardship.

While ACC provides income support for accident-related injuries, it does not cover illnesses, which are a significant cause of time off work. For example, conditions like cancer, heart disease, or mental health challenges fall outside ACC’s remit, leaving households to rely on savings or benefits.

The government’s work on the New Zealand Income Insurance Scheme shows recognition of this gap, proposing benefits of up to 80% of prior earnings for eligible workers. However, as the scheme is still under consultation, it will not immediately replace the need for private policies.

For Kiwis juggling mortgages, rent, or raising children, an income protection policy provides certainty in uncertain times. It ensures essential bills are paid, maintains living standards, and protects long-term financial wellbeing. Especially when illness or disability strikes unexpectedly.

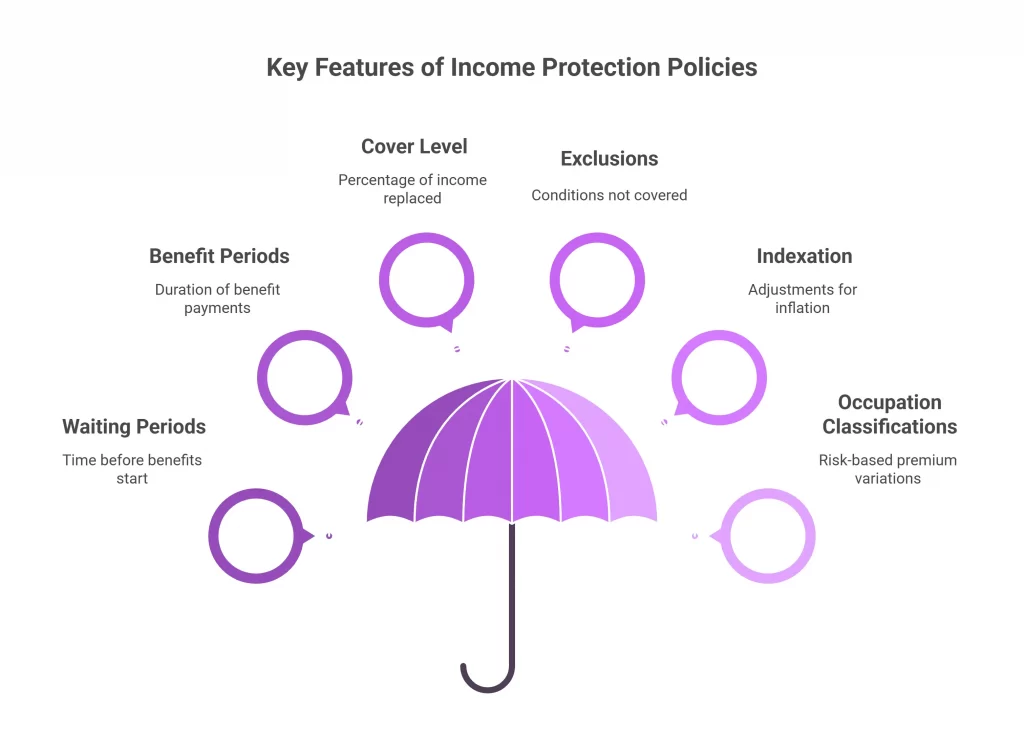

Key Features to Compare

When evaluating the best income protection policy, understanding key policy features is critical. While premiums often drive decisions, the true value lies in how well the policy protects income during a crisis.

1. Waiting Periods

The waiting period is the time between losing income and receiving your first payment. Submissions to MBIE on the proposed income insurance scheme confirm that standard waiting periods are approximately 13 weeks, although some suggest extending them to seven months to reduce premiums by 10–20%. A shorter waiting period offers faster protection, but it also raises the cost.

2. Benefit Periods

Benefit periods determine how long you will be paid. In New Zealand, standard terms range from two years up to age 65 . Longer terms provide stronger security but increase premiums. The best option balances affordability with the length of cover needed for your financial obligations.

3. Cover Level (Income Replacement Rate)

The proposed New Zealand Income Insurance Scheme suggests cover of up to 75% of previous earnings (Based on the providers). Many private policies align with this benchmark. Choosing a lower replacement rate can make premiums more affordable, but risks leaving households unable to meet essential expenses.

