Why Are Income Protection Claims Denied? Common Pitfalls Explained

When Kiwis claim income protection, most declines can be attributed to a handful of fixable issues—such as missing information, policy exclusions, or timing mistakes. Understanding these patterns now can save you stress later and help you set up coverage that actually pays when you need it.

In New Zealand, the core reasons income protection claims denied often come down to:

(1) non-disclosure, (2) exclusions, (3) not meeting the policy’s disability definition, (4) waiting/benefit-period timing, and (5) admin slip-ups. We’ll unpack each—and show you how to avoid them—so your future claim stands the best chance of approval.

Key Takeaway

- Disability is common: In 2023, 17% of people living in New Zealand households—about 851,000 people—were identified as disabled. That’s a clear signal that loss of earning capacity is a real, not rare, risk. Stats NZ

- ACC covers accidents, not illness: ACC is brilliant for accidental injuries, but it doesn’t cover general illness or age-related conditions—the very scenarios income protection is designed for. ACC

- If you’re injured, ACC may pay up to 80% of income (after a 1-week stand-down): For covered injuries, ACC pays up to 80% of pre-injury earnings, and eligibility starts after the first week off work; illnesses aren’t covered. ACC

- Government benefits are modest if you’re too sick to work: As a benchmark, Jobseeker Support rates (as scheduled for 1 April 2025) show how limited base government assistance can be relative to an average salary, making private cover important. Work and Income

- Disclosure rules are being modernised: The Contracts of Insurance Bill replaces the old “utmost good faith” approach with a fairer duty to take reasonable care not to misrepresent, aiming to reduce unfair non-disclosure disputes. (Honesty still matters—hugely.) Legislation New Zealand

Bottom line: Know the landscape, set up your policy carefully, and you’ll sidestep the most common reasons income protection claims denied. Ready to compare wording and wait times across providers? COMPARE NOW.

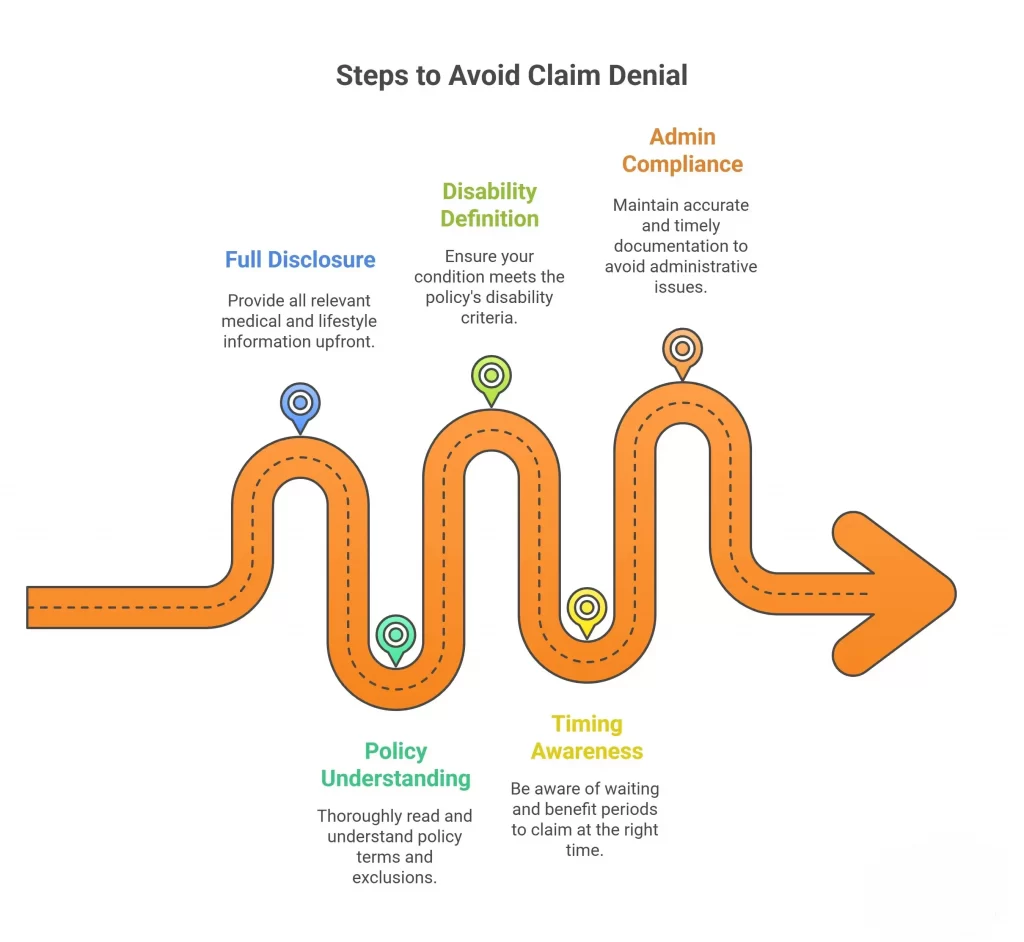

Non-Disclosure of Medical Information

What it is (and why it sinks claims): A non-disclosure claim issue happens when details that could influence an insurer’s decision weren’t shared at application—think previous diagnoses, specialist referrals, test results, medications, or risky hobbies. New Zealand’s Contracts of Insurance Act 2024 has been enacted but is not yet commenced. When it commences, consumers will have a duty to take reasonable care not to make a misrepresentation when answering insurers’ questions. Dishonest misrepresentations are treated as a failure to take reasonable care—so accuracy matters. Legislation New Zealand

Why questions matter (but your answers matter more): The reform shifts emphasis onto insurers asking clear, targeted questions. Your job is to answer those questions completely and truthfully, using what you know (and checking records if you’re unsure). This modernised approach is intended to reduce unfair denials where people innocently missed something they didn’t realise was relevant—but it still relies on your full, careful disclosure. MBIE

Avoid insurance claim denial: a 60-second disclosure checklist

- List all diagnoses you’ve ever received (including mental health) and ongoing symptoms under investigation.

- Include tests, scans, GP referrals, prescriptions, and any specialist follow-ups (even if results were “normal”).

- Note time off work, ACC injury claims, and any recurring conditions (e.g., migraines or back pain).

- Declare lifestyle risks: smoking/vaping history, high-risk sports, heavy lifting, or hazardous work.

- Be precise about medications (including dosages, dates started/stopped), and treatment plans.

- Cross-check your answers with GP notes or patient portals before submitting.

- If something is unclear, say so and provide context rather than guessing.

Real-world tip: Many Reasons Income Protection Claims Denied begin with small omissions (“I forgot that specialist referral”) that later look like misrepresentation. Slow down, keep notes, and attach supporting documents so your application and any future claim line up cleanly. For plain-English guidance on what good insurance conduct looks like for consumers in NZ, see the Financial Markets Authority’s consumer pages. Financial Markets Authority

Unsure which insurer’s questions or wording suit your health history best? Compare policies side by side and get clarity before you apply. Compare now.

Condition Not Covered by Policy

Why claims get declined: Even good policies have exclusions and limitations. If your condition falls within one of those, the insurer can claim it’s outside the scope. Common examples include pre-existing conditions (symptoms, tests, or diagnoses before you applied). Some insurers offer optional mental-health (and sometimes back) claim caps (e.g., 24 months) for a lower premium — check if that option is applied to your policy.

self-inflicted injuries, or high-risk activities listed as excluded. When a claim touches any of these, it becomes one of the classic reasons for claim rejection.

How to spot what’s not covered (before you need it):

- Read the Policy Schedule (your personal terms) and the full Policy Wording—that’s where exclusions and offsets live.

- Look for pre-existing condition rules (what’s the “look-back” or stand-down on prior conditions?).

- Check any mental health provisions (waiting periods, maximum months payable, treatment requirements).

- Confirm occupation class rules (some hazardous duties or second jobs may be excluded).

- Ask about offsets (e.g., how payments interact with other sources like ACC for accident-related injuries).

- Get clarifications in writing (email from the insurer/adviser) and save them with your policy.

Make coverage match your risks: If an exclusion would cut across your real-world risks (say, a known back issue or recurring migraines), consider a provider that can remove or narrow that exclusion, or adjust structure (benefit period, waiting period, own-occupation definition) so you’re not paying for cover you can’t use. A quick primer on where income protection fits next to accident cover is here: ACC vs Income Protection Insurance in New Zealand.

Pro tip (keep it simple): Create a one-page “what’s in / what’s out” summary for your policy and review it annually. That habit alone avoids many Reasons Income Protection Claims Denied later.

Not sure which provider’s wording suits your health history and job? Compare the fine print side-by-side: COMPARE NOW.