4. Exclusions

All policies carry exclusions. Commonly excluded are pre-existing conditions, self-inflicted injuries, or certain mental health conditions. Reviewing exclusions ensures you’re not caught off guard when making a claim.

5. Indexation and Inflation Adjustments

Some policies include indexation, where benefit payments rise annually in line with inflation. This prevents payouts from losing value over time—a key safeguard given New Zealand’s rising household living costs (Stats NZ).

6. Occupation Classifications

Premiums vary by occupation. Higher-risk jobs may face higher costs or reduced options. Carefully check how your occupation is classified and whether another provider offers better terms.

The best income protection policy is one that balances waiting periods, benefit length, cover level, and affordability—ensuring your income is protected when it matters most.

Ready to match key features like waiting periods or benefit terms to your needs? Use our comparison tool to find your perfect fit.

Tax Considerations in NZ

When comparing the best income protection policy, understanding New Zealand’s tax rules is essential. Premiums and payouts are treated differently depending on whether the policy is held personally or through an employer.

Individual Policyholders

According to Inland Revenue, individuals may claim the cost of income protection insurance as a non-business expense if the benefit is taxable. This means you can include premiums in your tax return only where any payout is counted as income (IRD). Policies that provide non-taxable benefits—such as lump sums—are generally not deductible.

Employer-Paid Policies

When an employer pays premiums for an employee, those premiums are not subject to PAYE or fringe benefit tax (FBT), provided the employer is liable for the payments. However, if a claim is made, the resulting benefit payments are treated as assessable income for the employee (IRD Tax Technical QB 18/04).

Payouts

Claim payments received under income protection insurance are typically taxable as income. This is different from life insurance lump sums, which are not taxable.

Understanding these rules ensures you avoid unexpected tax bills and maximise available deductions. An income protection policy should not only meet your household needs but also align with your tax obligations in New Zealand.

Want help finding a policy that’s tax-smart and tailored to your work type? Compare smart income protection options here