Not Meeting the Disability Definition

Why claims get declined: Income protection only pays when you meet the policy’s definition of total or partial disability. If the insurer believes you can still perform the substantial duties of your job (or a suitable alternative role) — even part-time — they may decide you don’t meet the threshold. Typical triggers are: you’ve returned to light duties, medical notes suggest capacity for “alternative work,” or the evidence doesn’t align with the policy wording.

How to line up your evidence (so your claim fits the wording):

- Match your job duties to the policy: List your core tasks (time on feet, lifting, concentration, travel, safety-critical work) and link each to what your condition prevents.

- Ask your GP or specialist to be specific: Reports should state which inherent duties you can’t perform and for how long, not just the diagnosis.

- Be consistent across documents: Employer letters, ACC notes (if applicable), and medical certs should tell the same story about capacity and restrictions.

- Watch “any-occupation” vs “own-occupation”: If your policy is “any-occ,” expect tougher scrutiny around whether you could do some work. “Own-occ” tends to focus on your actual role. For a quick primer on getting definitions right before you buy, see this checklist on reviewing definitions. Compare Income Protection

Example: A project manager with severe migraines can’t tolerate screen time or meetings >30 minutes. Their specialist letter ties symptoms to essential duties (planning, stakeholder sessions, long screen exposure) and duration — this aligns with the policy’s disability test and strengthens the claim.

If you want a policy whose definition suits your job and health history, compare wordings side by side. Compare now

Getting this right prevents many Reasons Income Protection Claims Denied later on.

Claim During Waiting Period or Outside Coverage Period

Where timing trips people up:

- Waiting (stand-down) period: Benefits don’t start until your selected waiting period ends (e.g., 4, 8, 13, 26 weeks). Claiming “too early” means the policy won’t pay yet.

- Benefit period: Payments stop at the end of your chosen duration (e.g., 2 years, 5 years, to age 65). If your incapacity outlasts that, the policy cannot continue to pay.

Plan your cash flow around the clock:

- Map out weeks 1–13: Use sick leave, savings, or partner income to bridge the waiting period.

- Pick the right wait time upfront: Longer waits cut premiums but require a bigger buffer; shorter waits cost more but pay sooner. See the step-by-step guide to choosing an appropriate waiting period for NZ workers.

- Know how accidents interact with private cover: If an accident triggers ACC payments, your income protection may top up after the waiting period rather than duplicate benefits. (More on the ACC vs IP “who pays first” question here.)

Quick worksheet:

- Add up accessible savings + sick leave.

- Choose the longest waiting period your buffer can comfortably cover.

- Confirm the benefit period suits your risk (e.g., chronic conditions might justify longer).

Dial in a wait/benefit combo that matches your budget and risk tolerance: COMPARE NOW.

Mis-timed claims are common Reasons Income Protection Claims Denied — understanding waiting and benefit periods keeps you out of that trap.

Administrative or Technical Issues

Why perfectly valid claims still get tripped up: Many declines aren’t about medical eligibility at all—they’re avoidable admin snags. Missing or inconsistent paperwork, late notifications, or a lapsed policy can stall or sink a claim. These process errors are among the quiet but common Reasons Income Protection Claims Denied in New Zealand.

Typical admin pitfalls to watch for

- Missing proof of income:

○ Employees: recent payslips (usually 3–6), employment agreement, and sometimes a letter from HR confirming hours and role.

○ Self-employed/contractors: latest IR3/financials, profit & loss, bank statements, and (ideally) an accountant’s letter explaining income trends or seasonal variability.

- Inconsistent info: Dates off work, job duties, or treatment history that don’t match between claim forms, medical notes, and employer letters.

- Late or incomplete medical certificates: Certificates without functional restrictions (what you can’t do at work) or with open-ended timelines invite pushback.

- Policy lapsed due to unpaid premiums: If cover isn’t in force on the event date, the insurer can’t pay. Reinstatement may require fresh health disclosures or waiting periods.

- Not telling the insurer about material changes: For indemnity-style benefits, changes to income/employment status can affect what’s payable. If you’ve shifted roles, reduced hours, or changed structure (e.g., sole trader → company), update the insurer.

- Wrong claim timing logistics: Submitting before your waiting period ends, or forgetting to provide updated documents at review points during a long claim.

A tidy claim file = fewer hurdles

- Create a single digital folder with subfolders for medical records, employment/income information, and correspondence.

- Use a simple timeline doc (dates of symptoms, GP visits, specialist referrals, time off work).

- Ask your GP/specialist to include functional limitations tied to job duties (not just a diagnosis).

- Set up a direct debit for premiums and add a calendar reminder to check that payments have cleared.

- Get an accountant’s letter (if self-employed) summarising income stability/seasonality to pre-empt questions.

- Ask the insurer (or your adviser) for a document checklist at lodgement—and confirm by email when they have everything.

Helpful internal resource: If you’re about to lodge, walk through this step-by-step primer: How to Claim Income Protection Insurance in New Zealand—it covers timing, documents, and what to expect in the assessment process.

Prefer a policy with clearer paperwork and stronger guidance at claim time? Compare Now! side by side to see your options

How to Avoid Claim Problems

You can prevent most headaches by setting things up right at the start—and staying organised when it’s time to claim. Use this quick action plan to dodge the most common Reasons Income Protection Claims denied in New Zealand.

1) Disclose everything (no surprises later)

- Treat the application like a medical timeline: diagnoses, tests, referrals, medications, time off work, and high-risk activities.

- If you’re unsure, add context rather than making a guess. This avoids a non-disclosure claim issue and helps you avoid insurance claim denial later.

2) Check exclusions match your real risks

- Scan policy wording for pre-existing conditions, mental health limits, hazardous duties, and offsets.

- If an exclusion affects your history, ask whether it can be removed/limited—or compare providers that handle it more effectively. That’s how you get ahead of claim rejection causes.

3) Align the disability definition with your job

- Prefer “own-occupation” where appropriate; it focuses on your actual role.

- Keep evidence job-specific: which inherent duties (lifting, screens, travel, concentration, safety-critical tasks) you can’t perform and for how long.

4) Get timing right (waiting & benefit periods)

- Choose a waiting period that your savings can genuinely cover; longer waits lower premiums, but demand a bigger buffer.

- Select a benefit period that aligns with your risk (e.g., individuals with chronic conditions may require a longer period).

- If an accident is involved, remember that ACC may pay first—your policy often tops up after your stand-down period.

5) Nail the paperwork

- Before lodging, gather the following documents: medical certificates (with functional limits), payslips/IR returns or an accountant’s letter, employer confirmation of duties/hours, and a simple event timeline.

- Keep premiums on auto-pay so the policy is always in force.

6) Review yearly (or after life changes)

- Promotions, role changes, income shifts, new diagnoses, or family changes can all affect coverage. A quick annual check keeps you out of the “technical denial” bucket.

7) Compare providers before you commit

- Wordings, exclusions, and claims support models vary widely. Comparing side-by-side helps you avoid the classic Reasons Income Protection Claims denied that come from buying the wrong fit for your situation.

Ready to see differences in waiting periods, definitions, and exclusions? COMPARE NOW

FAQs

Q: Does ACC cover illnesses?

A: No. ACC is designed for accidents and injury-related conditions. It does not cover general illnesses or age-related conditions. For injuries, ACC can help with treatment and (if eligible) income support; for illness, you’d look to income protection instead.

Q: When do ACC weekly compensation payments start, and how much do they pay?

A: If ACC accepts your injury claim and you can’t work, weekly compensation is up to 80% of your income and typically starts after the first week you’re off work (there’s a one-week stand-down).

Q: What changed with NZ insurance disclosure law—do innocent mistakes always void a policy?

A: Under the Contracts of Insurance Act 2024, consumers must take reasonable care not to make a misrepresentation when answering an insurer’s questions. This modernises the old “duty of disclosure.” Remedies are intended to be proportionate to the type of misrepresentation (e.g., whether it was honest and reasonable vs. reckless or deliberate), rather than automatically voiding cover in every case. Still, the safest path is to disclose fully and clearly.

Q: If I’m too sick to work and don’t have income protection, what government support could I get?

A: Check Work and Income’s current benefit rates (e.g., Jobseeker Support). These payments are means-tested and generally modest compared with most salaries, so many Kiwis use income protection to bridge the gap.

Conclusion

Most declines aren’t mysteries—they’re preventable. If you disclose fully, choose wording that matches your job and health, mind the waiting/benefit periods, and keep documentation tidy, you’ll sidestep the usual traps. And because ACC covers injuries (not illness) and government benefits are modest, getting your private cover right really matters.

If you’re comparing options, focus on the details that decide outcomes at claim time: disability definitions, exclusions, offsets, and admin support. That’s how you avoid the most common Reasons Income Protection Claims denied and set yourself up for a smoother claim experience.

When you’re ready, line up policies side by side to find the best fit.

{kind=link}

{kind=link}

{kind=link}

{kind=link}