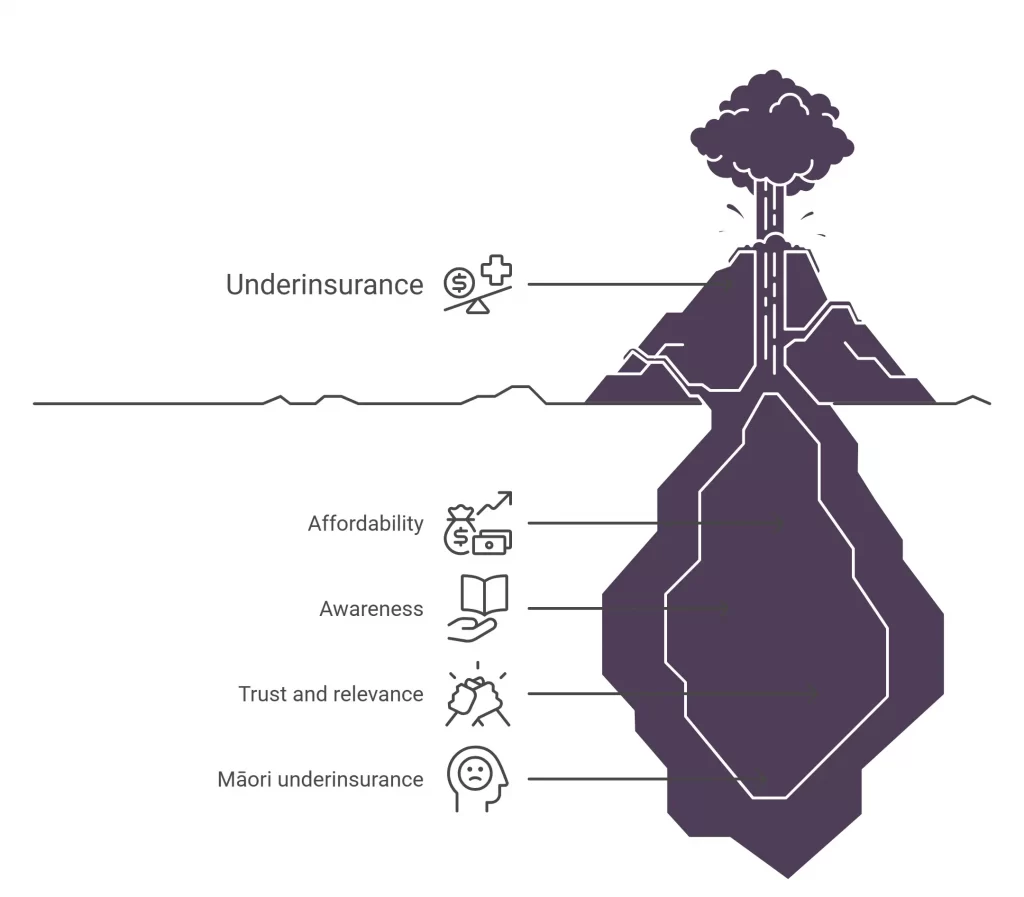

Policy Access & Underinsurance Issues

One of the biggest challenges in identifying the best income protection policy is ensuring that all New Zealanders can access it. Evidence shows that many households remain underinsured, leaving them financially vulnerable if income stops.

The Retirement Commission highlights that Māori have the lowest insurance uptake in New Zealand, including life, health, and income protection products. This underinsurance gap is particularly concerning because Māori also experience higher rates of chronic health conditions, which increase the risk of needing time off work.

Barriers to access include:

- Affordability: Rising living costs and high household debt make regular premiums difficult for many families.

- Awareness: A lack of clear financial education means many Kiwis don’t fully understand what income protection covers.

- Trust and relevance: Standardised policies may not always reflect the needs of diverse communities, leading to disengagement.

Government work on the New Zealand Income Insurance Scheme seeks to address some of these gaps by extending coverage to part-time, contract, and self-employed workers with regular earnings. However, private policies remain a vital tool for families seeking more comprehensive or immediate protection.

To close the underinsurance gap, financial advice, cultural accessibility, and community engagement will be key.

Struggling to find inclusive cover options? Compare policies designed for diverse needs—Compare Now.

FAQs About the Best Income Protection Policy

What is income protection insurance in New Zealand?

The best income protection policy provides regular payments if you’re unable to work due to illness or injury. Unlike ACC, which only covers accidents, private policies also cover health conditions such as cancer or heart disease.

Why is the uptake of income protection so low in NZ?

Research indicates that only a small percentage of New Zealanders hold income or mortgage protection insurance. Barriers include affordability, lack of awareness, and perceptions that ACC or government benefits are sufficient.

Are premiums for income protection tax-deductible?

Yes, but only in some instances. Individuals can claim premiums as a non-business expense if payouts are taxable, while employers may claim deductions for policies they provide.

Are income protection payouts taxable?

Yes. Payments received are treated as assessable income under Inland Revenue rules (IRD Tax Technical QB 18/04). This differs from life insurance lump sums, which are not subject to taxation.

When should I update or review my policy?

It’s best to review your income protection policy whenever your circumstances change—such as starting a new job, taking on a mortgage, or having children—to ensure the cover remains adequate.

Still unsure which policy suits you best? Compare tailored options now and find clarity.

Final Thoughts

Choosing the best income protection policy is about securing more than just a safety net—it’s about protecting your family’s future and peace of mind. With most Kiwis still uninsured, and ACC unable to cover income loss from illness, the gap is clear. Government initiatives may help, but private policies remain the most direct way to safeguard earnings. By weighing features like waiting periods, benefit terms, and tax implications, you can make an informed choice that ensures your household stays financially resilient through life’s uncertainties.

Your income is your most valuable asset. Don’t leave it to chance—Compare the best income protection policies in New Zealand today and start building your financial resilience.

Protect Your Income Today

Your income is your most valuable asset—without it, everyday life quickly becomes unaffordable. Don’t wait until it’s too late. Compare the income protection policy options available in New Zealand, tailored to your needs, and safeguard your future today with Compare Income Protection.

{kind=link}

{kind=link}

{kind=link}